Unlocking Opportunity in Connecticut’s Cannabis Market

Introduction

In 2021, Connecticut became the 19th state to legalize recreational cannabis. Eighteen months later, the regulatory framework was finalized, and adult-use sales officially launched in January 2023. As one of the newer entrants in the rapidly expanding Northeastern cannabis market, alongside neighbors such as Massachusetts, New York, and New Jersey, Connecticut is quickly establishing its place in the region.

The market is still in its early stages, but local cultivators, retailers, and brands are beginning to emerge alongside national players, creating a dynamic environment marked by challenges around pricing, competition, and access. At Headset, we provide the data and insights to illuminate how Connecticut’s market is evolving in comparison to both regional and national peers. From brand landscape and pricing trends to category preferences, consumer demographics, and more, our analysis helps identify how this market is taking shape.

Methodology

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally directly from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. In this report, we examine sales from US Headset Insights markets. Unless otherwise mentioned the analysis period is January - August 2025.

Key Takeaways

- Although Connecticut is a smaller state within the emerging Northeastern cannabis market, its sales trail comparable states on a per-capita basis, with total sales reaching nearly $300 million in 2024.

- Year over year, Connecticut’s total sales have declined by 2%, while comparable markets such as Missouri and Maryland have grown by 6% and 3%, respectively.

- Regulations have shaped category preferences in Connecticut, as limits on concentrates and beverages have pushed customers toward vapor pens and edibles instead.

- Connecticut’s limited selection of products and brands creates a clear opportunity for new entrants. Increased competition will help drive prices down to more competitive levels.

- Similar to other new markets, Connecticut has some of the highest prices in the country, though they have been declining consistently throughout 2025. The rate of decline has outpaced both comparable markets and the U.S. market as a whole.

- Connecticut’s average basket size is competitive, but it will likely decline as prices fall unless offset by an increase in average units per basket currently the lowest in the country.

- With an average discount rate of 20%, Connecticut is seeing increased use of discounting, though it remains slightly below the national average of 23%.

- Customers aged 45 and older are significantly more represented in Connecticut’s cannabis market than in the rest of the U.S., accounting for 44% of total sales in 2025.

Sales Overview

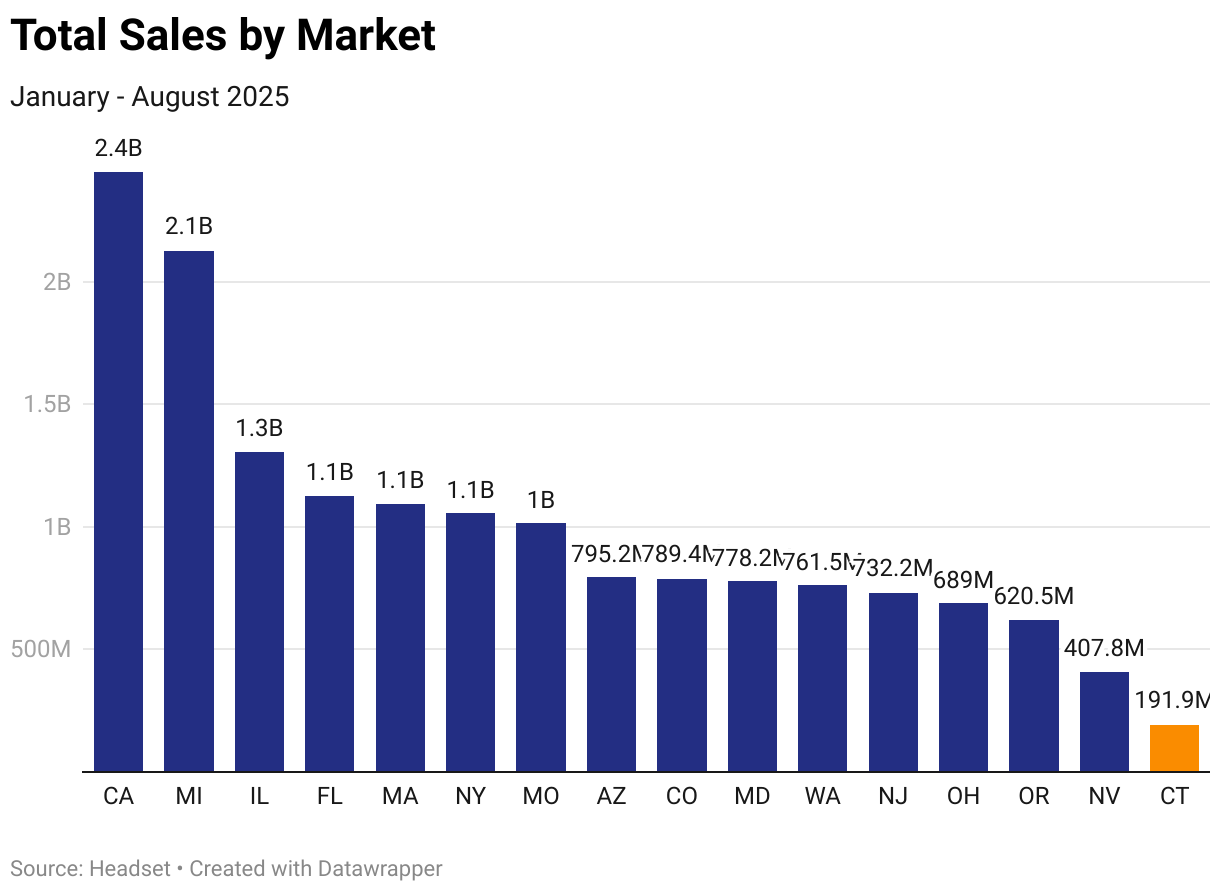

Among all of Headset’s tracked markets, Connecticut reports the lowest total sales, with approximately $300 million in 2024 and nearly $200 million through the first eight months of 2025. However, given Connecticut’s relatively small population of about 3.5 million, the market naturally faces a lower overall ceiling compared to larger states.

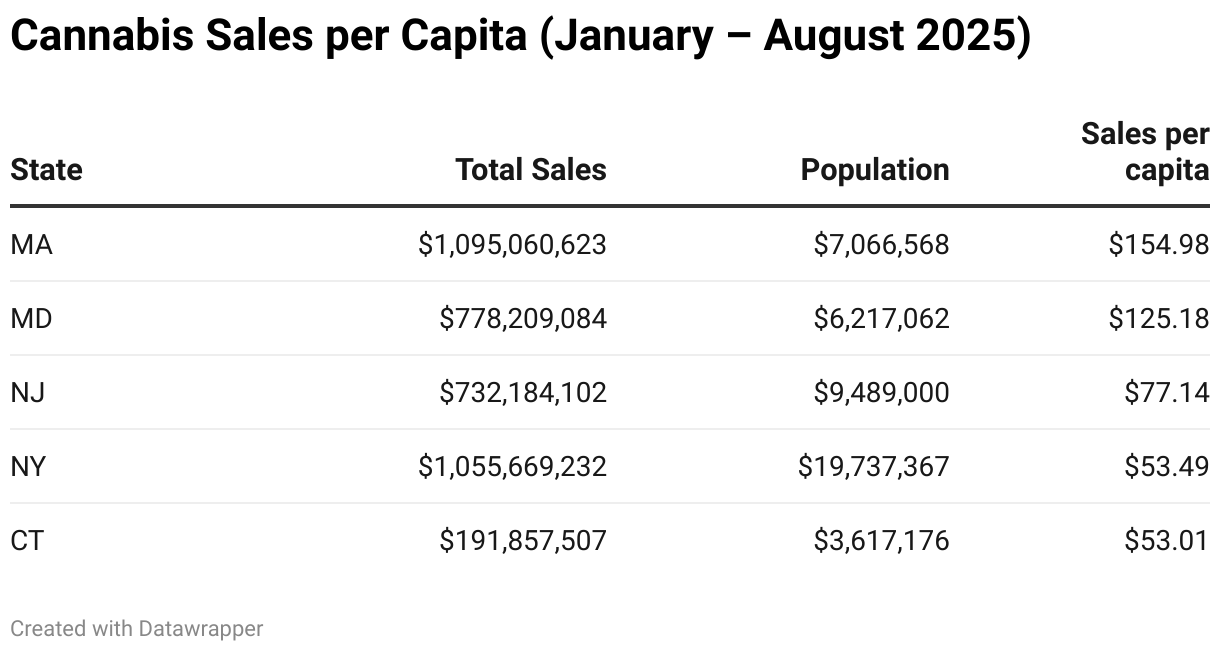

Although Connecticut has a smaller population, the state shows signs of underperforming relative to its sales potential when adjusting for population compared to other regional markets. Sales per capita are approximately 66% lower than regional leader Massachusetts, suggesting there is still significant room for growth within Connecticut’s customer base. However, it is important to view these figures in the context of market maturity. Massachusetts has operated an adult-use cannabis market since 2018, giving it a considerable head start, while Connecticut and other nearby states have only launched within the past five years or less.

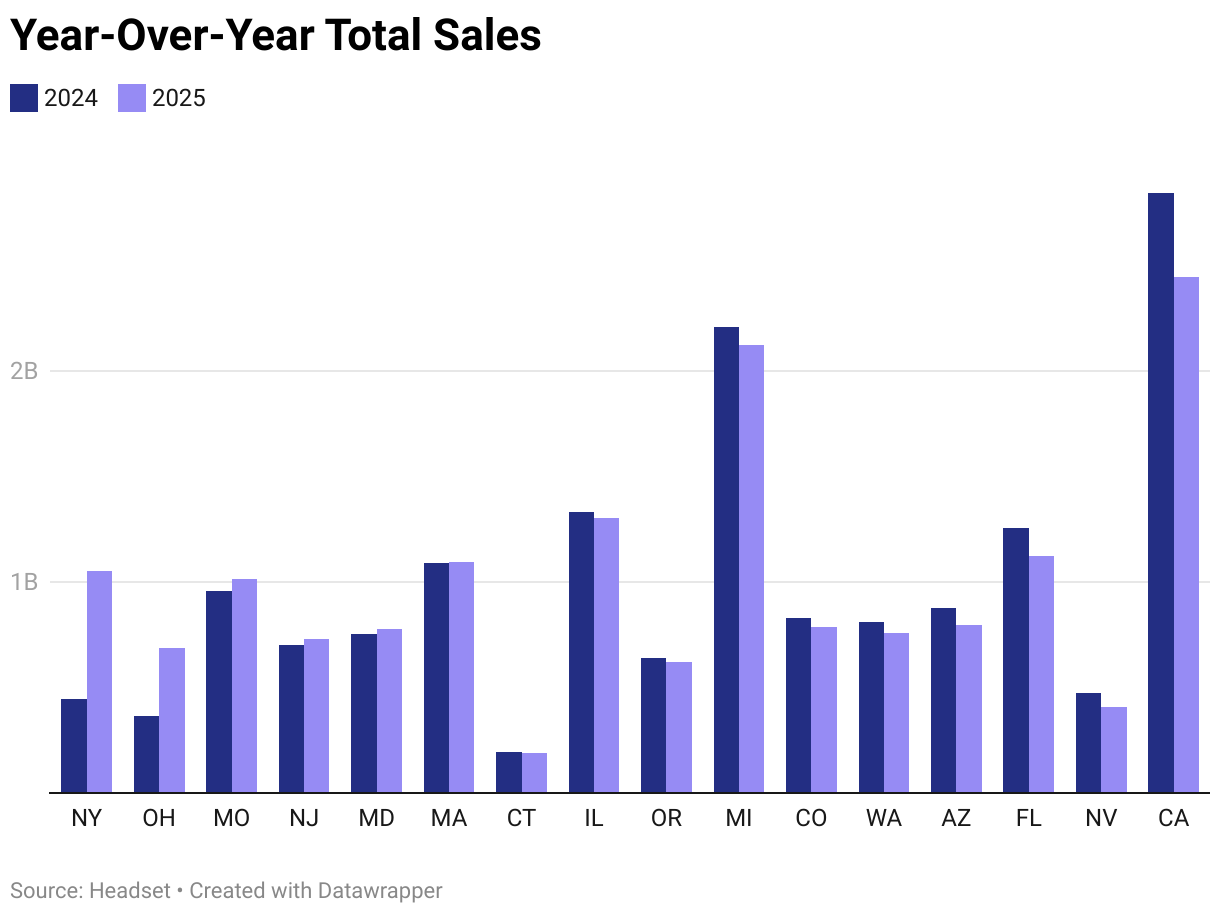

Despite entering the cannabis market less than three years ago, Connecticut is still struggling to generate year-over-year growth. Through August, total sales have declined by 2% compared to the same period in 2024. While flat performance is not uncommon in a highly competitive cannabis landscape, a new market in its third year would typically be expected to post gains driven by falling prices, expanded access, and the release of pent-up demand. By comparison, Missouri and Maryland, which also launched recreational sales in 2023, have grown by 6% and 3% year-over-year, respectively.

Category Performance

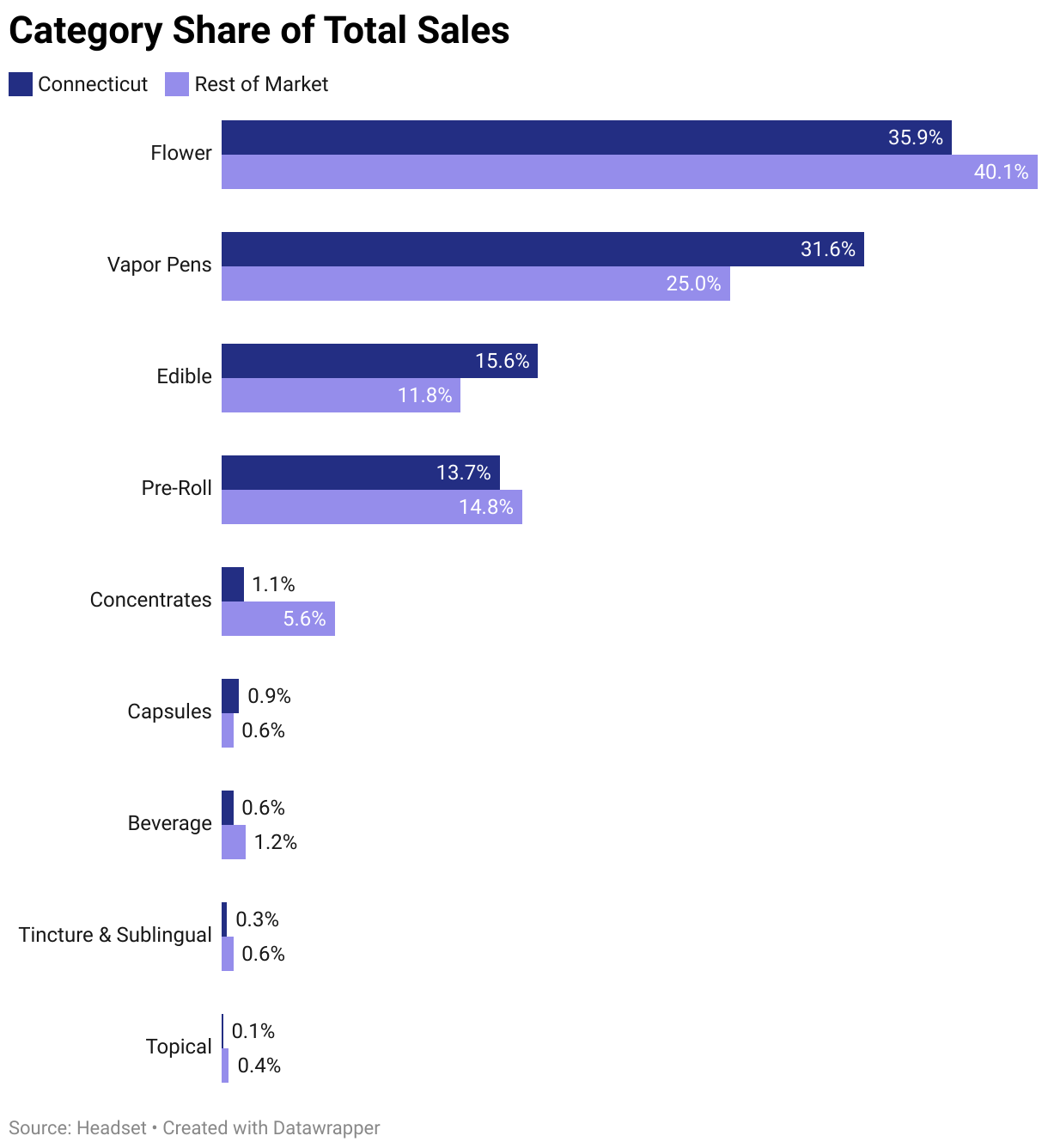

Connecticut’s young market shows some distinct product assortment trends, shaped in part by state regulations. One of the most noticeable differences from the national market appears in the concentrates and vapor pen categories. In Connecticut, concentrates face potency limits that do not apply to vapor pens. As a result, concentrates account for only about 1% of sales, compared to 6% nationally. Conversely, vapor pens are overrepresented, making up nearly 32% of total sales in Connecticut versus 25% at the national level.

Regulation is also influencing the performance of the beverage category in Connecticut, which accounts for just 0.6% of total sales and is shrinking, compared to 1.2% and growing at the national level. The state permits the sale of hemp-derived beverages containing up to 3mg of THC in certain non-dispensary retailers, while at the same time restricting higher-potency beverages within dispensaries, the very products that have historically driven growth in this category. As a result, edibles are overrepresented in Connecticut and have become the dominant non-inhalable option for consumers.

Brand & Product Landscape

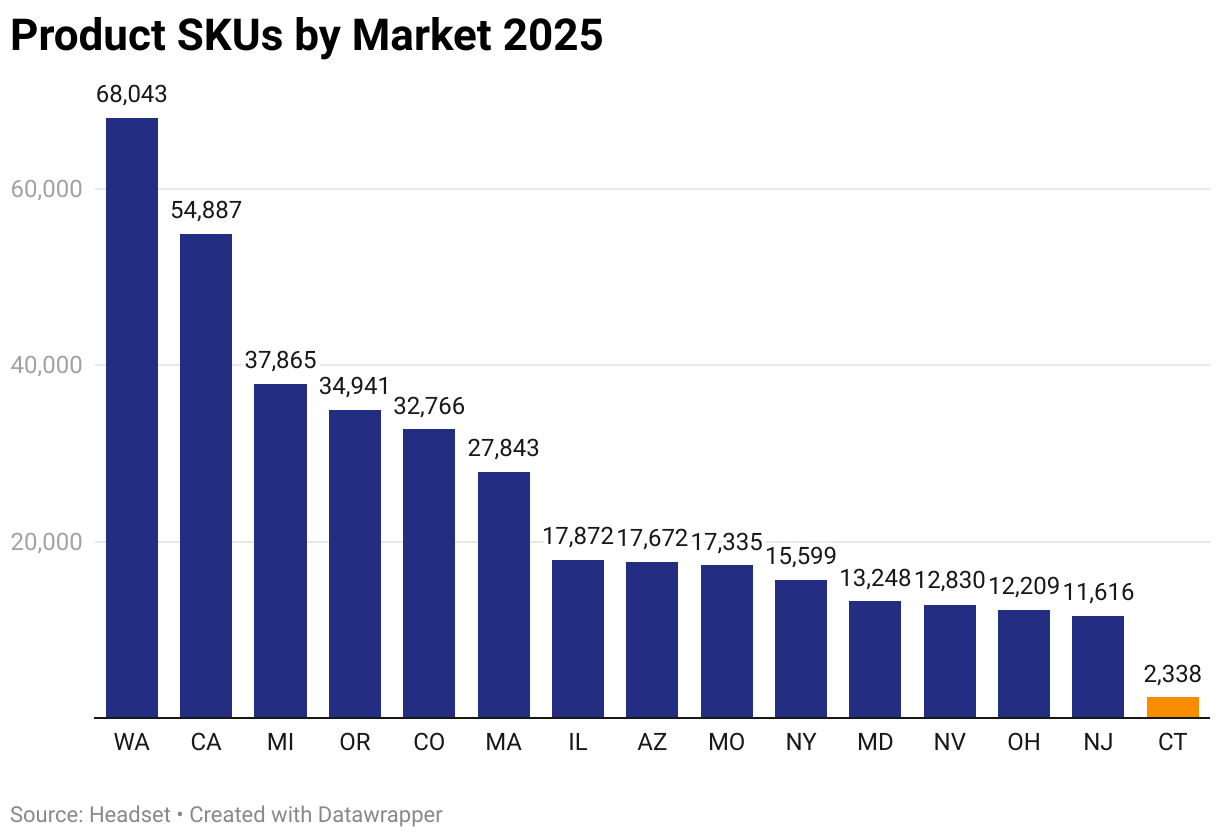

As a smaller market, Connecticut naturally carries fewer SKUs than other states Headset tracks, with the lowest product count overall and 80 percent fewer than New Jersey, the next-smallest market. While a limited number of brands and products is expected given the state’s population, Connecticut stands out in one key area: an average of 68 SKUs per brand compared to the national average of 56. This suggests clear room for growth. As more brands and products enter the market, competition will increase, leading to greater product variety and ultimately driving prices to more attractive levels for consumers.

Pricing

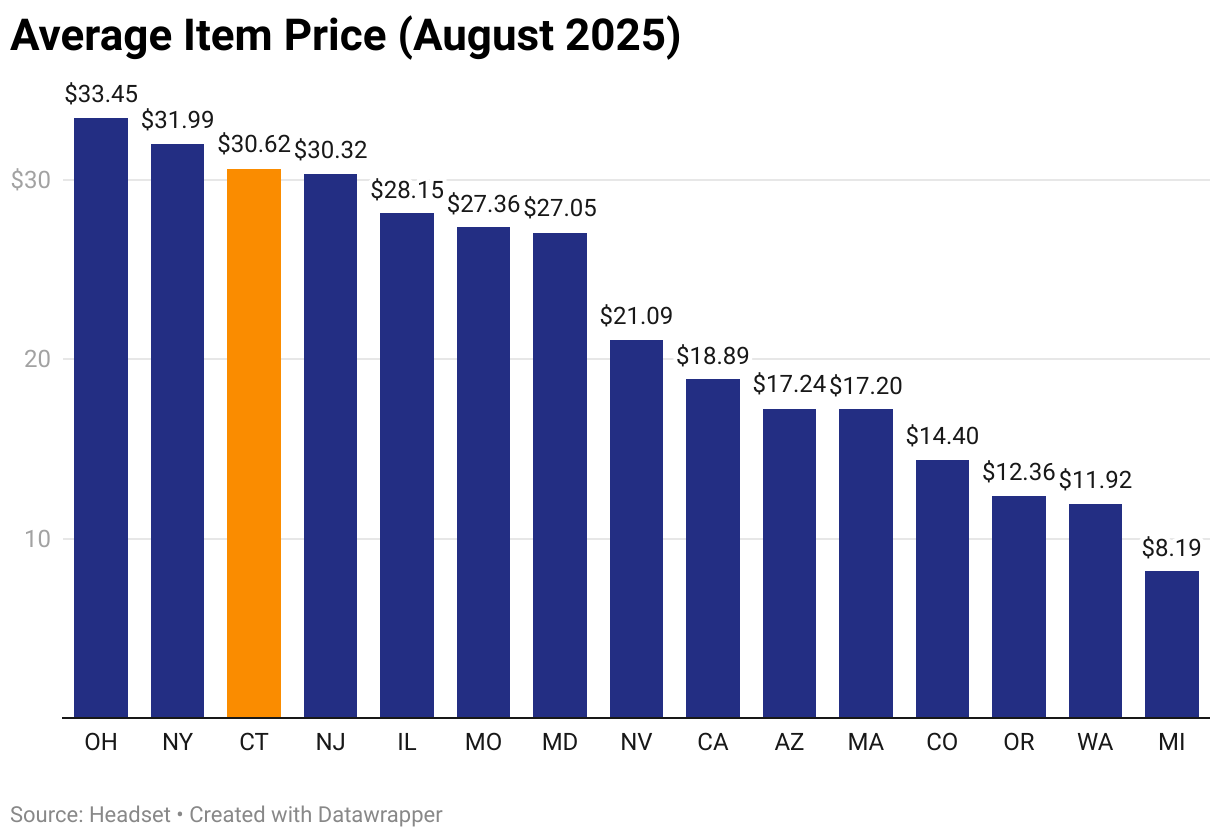

As is common in newer markets, Connecticut has some of the highest cannabis prices in the country, with an average item price of around $30. Bringing prices down to more competitive levels will be critical to keeping customers within the state and supporting the local market. Given Connecticut’s compact geography and the rapid expansion of cannabis access across the Northeast, operators will face stiff competition from neighboring states, as consumers have already shown a willingness to travel for better prices. While neighboring New Yorkers are paying even higher prices, Connecticut’s average item price remains nearly 80% higher than that of Massachusetts, just next door.

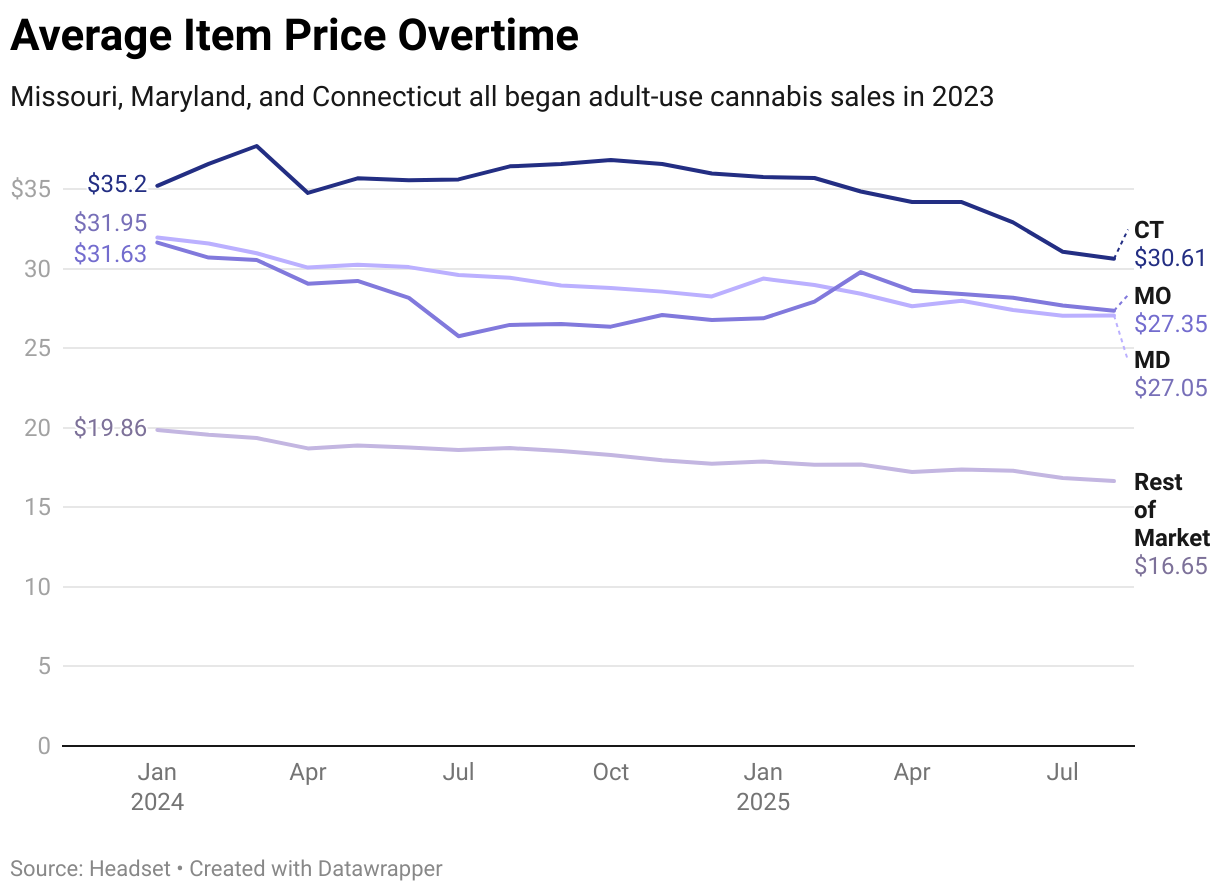

While prices in Connecticut remain higher than in some peer markets that launched around the same time, they have recently begun to decline at a meaningful pace. After holding steady, and even rising, throughout 2024, prices are now falling across most categories in 2025. On a year-over-year basis, the average item price in Connecticut is down 16%, compared to an 8% decline in Maryland, a 3.4% decline in Missouri, and an 11.1% decline across the U.S. overall.

Basket Analysis

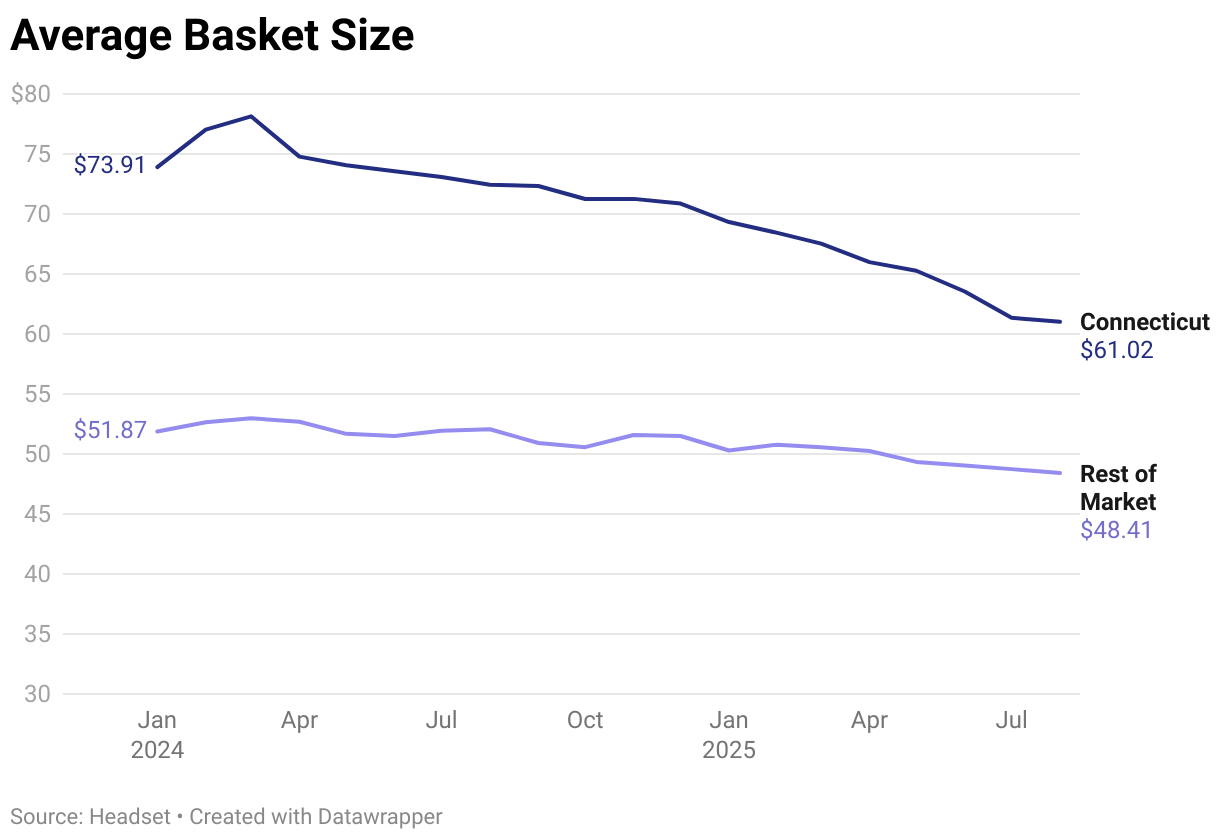

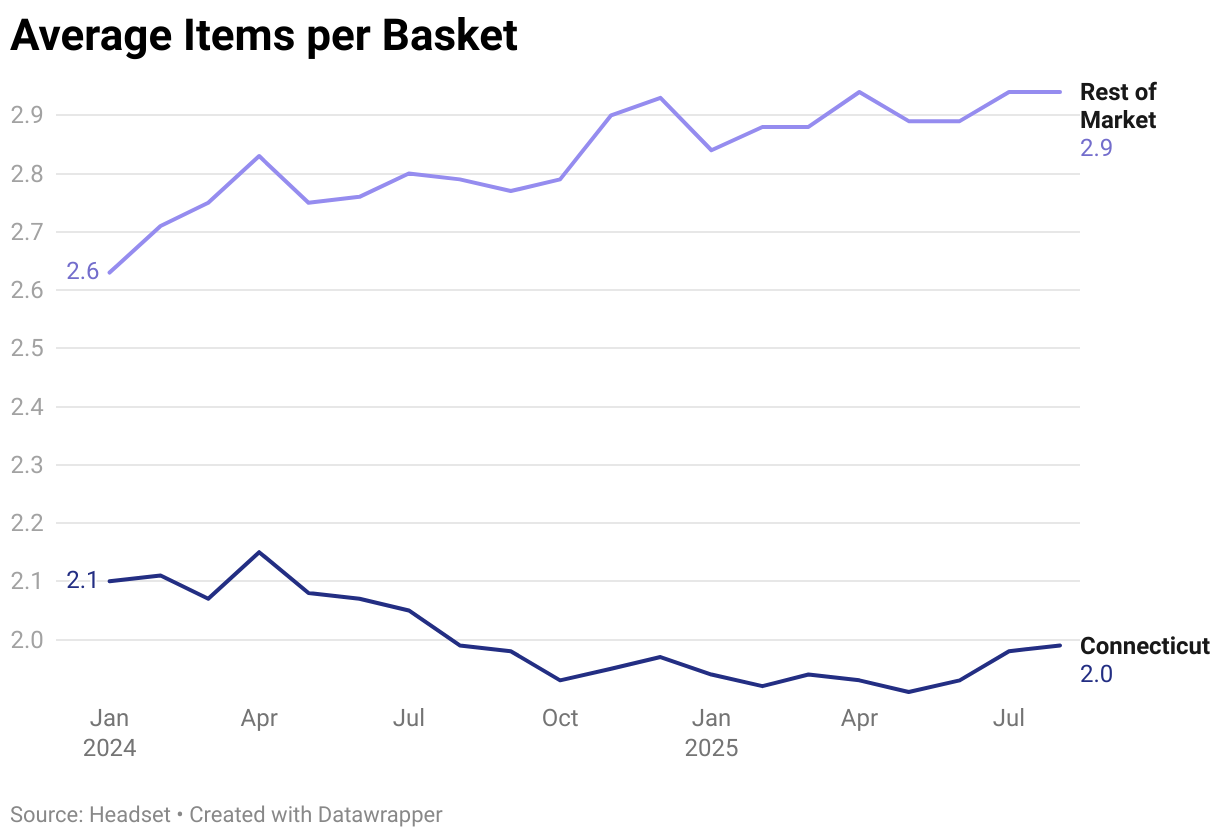

With a current average basket price of $62.02, Connecticut ranks in the top half of U.S. markets, compared to the national average of $52.22. However, this metric is closely tied to overall pricing. Higher prices naturally drive larger basket sizes, while declining prices lead to smaller average baskets. Although falling prices make the market more competitive and appealing to consumers, retailers must strike the right balance to maintain healthy and sustainable basket sizes over the long term.

Units per basket serve as the counterbalance to price. As prices fall and average basket values decline, more affordable pricing should ideally drive an increase in the number of items per basket. Nationally, the average is 2.7 items per basket, while in Connecticut it is just 2, among the lowest in the country. With prices falling significantly in 2025, we are beginning to see a reversal in purchasing trends, with consumers adding more items to their baskets. As the market becomes more price-competitive, retailers will want to monitor this metric closely as a way to offset reduced revenue per item.

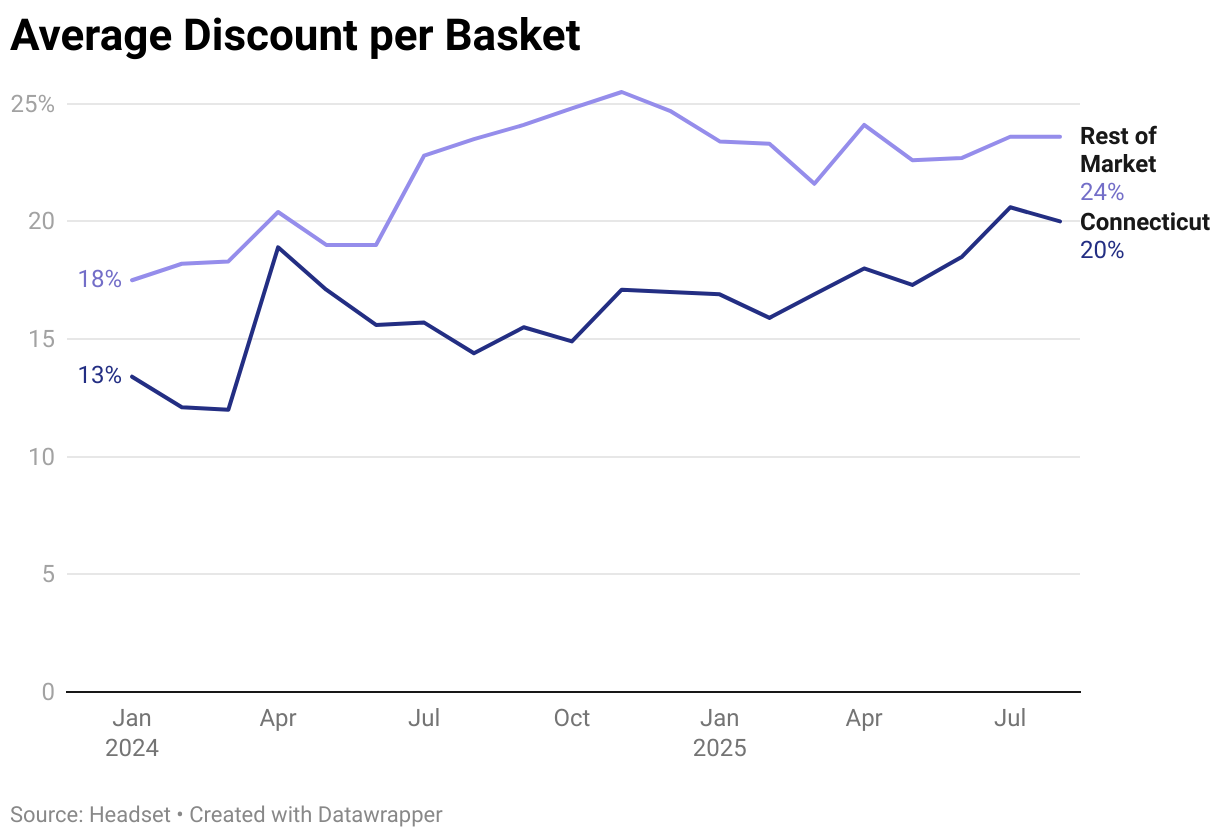

As of August 2025, Connecticut’s average discount rate stands at 20%, slightly below the national average of 23%. Discounting can be a powerful tool to upsell, cross-sell, and drive foot traffic in an increasingly competitive market. Across the U.S., discounting has escalated, with some markets averaging in the mid-to-high 30s as retailers compete aggressively for customers. While discounting in Connecticut remains at a relatively healthy level, the upward trend should be approached strategically to avoid eroding margins.

Demographics

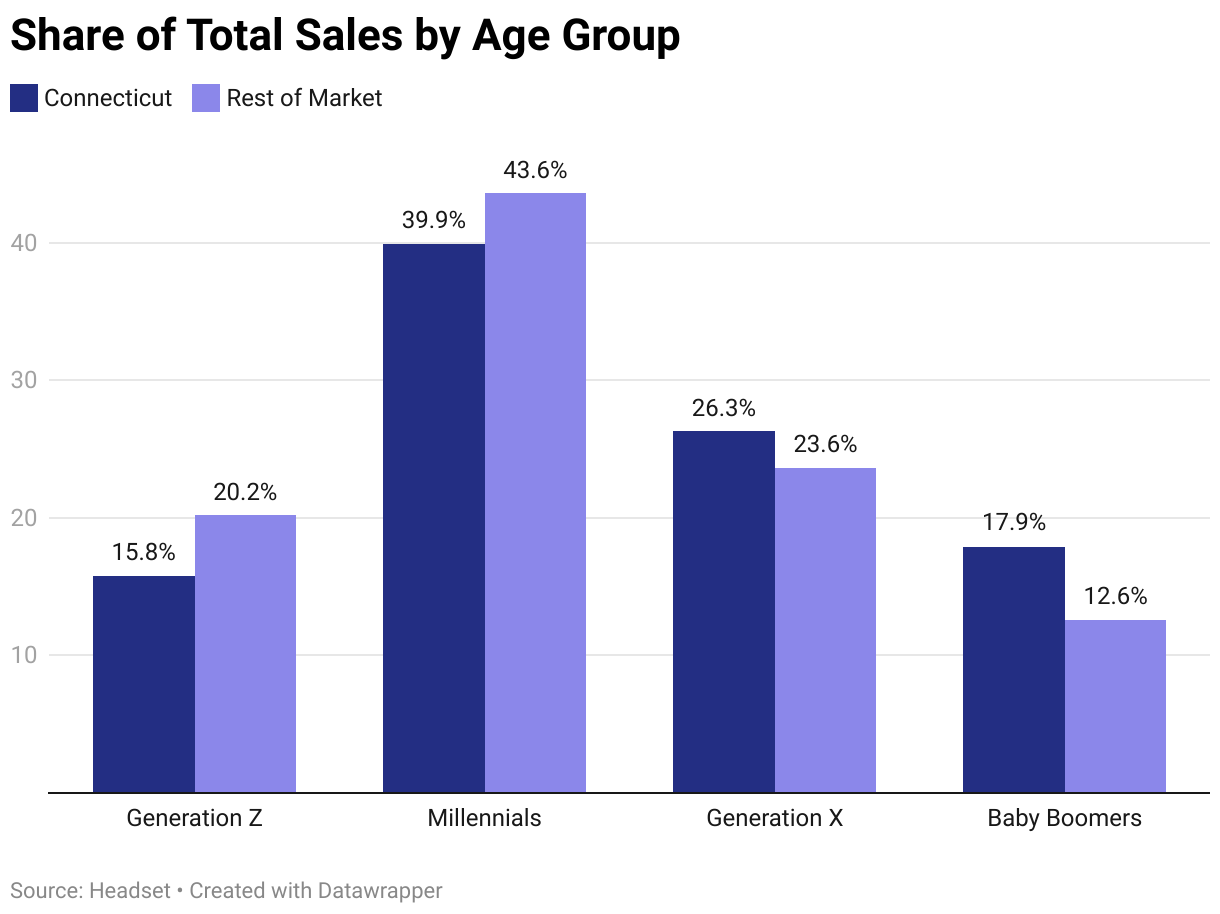

As in most markets, Millennials and men make up the largest share of cannabis consumers. However, the state stands out for its stronger skew toward older demographics, particularly Gen X and Baby Boomers. Across the U.S., these groups typically account for about 36% of total sales, but in Connecticut they represent 44%. Women are also slightly overrepresented in the state compared to the U.S. overall.

Conclusion

Connecticut’s adult-use cannabis market has been operating for just over two years and is already generating approximately $300 million annually in a state of only 3.5 million residents. Despite this strong revenue base, the market has gotten off to a relatively slow start, with flat year-over-year growth between 2024 and 2025 and historically high prices. Encouragingly, prices are now declining significantly, and more affordable products will help attract additional customers.

There remains considerable room for new brands to enter the market, which will further increase competition, expand product selection, and push prices down to more accessible levels. Greater variety and lower costs will also help Connecticut remain competitive with neighboring states, particularly Massachusetts, which is one of the region’s most developed cannabis markets and presents a potentially more robust and less expensive alternative for Connecticut consumers.

Regulatory dynamics are also shaping category performance, with rules hindering the growth of concentrates and beverages while supporting vapor pens and edibles. Additionally, Connecticut’s noticeably older consumer base presents a valuable opportunity for brands, as this demographic traditionally spends more per visit at dispensaries.

As this young market continues to mature, tracking its evolution against national trends will be essential for operators seeking to seize the significant opportunities ahead in both the state and the broader region.