Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

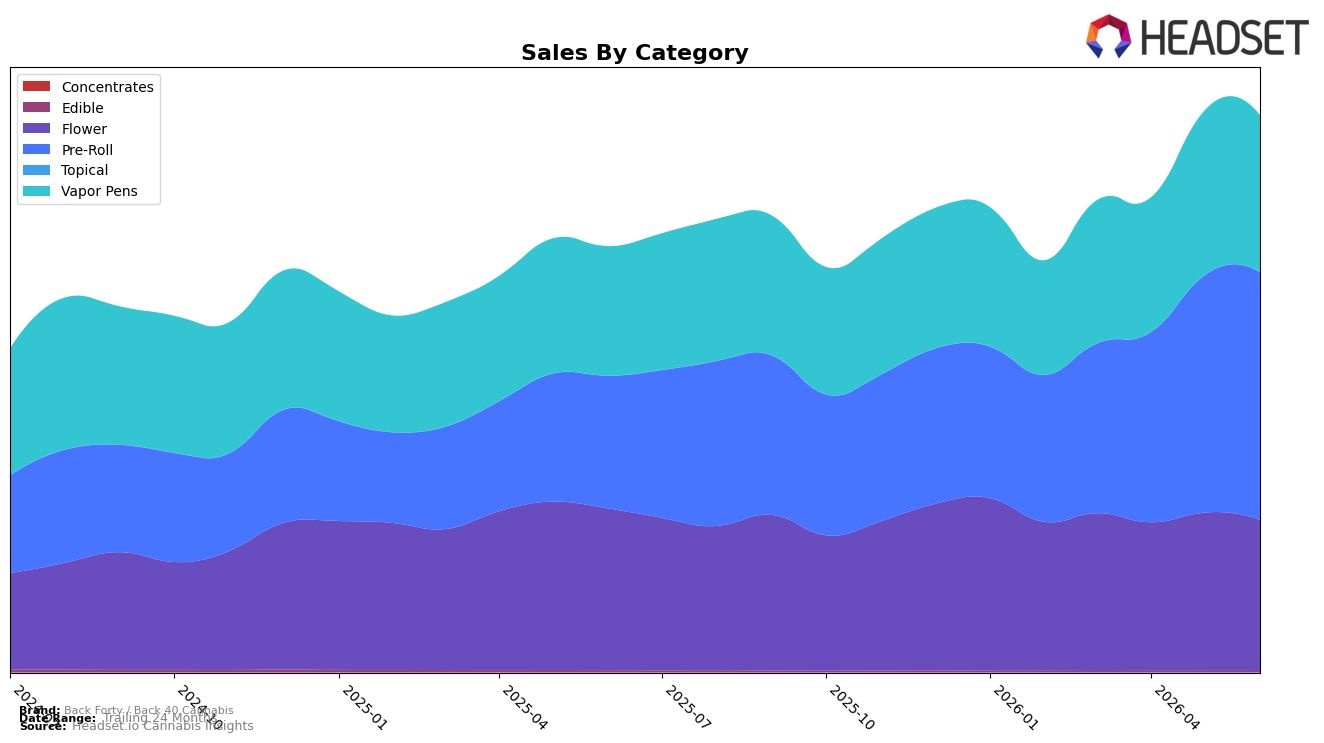

Back Forty / Back 40 Cannabis shifted decisively toward Pre-Roll in June 2026, with Pre-Roll holding 44.45% share and growing 86.58% year over year while rising 4.29% month over month, versus Vapor Pens at 28.20% share with 21.40% YoY growth but a -4.68% MoM decline. Flower contracted to 27.13% share with -6.59% YoY and -4.56% MoM, and Edible remained minimal at 0.21% share with -40.44% YoY and -3.43% MoM. Average price across the brand eased -0.52% YoY to $33.30 as the leading Pre-Roll average price sat at $26.11 relative to Flower at $62.01, and within Ontario the brand holds rank 1 in Pre-Roll. The mix now concentrates volume in a lower-priced, faster-growing Pre-Roll core while Vapor Pens and Flower recede or stagnate, implying the brand is consolidating demand where price-accessible formats deliver outsized growth.

The combination of an 86.58% YoY surge and a 4.29% MoM uptick in Pre-Roll alongside a -4.68% MoM decline in Vapor Pens and a -4.56% MoM decline in Flower signals a pivot toward value-led inhalables, aided by the $26.11 Pre-Roll price point versus $62.01 for Flower. Rank 1 in Pre-Roll within Ontario plus a -0.52% YoY brand-wide price move suggests volume-led share capture rather than premium trading-up, and the 0.21% Edible share with -40.44% YoY indicates limited diversification upside. This pattern implies positioning as a scale Pre-Roll specialist that leverages price-to-THC and multi-pack formats to defend and expand share while de-emphasizing slower or shrinking segments.

Competitive Landscape

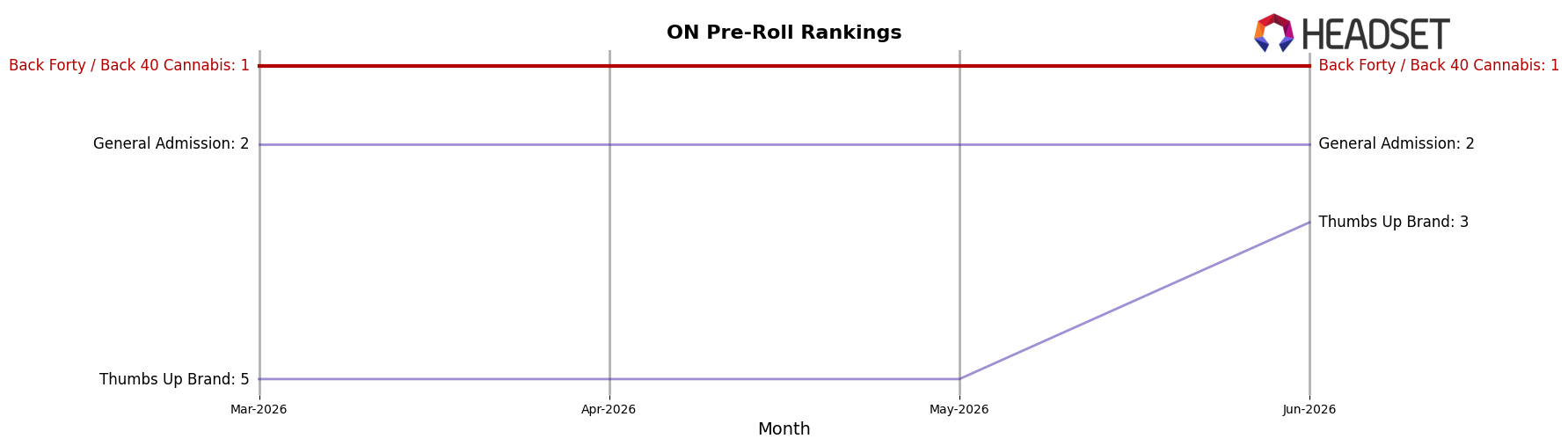

Back Forty / Back 40 Cannabis sits at rank #1 in ON Pre-Roll in June 2026, up two positions from #3 year over year, marking a peak at #1 in June 2026 while holding #1 over the last three months; meanwhile, General Admission fell from #1 to #2 as its year-over-year sales declined 17.9%, and Jeeter sits at #4 with a 48.5% year-over-year sales drop, whereas Thumbs Up Brand advanced to #3 alongside a 53.6% year-over-year sales increase. The rank ascent of Back Forty / Back 40 Cannabis alongside competitor declines of 17.9% and 48.5% suggests the brand’s #1 position is being reinforced by rivals ceding share, though the 53.6% growth at #3 indicates pressure from below that will test the durability of its leadership.

Notable Products

Liquid Imagination Pre-Roll 10-Pack (3.5g) posted the steepest decline at -70.7% month over month while still holding rank 1, and Kush Mint Distillate Cartridge (1g) fell -10.7% at rank 10, indicating a bifurcation between flagship pre-rolls and trailing vapor pens. Meanwhile, Lemon Diesel Pre-Roll 10-Pack (3.5g) and Liquid Imagination Pre-Roll 10-Pack (7.5g) rose +501% and +7.1% respectively at ranks 2 and 4, and five of the top six spots are Pre-Roll SKUs, concentrating share in multi-pack formats; this implies a deliberate pivot toward high-frequency, value-oriented pre-roll packs even as select SKUs reset. With Peach Lemonade Distillate Disposable (0.95g) up +15.9% at rank 7 against a -10.7% decline for Kush Mint at rank 10, vapor pens are mixed but secondary to pre-roll momentum; the $1,609,045 result for Liquid Imagination Pre-Roll 10-Pack (7.5g) reinforces scale in larger pack sizes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.