Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

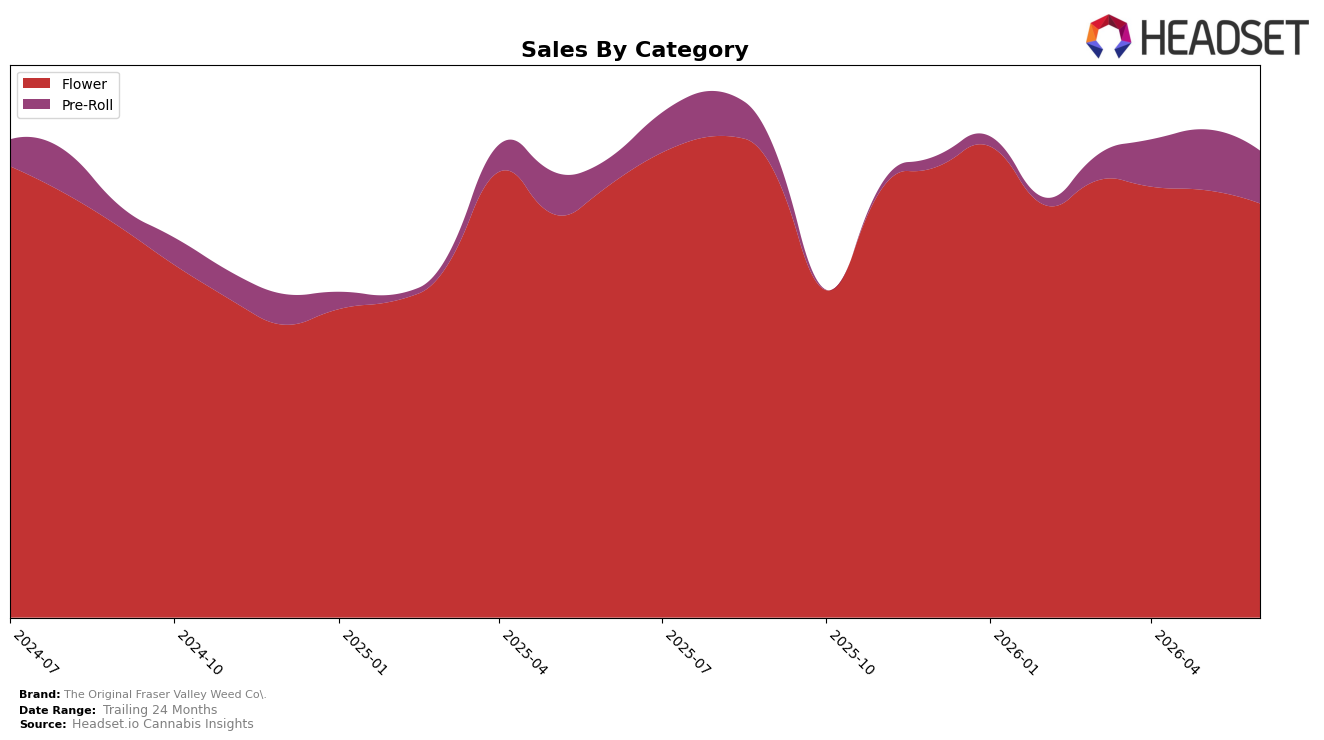

In June 2026, The Original Fraser Valley Weed Co. leaned further into a two-category profile where Flower held 78.92% share and Pre-Roll carried 21.08%, with Flower down 3.42% year over year and 2.64% month over month while Pre-Roll rose 24.04% year over year but fell 5.63% month over month. Despite brand-level sales up 1.31% year over year and an average price decline of 12.45%, the mix still concentrated in Flower at an average price of $88.75 versus Pre-Roll at 27.35, implying that June 2026 growth relied on price accessibility and Pre-Roll elasticity rather than volume expansion in Flower; the pattern suggests a cautious rebalancing toward Pre-Roll while guarding a Flower anchor.

The category tilt, combined with a Flower rank of 4 in British Columbia, indicates the brand’s positioning rests on premium-leaning Flower scale while using lower-priced Pre-Rolls to buffer volatility; the 2.64% month-over-month Flower dip alongside a 5.63% Pre-Roll dip signals exposure to short-term demand shocks across both pillars. With overall sales up 5.62% over 24 months but current gains just 1.31% year over year, the mix points to a need to convert Pre-Roll’s 24.04% annual growth into sustained share lift from 21.08% while mitigating the Flower share drag at 78.92%; the implication is to defend top-quartile Flower rank positioning by price-pack architecture while allowing Pre-Roll to carry incremental trial.

Competitive Landscape

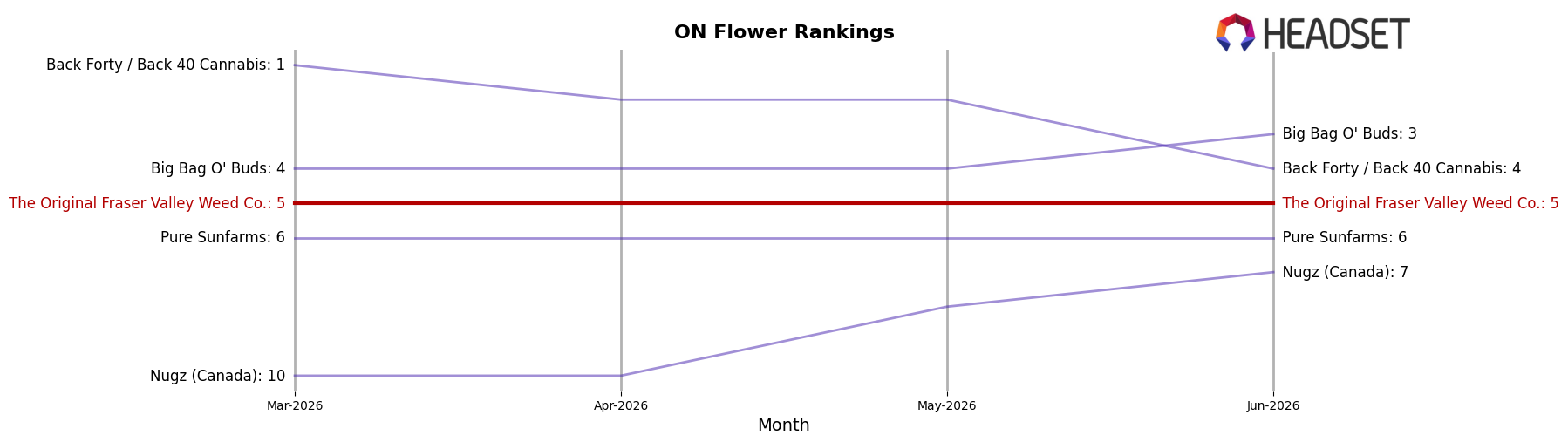

The Original Fraser Valley Weed Co. ranks #5 in ON Flower in June 2026, improving 3 positions from #8 year over year, while holding flat versus March 2026 at #5; this stability contrasts with Back Forty / Back 40 Cannabis sliding from #1 to #4 and with Spinach climbing from #4 to #1 alongside 38.3% YoY sales growth. Relative to Shred steady at #2 with 18.5% YoY growth and Big Bag O' Buds holding #3 with 16.2% YoY growth, maintaining #5 while reaching a peak rank in June 2026 implies share is consolidating just outside the top four and that breaking into #4 requires displacing a declining incumbent rather than chasing the top three.

Notable Products

Little Red Indica Pre-Roll 4-Pack (2g) posted the clearest movement in June 2026 with a +27.3% month-over-month lift at rank 2, contrasting with Big Red - Hybrid Pre-Roll 20-Pack (10g) slipping -8.3% while holding rank 1. Four of the top ten are Flower SKUs clustered between ranks 3 and 10, where Strawberry Amnesia (28g) in rank 3 inched +2.1% as Kush Breath (28g) fell -7.4% at rank 5, signaling that incremental Flower growth is reliant on a few anchor strains while value-pack Pre-Rolls drive volume concentration. The mix implies The Original Fraser Valley Weed Co. is leaning into multi-pack Pre-Rolls for traffic while maintaining selective strain-led Flower positions to stabilize share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.