Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

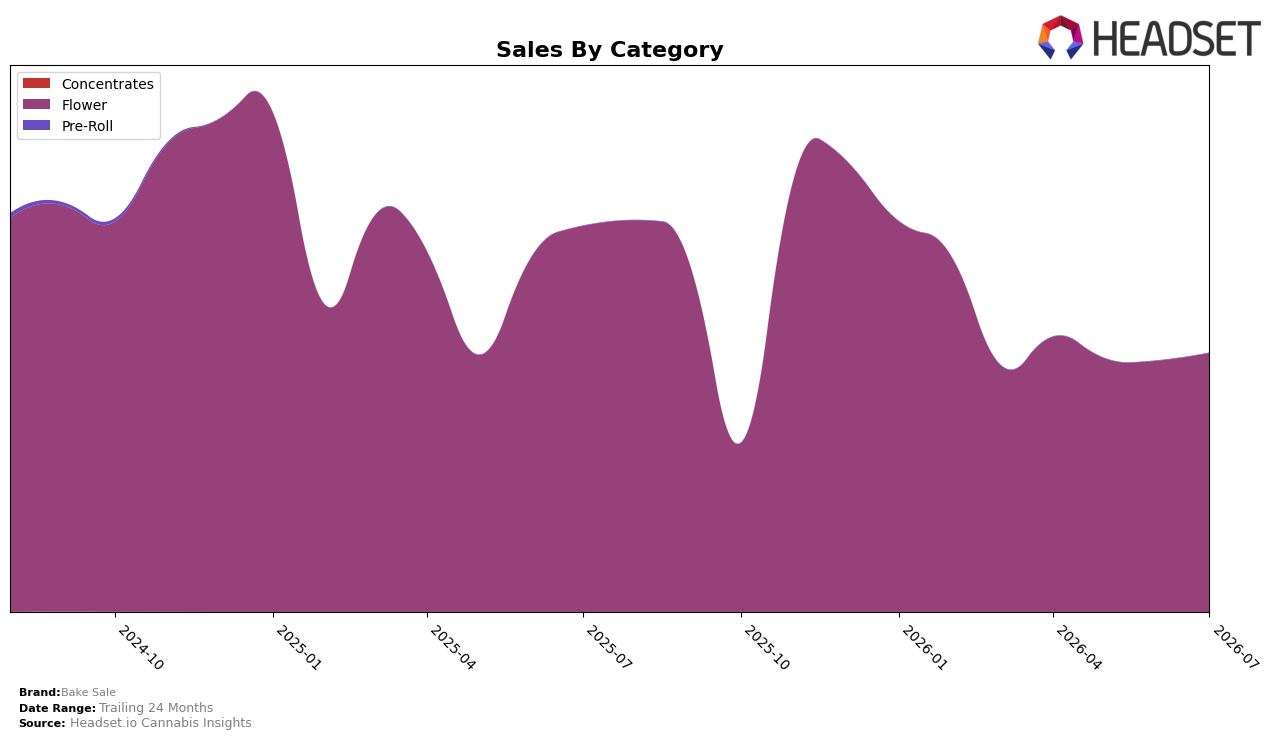

In July 2026, Bake Sale operated as a single-category brand with Flower at 100.0% of mix, pairing a year-over-year sales change of -32.9% with a month-over-month uptick of 3.1%. Average price rose 8.6% YoY while total brand sales fell -32.9% YoY, and the brand held rank 5 in Flower within British Columbia. The pattern implies a concentrated bet on Flower that lifted short-term momentum but left the overall YoY trajectory pressured by price-led elasticity and category exposure.

With all revenue tied to Flower, the 3.1% MoM lift alongside a -32.9% YoY decline suggests sequential gains are not yet offsetting the longer-cycle contraction, even as July 2026 pricing sits 8.6% above last year. Maintaining rank 5 in Flower in British Columbia while average price increased indicates pricing power without share diversification, implying Bake Sale’s positioning relies on defending a premium-per-ounce stance rather than expanding into adjacent categories to buffer volatility.

Competitive Landscape

Bake Sale sits at rank #5 in BC Flower in July 2026, down 2 positions year over year from #3, and up 1 place from #6 three months ago; the brand last peaked at #1 in December 2025, indicating a 4-place slide from that peak while competitors shuffled upward. Good Supply advanced from #6 to #2 alongside a 42.9% YoY sales increase, and Spinach moved from #5 to #3 with a 25.4% YoY lift, while The Original Fraser Valley Weed Co. slipped from #1 to #4 with a 23.9% YoY decline; Big Bag O' Buds rose from #2 to #1 with a 6.4% YoY gain, tightening competition at the top. The pattern implies Bake Sale’s trajectory is stabilizing but ceding share to faster-rising rivals, and without a catalyst to reverse a 2-rank YoY decline, the path back toward its December 2025 peak looks constrained by competitors’ upward momentum.

Notable Products

All Purpose Flower Indica (28g) posted the standout move in July 2026 with a +21.9% month-over-month lift to rank #2, while All Purpose Flower Sativa (28g) slipped -7.7% MoM yet held #1. Two Flower SKUs account for the entire top ten set for Bake Sale this month, concentrating share at ranks #1 and #2 and compressing variety within the lineup. With the leading SKU declining -7.7% alongside a +21.9% surge in its sibling, the mix points to intra-portfolio substitution within the Flower family rather than category expansion, implying a focus on defending high-volume formats over broadening assortment.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.