Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Healer is stocked at 36 licensed dispensaries across Maryland and Maine, 22 of them in Maryland, with the deepest coverage in Baltimore, Annapolis, Upper Marlboro, Bethesda, and Bowie. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

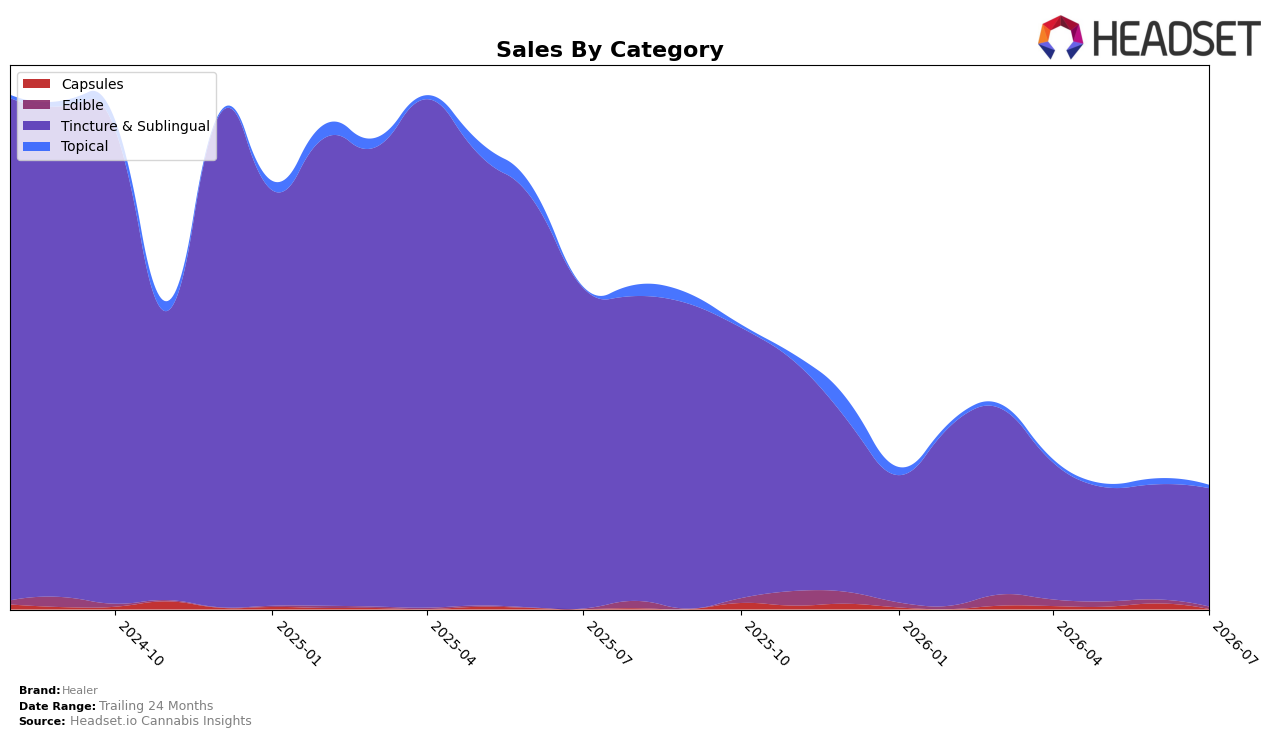

In July 2026, Healer’s mix is dominated by Tincture & Sublingual at 95.98% share, where sales fell 63.20% year over year but ticked up 2.75% month over month, while Topical holds 2.34% share with a 259.48% year-over-year jump yet a 47.82% month-over-month decline, and Edible at 1.68% share saw a 40.92% month-over-month pullback with no prior-year baseline. Despite average price rising 1.58% year over year to $28.75, the brand’s total sales declined 61.76% year over year, indicating that reliance on a single category with steep annual contraction outweighs minor month-over-month stabilization.

The category skew keeps Healer positioned as a Tincture-centric specialist, supported by a rank of 2 in Tincture & Sublingual in Maryland, but the 63.20% annual drop in that core alongside Topical’s 47.82% month-over-month retreat implies vulnerability to demand shocks within a narrow focus. With Edible shrinking 40.92% month over month and accounting for just 1.68% of sales, the current mix constrains cross-category insulation; the pattern implies Healer should either deepen defense where it ranks 2 or reallocate toward categories showing scalable share gains when month-over-month volatility subsides.

Competitive Landscape

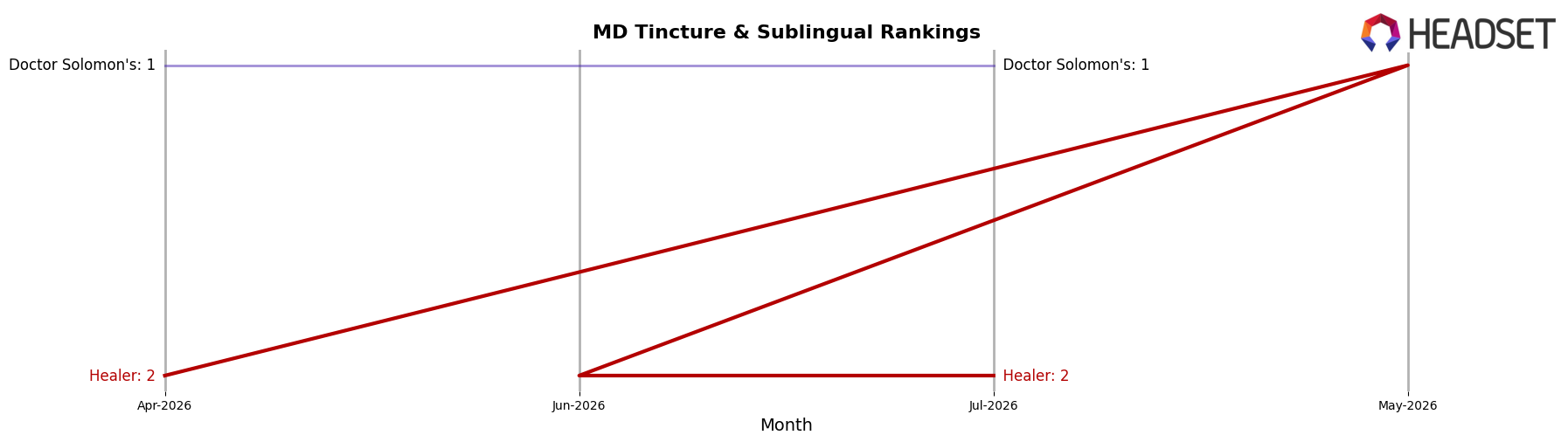

Healer sits at #2 in MD Tincture & Sublingual in July 2026 after a year-over-year drop of 1 rank, having previously peaked at #1 in May 2026, while holding #2 over the past three months and thus ceding the category lead it briefly captured; meanwhile, Doctor Solomon's holds #1 despite a -49.4% year-over-year sales change and a slip from #2 to #1 year-over-year positioning, and Cosmec Healing advanced from #5 to #4 alongside a 290.2% year-over-year sales surge that pressures the #3 spot currently held by Eastern Shore Extracts; the pattern implies Healer’s slight rank erosion from #1 to #2 creates vulnerability to faster movers, making retention of a top-two position contingent on countering competitors with triple-digit growth and capitalizing on the #1 brand’s steep decline.

Notable Products

THC/THCa 6:1 Night Tincture (600mg THC, 100mg THCA) posted the standout move in July 2026 with a 216.6% month-over-month surge and climbed into rank 4, while the legacy variant THC/THCa 6:1 Night Tincture (526.44mg THC, 99.96mg THCA) fell 36.4% to rank 5, indicating substitution within the same need-state. The flagship THC/THCA 1:1 Pain Relief Tincture (315.48mg THC, 327.12mg THCA) added 125.1% MoM to hold rank 1, contrasted by CBD Topical Hydrogel Cream (850mg CBD) dropping 64.4% to rank 10 with approximately $203 in sales. Four of the top ten are Uplift family or 4:1 SKUs clustered at ranks 2, 6, 7, and 8, with the 4:1 Uplift Tincture (100mg THC, 25mg THCA) up 50.5% at rank 2 while the 480mg format dipped 3.4% at rank 6, implying format and dose are steering choice more than flavor or label. The pattern points to Healer consolidating around THC-forward nighttime and 1:1 relief solutions while de-emphasizing non-tincture topicals, suggesting a pivot toward potency-tiered tincture depth over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.