Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Wyld is stocked at 4,180 licensed dispensaries across California, Michigan, and 21 other states, 853 of them in California, with the deepest coverage in Los Angeles, Sacramento, San Francisco, San Diego, and Long Beach. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

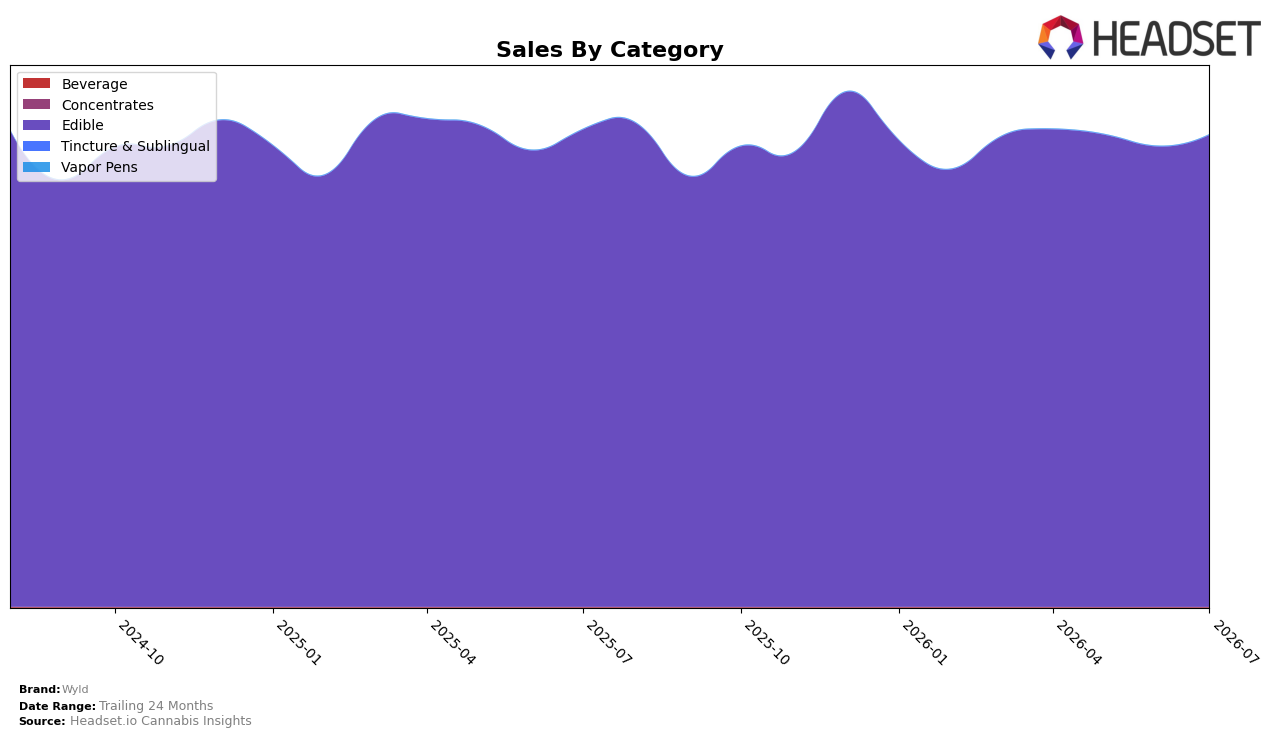

In July 2026, Wyld’s mix remained concentrated in Edible at 99.95% share, with Edible sales down 1.13% year over year but up 2.52% month over month, while Beverage held 0.05% share with a 7.95% year-over-year decline and a 5.00% month-over-month gain. Tincture & Sublingual contracted to 0.001% share with a 57.79% year-over-year drop and a 43.53% month-over-month decline, as the brand’s overall sales slipped 1.14% year over year alongside a 7.52% year-over-year increase in average price; the implication is a continued deepening in a single-category footprint, with small-format adjacency tests not converting to durable share.

That concentration aligns with Wyld’s #1 rank in Edible in Arizona, but the 2.52% month-over-month lift in Edible versus a 5.00% month-over-month uptick in Beverage suggests upside is still anchored in core gummies rather than in cross-category expansion, especially given Beverage’s 7.95% year-over-year decline. With average price up 7.52% year over year alongside a 1.13% year-over-year contraction in Edible sales, the pattern points to price-led value capture within Edible and diminishing elasticity headroom in non-core formats, indicating that near-term positioning remains premium-leaning within Edible while adjacencies require re-specification rather than scale.

Competitive Landscape

Wyld holds rank #1 in CA Edible in July 2026, unchanged from #1 in July 2025, while maintaining #1 over the last three months and peaking at #1 in July 2026; in contrast, Camino sits at #2 with a 14.8% year-over-year sales increase yet did not shift rank, and Kanha / Sunderstorm remains #3 with a 14.6% year-over-year lift without rank movement. With Lost Farm steady at #4 on 12.8% year-over-year growth and Good Tide at #5 despite a 22.1% year-over-year increase, the lack of rank change across the top five suggests Wyld’s #1 position is insulated by a stable leaderboard where competitor growth is not translating into share displacement; this trajectory implies Wyld’s lead is entrenched unless a competitor converts double-digit growth into rank gains.

Notable Products

CBD/THC 20:1 Hybrid Strawberry Gummies 20-Pack (200mg CBD, 10mg THC) posted the standout move with a +6.03% month-over-month gain while holding rank 8, compared with the top-ranked CBD/CBN/THC 1:1:1 Indica Boysenberry Gummies 10-Pack (100mg CBD, 100mg CBN, 100mg THC) at +2.51% and Sativa Sour Apple Gummies 10-Pack (100mg) at +2.65%. Hybrid Huckleberry Gummies 10-Pack (100mg) advanced +4.43% at rank 7 as Sativa Raspberry Gummies 10-Pack (100mg) slipped -0.58% at rank 3, indicating momentum is concentrated in hybrid and CBD-leaning SKUs rather than core sativa fruit flavors. With eight of the top ten in Edible gummies and only one product showing a decline under -1%, the mix tilts toward diversified cannabinoid ratios that can expand basket roles and de-risk reliance on single-flavor sativa lines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.