Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Ozone is stocked at 447 licensed dispensaries across Illinois, New Jersey, and 6 other states, 175 of them in Illinois, with the deepest coverage in Chicago, Normal, East Peoria, Naperville, and Peoria. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

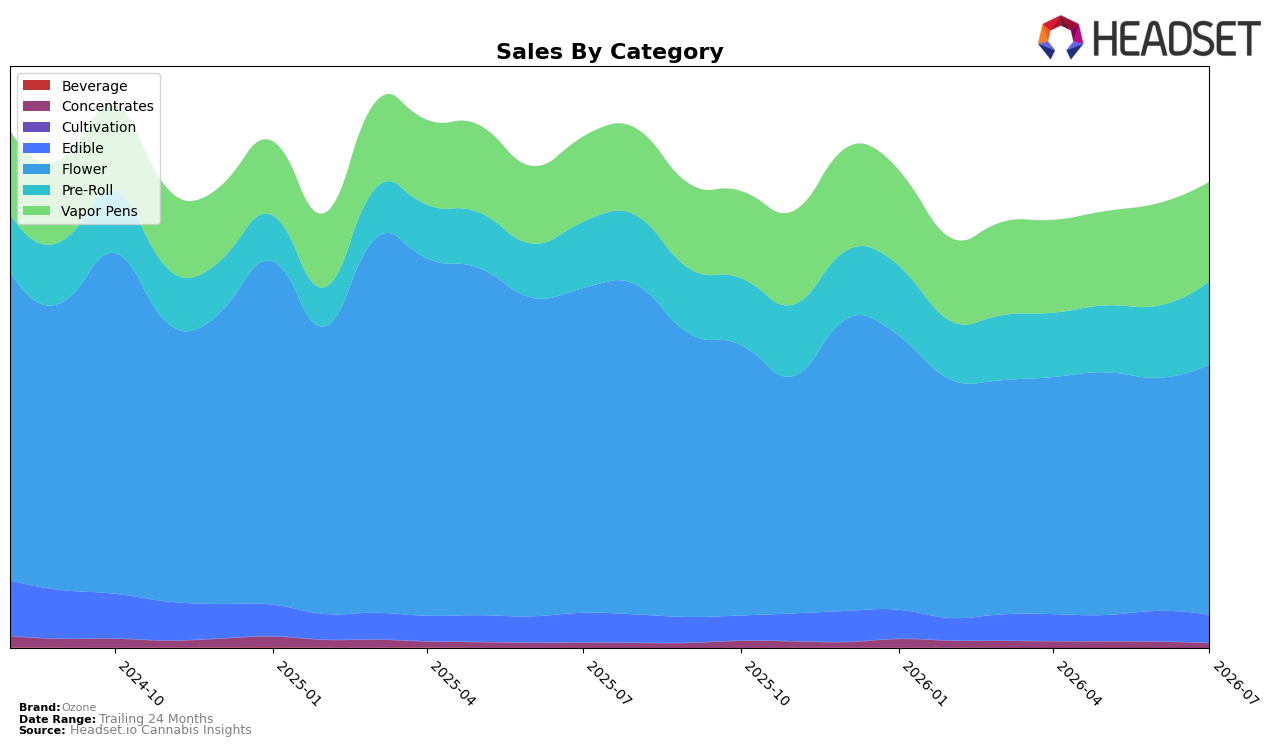

Ozone’s mix in July 2026 tilted further into Flower at 53.93% share despite a 22.83% year-over-year decline in that category and a 7.50% month-over-month lift, while Pre-Roll climbed to 17.85% share on 25.65% YoY growth and a 15.58% MoM increase. Vapor Pens held 21.32% share with 16.57% YoY growth but slipped 3.05% MoM, and Edible at 5.94% contracted 5.61% YoY and 8.41% MoM as Concentrates fell to 0.96% share with an 8.10% YoY decline and a 24.07% MoM drop. With Ozone ranked 1 in Flower in New Jersey and an average price down 15.37% YoY to $24.95, the mix suggests price-led defense in a flagship category coupled with a shift toward faster-growing Pre-Roll to offset Flower’s annual contraction.

The pattern implies Ozone is anchoring its positioning around Flower leadership in New Jersey (rank 1) while broadening demand capture through value-accessible formats: Pre-Roll’s 25.65% YoY and 15.58% MoM gains point to acquisition and frequency, whereas Vapor Pens’ 16.57% YoY growth but 3.05% MoM dip indicates sensitivity to short-cycle pricing or promo cadence. Given brand sales down 8.87% YoY alongside a 3.05% decline over 24 months, the combination of a 15.37% lower average price and a rising Pre-Roll mix signals a deliberate trade toward volume retention and entry points, implying that sustaining Flower rank while stabilizing MoM in Vapor Pens will determine whether the mix shift converts into share defense rather than margin dilution.

Competitive Landscape

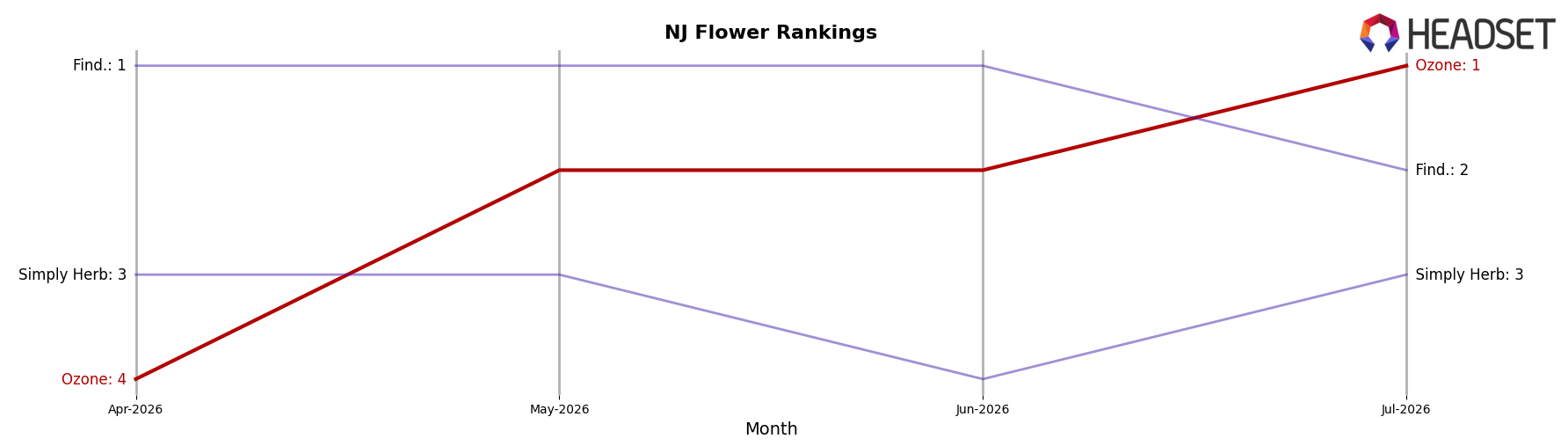

Ozone is currently ranked #1 in New Jersey Flower, up 1 position from #2 year over year and rising 3 spots from #4 in April 2026 to peak at #1 in July 2026, indicating acceleration rather than a one-off jump; meanwhile, Find. advanced from #10 to #2 with 128.97% YoY sales growth and Simply Herb moved from #6 to #3 with 35.87% YoY growth, so Ozone’s climb to #1 alongside faster-chasing rivals implies a tightening leaderboard where maintaining the top rank will hinge on defending recent share gains against upward momentum below.

Notable Products

Rainbow Chip Pre-Roll (1g) delivered the standout move in July 2026 with a 132.6% month-over-month surge, rising to rank 2, while Butterstuff Pre-Roll (1g) also climbed on an 81.7% gain to hold rank 1. Happy Hour #21 Pre-Roll (1g) added a 54.5% MoM lift at rank 4, whereas Garlic Cookies Pre-Roll (1g) slipped 6.0% at rank 7, and six of the top ten SKUs were Pre-Rolls, indicating a concentrated tilt toward ready-to-smoke formats. Butterstuff Popcorn (7g) at rank 5 advanced 16.6% MoM and remains the lone Flower SKU with scale at $302,939, pointing to a secondary role for Flower behind Pre-Rolls in near-term velocity. The pattern implies Ozone is leaning into Pre-Roll breadth to drive share, using a few Flower anchors to stabilize volume while newer Pre-Roll variants accelerate.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.