Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

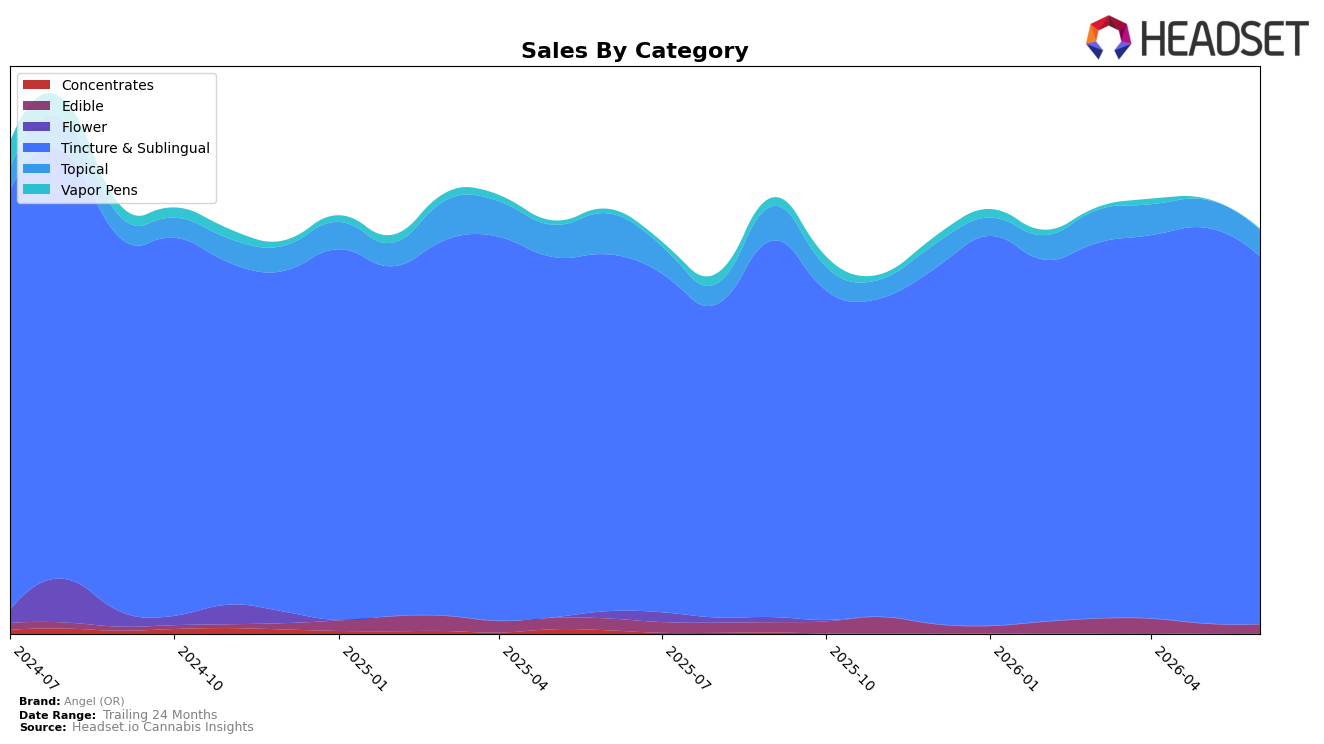

Angel (OR) in Oregon remained heavily concentrated in Tincture & Sublingual, holding a 91.07% share with 3.03% year-over-year growth but a 7.10% month-over-month decline in June 2026; by contrast, Topical accounted for 6.45% share with a 35.96% year-over-year drop and a 6.23% month-over-month decline. Smaller lines moved in opposing directions: Edible held 2.23% share with a 21.41% year-over-year contraction and a 7.32% month-over-month decline, while Vapor Pens sat at 0.25% share with a 75.03% year-over-year decline but a 21.65% month-over-month uptick. With total brand sales down 4.66% year over year and average price up 0.14%, the pattern implies category concentration is cushioning annual erosion in the core while near-term softness within Tincture & Sublingual is suppressing monthly momentum.

The mix shifts suggest Angel (OR) is anchored to a leadership position in Tincture & Sublingual, where it ranks 1 in Oregon, but exposure risk is elevated as 91.07% of sales depend on a category that just fell 7.10% month over month; the 21.65% monthly lift in Vapor Pens offers a testable hedge despite a 75.03% year-over-year decline and 0.25% share. Given the 35.96% year-over-year decline in Topical and 21.41% year-over-year decline in Edible, the data imply that near-term share defense is best achieved by stabilizing Tincture & Sublingual pricing and mix while selectively nurturing Vapor Pens as an option to offset future monthly volatility without diluting the brand’s category identity.

Competitive Landscape

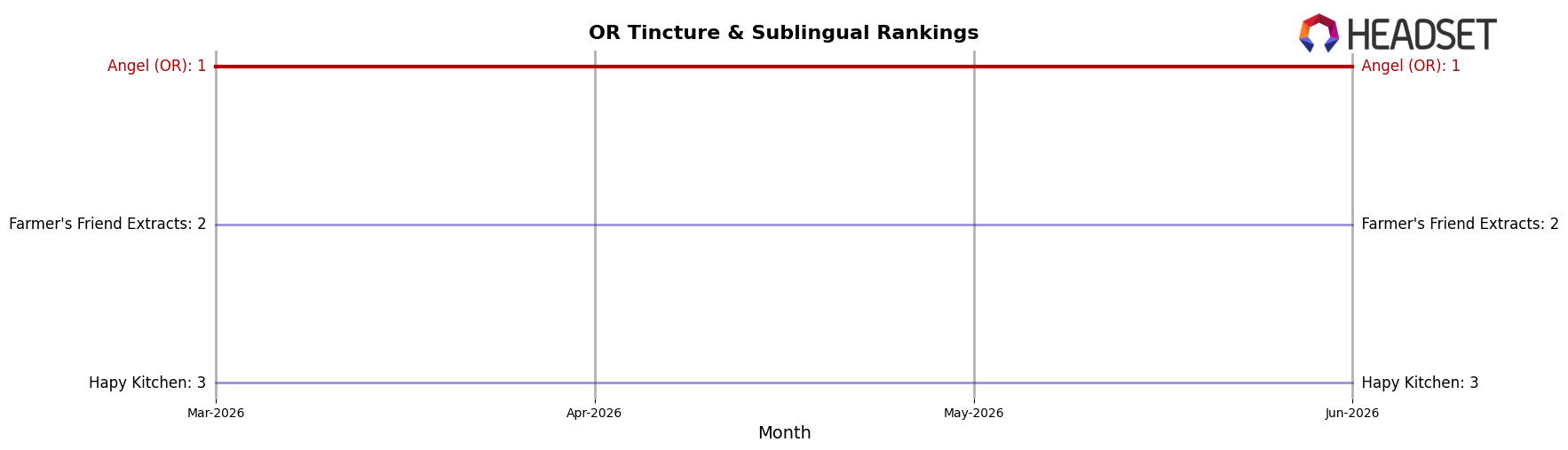

Angel (OR) holds rank #1 in Oregon Tincture & Sublingual for June 2026 with a 0-place YoY rank change, sustaining #1 since April 2026 and remaining #1 versus March 2026, while Farmer's Friend Extracts sits at #2 after improving from #3 year over year with a 28.6% YoY sales lift and Hapy Kitchen declined from #2 to #3 despite a 7.5% YoY sales increase; meanwhile, High Desert Pure held steady at #4 with 29.5% YoY growth and Crown B Alchemy advanced from #7 to #5 with 22.8% YoY growth, indicating that Angel (OR)’s unchanged #1 amid competitors’ upward mobility signals durable category leadership rather than a soft field.

Notable Products

THC Unflavored Tincture (1000mg) posted the steepest movement in June 2026 with a -55.6% month-over-month drop while holding rank 2, contrasting with Indica Tincture (1000mg) at rank 1 slipping a milder -8.1%. CBD Flavorless Hemp Tincture (1500mg CBD, 30ml) surged +62.2% to rank 6, and Limeade Blossom Gummy (100mg) jumped +62.8% to rank 8, yet tinctures occupy eight of the top ten positions, indicating category concentration outweighs isolated edible gains. The CBD/THC/CBN/CBG 1:1:1:1 Rainbow Children Tincture (1000mg CBD,1000mg THC, 1000mg CBN, 1000mg CBG, 1oz) advanced +16.9% at rank 3, and CBD Flavorless Hemp Tincture (3000mg CBD, 30ml) added +7.4% at rank 4, while CBD/THC 1:1 Flavorless Hemp Tincture (1000mg CBD,1000mg THC, 30ml) declined -24.1% at rank 7, signaling a tilt toward higher-dose CBD-only or multi-cannabinoid formats over 1:1 blends. This pattern implies Angel (OR) is consolidating around tincture-led volume with selective momentum in CBD-heavy and multi-cannabinoid SKUs, using a single edible uptick as a secondary testing lane rather than a mix shift.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.