Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

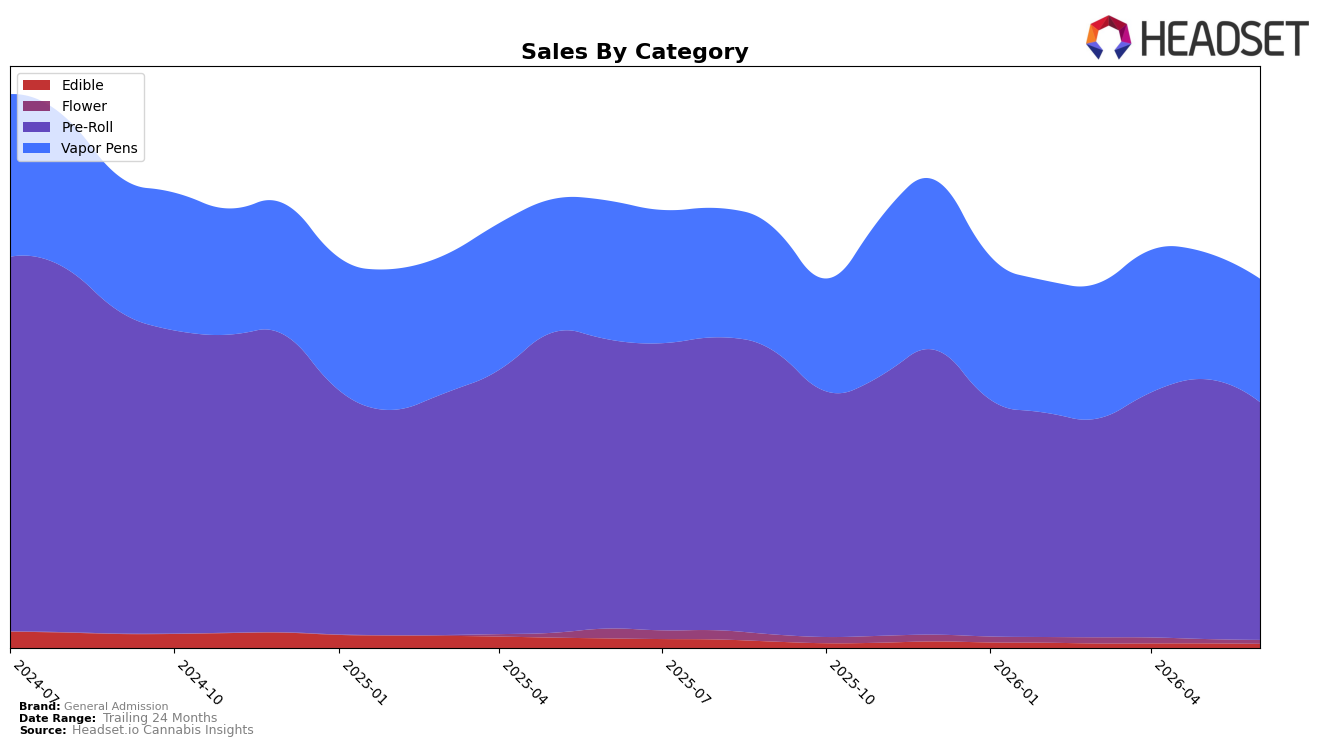

In June 2026, General Admission remained concentrated in Pre-Roll at 64.53% share while Vapor Pens held 33.47%, a 31.06 percentage-point spread that narrows or widens depending on relative declines. Pre-Roll contracted faster month over month at -8.52% versus Vapor Pens at -2.80%, and year over year at -17.81% versus -11.07%, while minor lines like Edible and Flower fell -10.24% and -11.41% MoM respectively. Against a brand-level sales change of -17.51% YoY and an average price up 6.51%, the mix skew toward Pre-Roll magnifies volume sensitivity, implying that June 2026 performance is primarily dictated by Pre-Roll elasticity and that incremental stabilization in Vapor Pens could buffer near-term volatility.

The mix and rank context point to positioning trade-offs: holding the number 1 rank in Pre-Roll in Alberta alongside a -17.81% Pre-Roll YoY decline suggests leadership is anchored in a contracting core while secondary exposure to Vapor Pens, down -11.07% YoY, provides a slower-declining lane. With Pre-Roll average price at 29.02 versus Vapor Pens at 36.10 and an overall June 2026 average price of 29.64, the brand is clustered near value tiers where small price shifts can move share, and the -8.52% MoM drop in Pre-Roll versus -2.80% in Vapor Pens implies that incremental emphasis on the latter could lift mix resilience without abandoning the Alberta Pre-Roll leadership position.

Competitive Landscape

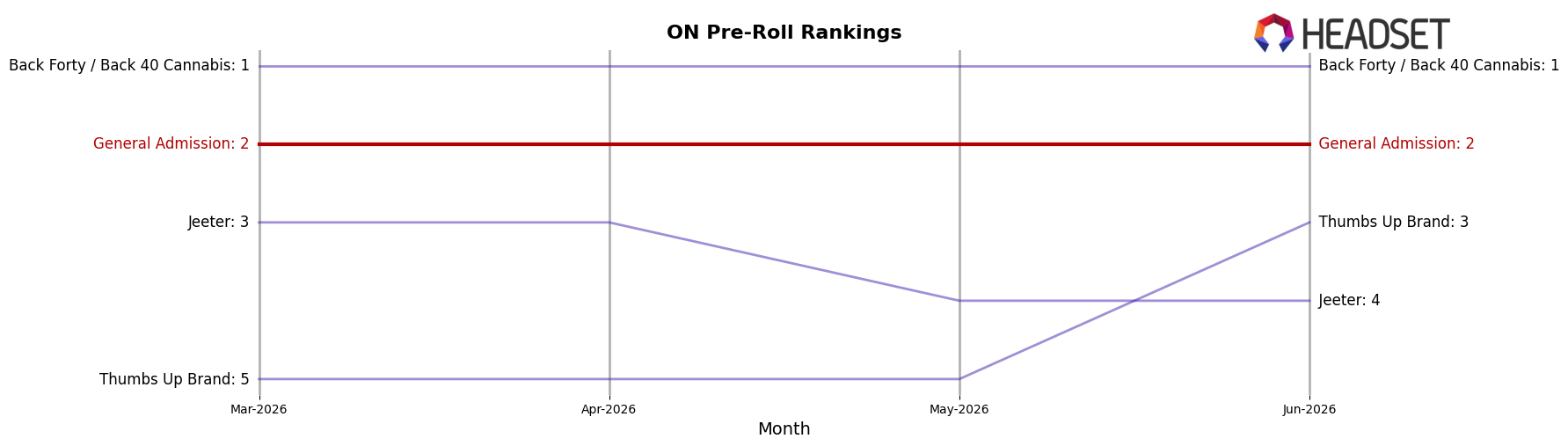

General Admission ranks #2 in ON Pre-Roll in June 2026, down 1 position year over year from #1, while holding flat versus March 2026 at #2; the brand’s peak at #1 in December 2025 contrasts with Back Forty / Back 40 Cannabis advancing from #3 to #1 year over year (+2 ranks) and Thumbs Up Brand rising from #8 to #3 (+5 ranks), indicating that faster YoY momentum from leaders above and challengers below compresses headroom even as General Admission remains top-two, implying the trajectory points to a defend-or-recapture fork where sustaining #2 requires countering upward moves from #3 and reclaiming #1 requires displacing a competitor that gained two ranks.

Notable Products

Purple Stuff Hi-Fi Diamond Distillate Infused Pre-Roll 5-Pack (2.5g) posted the steepest movement in June 2026 with a -24.1% month-over-month drop while holding rank 8, a sharper slide than the -7.7% on Tiger Blood Distillate Infused Pre-Roll 3-Pack (1.5g) at rank 3 and the -7.3% on Tiger Blood Liquid Diamond Disposable (1g) at rank 4. In contrast, Tiger Blood Distillate Infused Pre-Roll 5-Pack (2.5g) inched up +5.3% and remained rank 1, and Tiger Blood Distillate Infused Pre-Roll (1g) gained +5.9% at rank 2, indicating the Tiger Blood line is consolidating share at the very top while mid-pack variants soften. Eight of the top ten are Pre-Roll SKUs, and that category concentration alongside a -9.6% decline for Tiger Blood Chews 2-Pack (10mg) at rank 9 signals a portfolio skew toward inhalables rather than edibles. The pattern implies General Admission is leaning into a flagship Pre-Roll franchise with incremental premium-trim volatility, suggesting resources are best allocated to sustaining the leading Tiger Blood formats while tightening underperforming multi-pack and Hi-Fi variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.