Beyond Potency: How Brands Can Stand Out With Effects-Driven Strategies

Introduction

Product development in cannabis has long been dominated by a THC arms race, with brands pushing potency higher and higher. While marketing products around strength and price has been proven to drive sales, this strategy does not necessarily appeal to the consumer segment most likely to fuel sustainable growth in the industry.

So, how else can brands and retailers attract new customers and, more importantly, turn them into educated, loyal return buyers?

One promising path is effects-based marketing. Some of the industry's largest brands are already developing product lines that highlight specific cannabinoid combinations. By educating consumers and setting clear expectations around targeted effects, these brands help customers shop with confidence and build trust in what the product will deliver. While effects-driven positioning is common in some categories, it is only beginning to take root in others, leaving substantial room for growth.

The opportunity now lies in creating a blueprint that carries effects-based products into new categories, helping consumers navigate beyond potency and price. A thoughtful framework can not only drive trial but also foster brand champions as customers who are engaged, informed, and eager to advocate for products that truly meet their needs.

Methodology

Data for this report come from real-time sales reported by participating cannabis retailers via their point-of-sale systems, which are integrated with Headset's business intelligence platform. Because the data are transmitted digitally and directly from partner retailers, Headset's dataset is highly reliable. Nevertheless, occasional inaccuracies may occur—for example, duplicate transactions, misclassified products, incorrect product entries in point-of-sale systems, or simple human error at checkout—so a small margin of error should be assumed. While the presence of non-THC cannabinoids may be presented in test results or within the packaging, Headset flags the presence of cannabinoid as they are presented in the product title. Based upon how some products present this information they may be excluded from being flagged for non-THC cannabinoids.

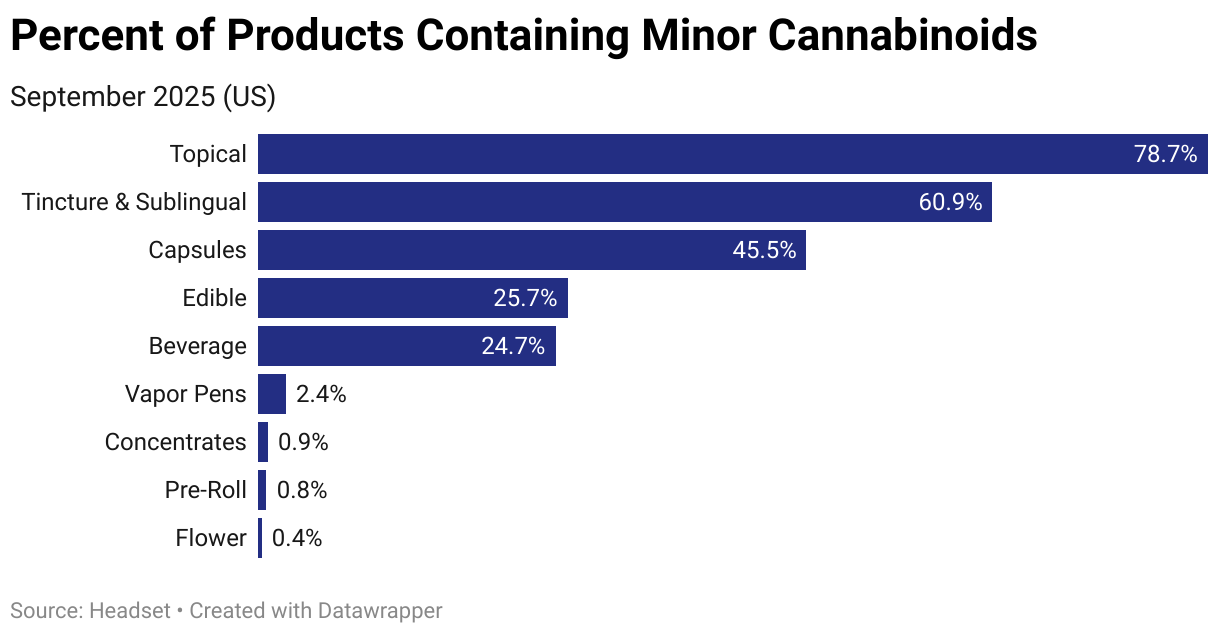

Cannabinoid marketing is most prevalent in wellness categories such as topicals, capsules, tinctures, and sublinguals where a majority of products reference specific cannabinoids to target health concerns or steer consumers toward a desired effect. Edibles and beverages, which straddle wellness and recreation, also feature extensive cannabinoid-forward positioning. These categories are seeing the fastest growth in this approach, with a 6–12% year-over-year increase in the number of distinct products that reference non-THC cannabinoids.

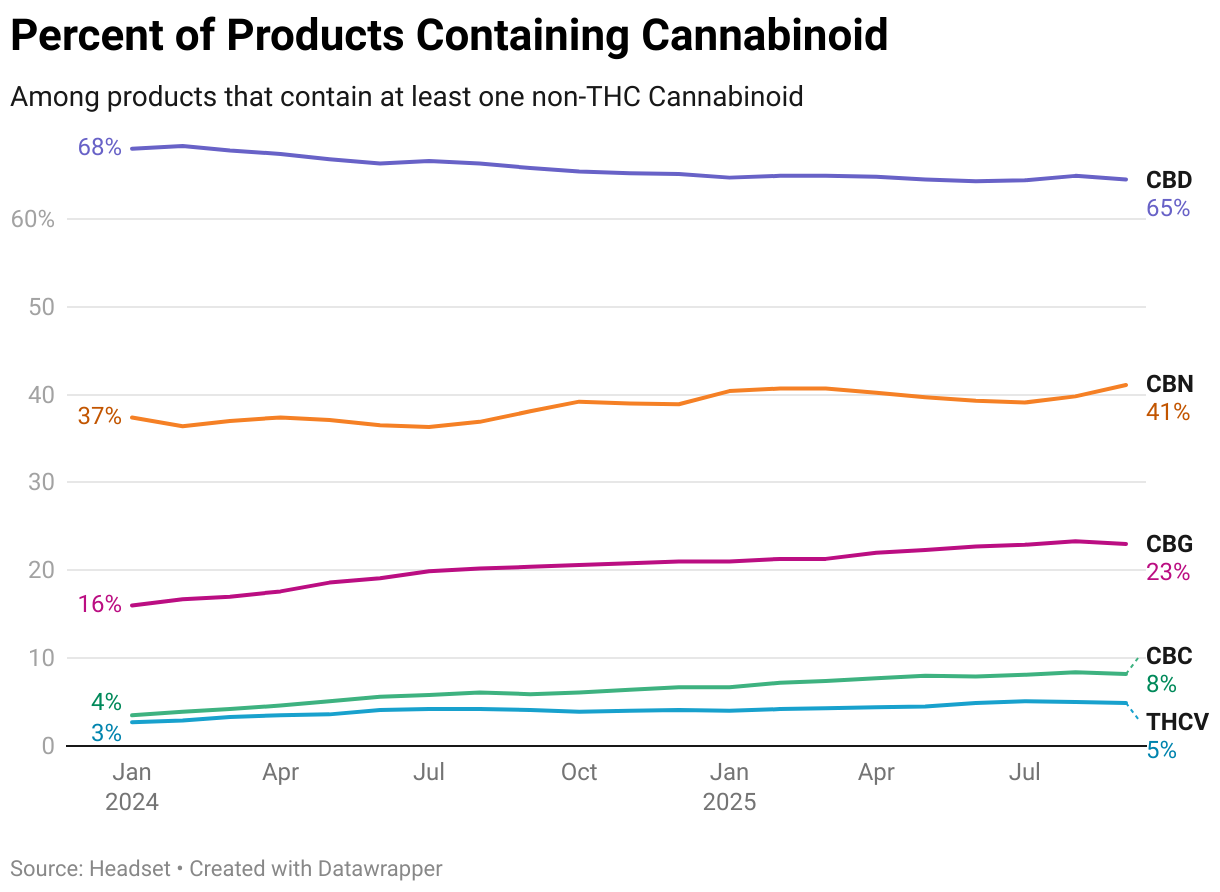

Historically, CBD has dominated the non-THC cannabinoid market as the most widely recognized compound in the category. Today, it still appears in about 65 percent of products marketed with non-THC cannabinoids, but its share has declined as other cannabinoids gain momentum. CBN is now featured in roughly one-third of these products, while CBG, THCV, and CBC continue to grow in presence. Notably, CBC and THCV have shown the sharpest recent gains, now appearing in more than 8 percent and 5 percent of non-THC cannabinoid-marketed products, respectively.

.png)

Kiva's Camino brand is a strong example of an alternative to the potency and price-driven marketing that dominates much of the cannabis industry. The line features dozens of products with a variety of cannabinoid combinations, focusing on the experience rather than raw potency. Many Camino offerings come in lower dosages, typically between 2 and 10 milligrams of THC per serving, which appeals to consumers who are less motivated by potency and more inclined toward a specific experience.

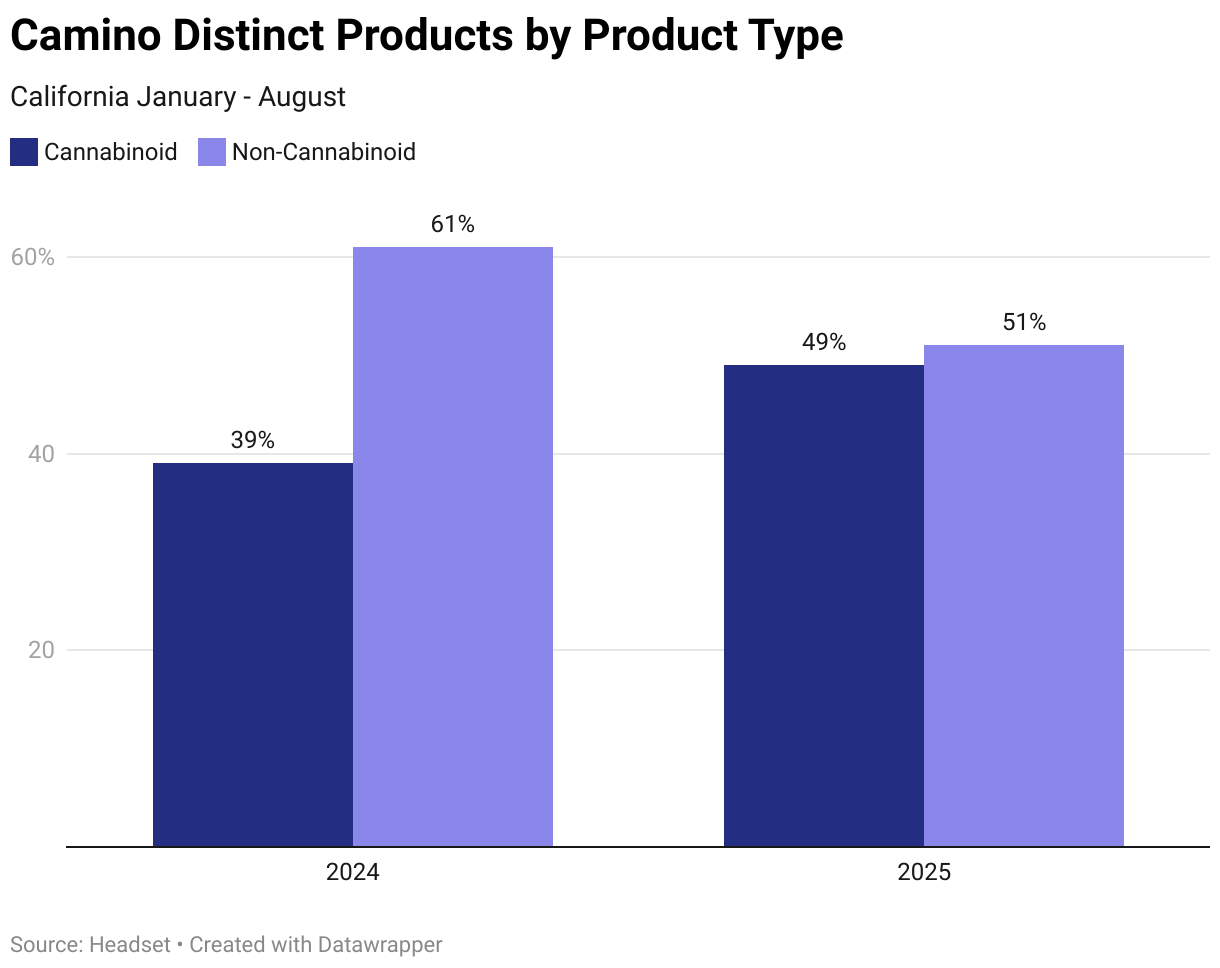

While Camino's California edible portfolio includes both traditional formulations and products featuring non-THC cannabinoids, it is clear the brand is leaning into offering a diverse range of cannabinoid experiences. In 2024, nearly 40 percent of its distinct products in California highlighted alternative cannabinoids. By 2025, that share had grown to almost half of the portfolio, with products increasingly formulated and marketed around varied cannabinoid ratios.

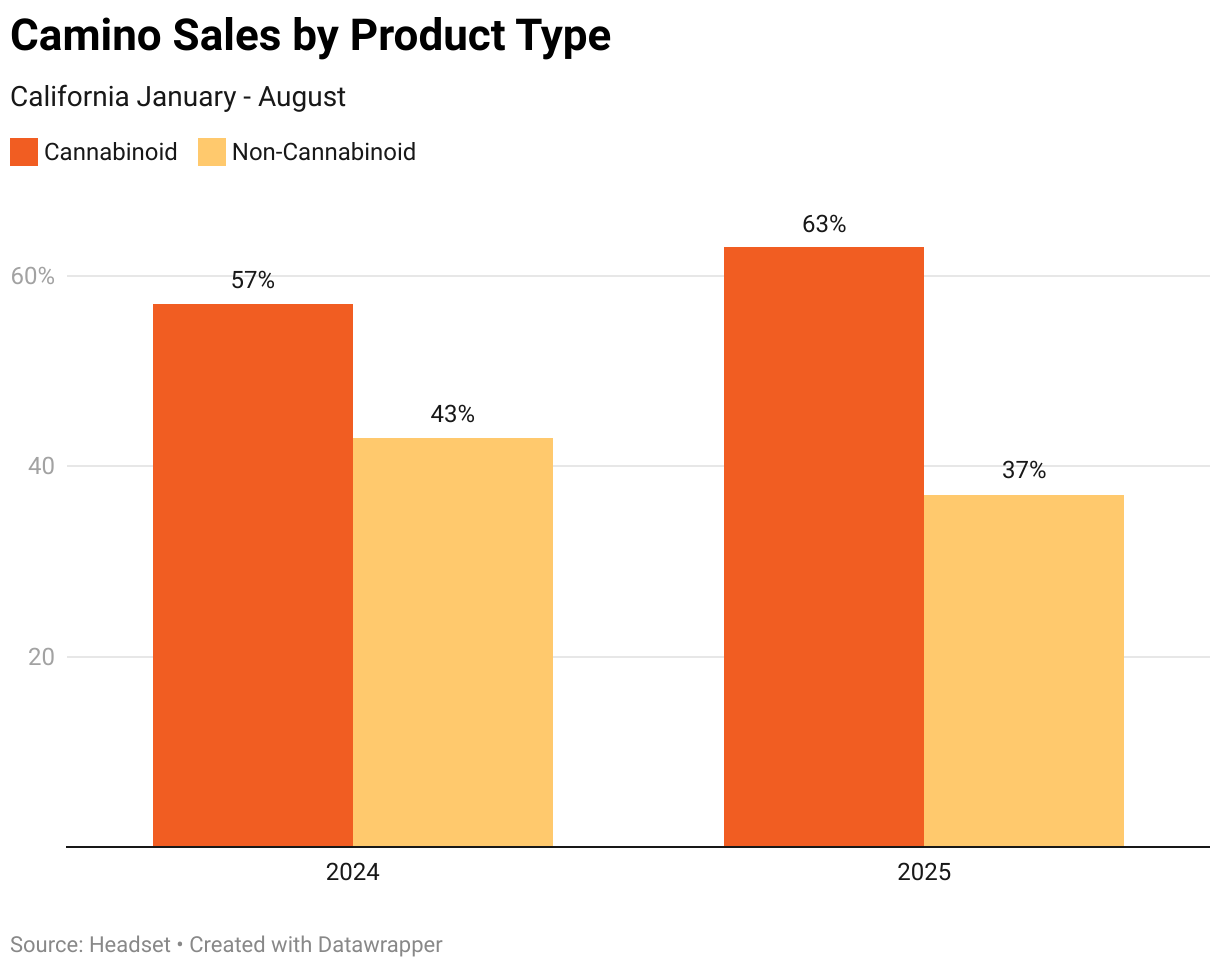

The shift in product mix is likely driven by the outsized sales performance of products marketed around cannabinoids. In 2025, although only half of Camino's portfolio highlighted alternative cannabinoids, these products accounted for 63 percent of total sales in California.

Conclusion

Potency and price remain two of the most important value propositions for brands and retailers looking to drive sales. However, as operators seek to diversify their product offerings and engage new customers, cannabinoid-driven and effects-based products have emerged as a compelling alternative to strategies focused solely on cheap, high-THC products.

Camino demonstrates this approach at scale, but they are not alone. Alongside Camino, Wyld has also leaned heavily into cannabinoid-focused formulations, and together the two brands dominate California's edible market. In fact, six of the top ten edible products in the state are marketed containing a variety of cannabinoids.

While edibles and wellness products have pioneered this type of marketing, the approach is increasingly visible in other categories as well. Beverages featuring THCV or CBN, as well as vapor pens marketed with effects-based language, highlight how brands are extending beyond potency into new territory. This diversification offers a path to reach a different type of customer, one who is motivated to learn, willing to pay more, and eager to return for products that deliver a unique and reliable experience.