Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

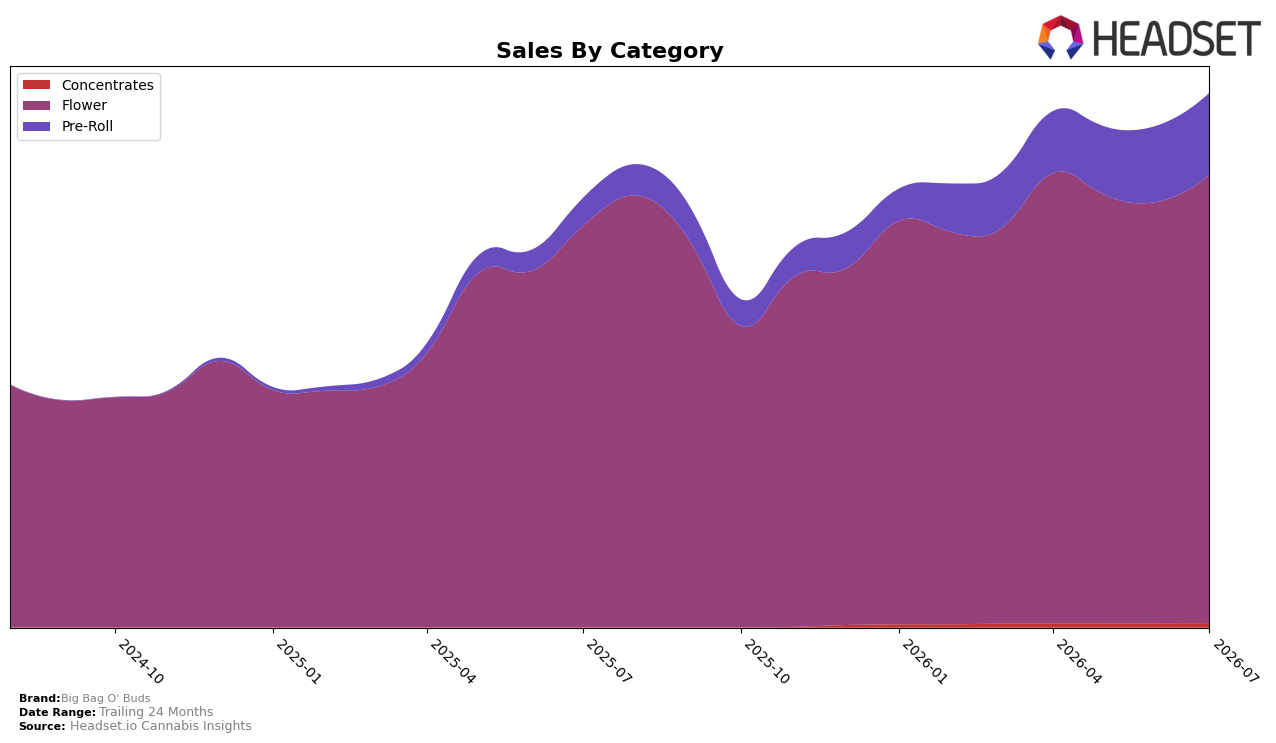

In July 2026, Big Bag O' Buds concentrated 83.92% of sales in Flower, where category sales grew 11.63% year over year and 6.31% month over month, while Pre-Roll accounted for 15.31% with a 196.48% year-over-year surge and 7.42% month-over-month growth. Concentrates remained 0.77% of mix with a 4.06% month-over-month uptick and no reported year-over-year figure, and the brand’s overall average price fell 32.15% year over year to $50.87 even as total brand sales rose 24.47% year over year. The pattern implies the brand is leaning into unit velocity via lower prices and expanding Pre-Roll presence without diluting its Flower anchor, setting conditions for sustained volume-led growth while keeping category breadth controlled.

With Flower at an 83.92% share and ranked 1 in Flower in British Columbia, the 6.31% month-over-month and 11.63% year-over-year gains indicate defensible leadership, while the 196.48% Pre-Roll year-over-year lift alongside a 7.42% month-over-month increase signals targeted penetration into a lower-price, trial-friendly format. Paired with a 32.15% price decline against a 24.47% year-over-year sales increase and a 223.94% two-year expansion, this mix shift implies Big Bag O' Buds is trading some average selling price for share capture and frequency, positioning the brand to convert Pre-Roll trial into Flower loyalty while using Concentrates (0.77% share, 4.06% month-over-month) as a niche halo rather than a scale driver.

Competitive Landscape

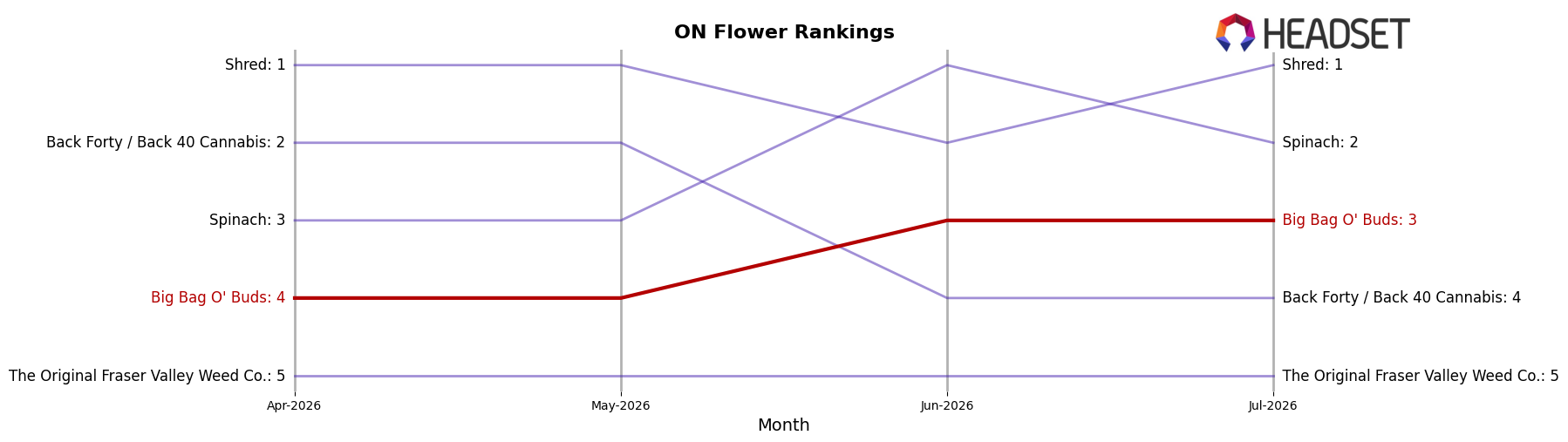

Big Bag O' Buds sits at rank #3 in ON Flower in July 2026, unchanged YoY from #3, after edging up one spot from #4 three months prior; the brand previously peaked at #1 in August 2025, indicating a two-position slide from that high. Shred moved from #2 YoY to #1 with a 17.2% sales increase, while Spinach climbed from #4 to #2 on 31.1% YoY growth, placing both ahead of Big Bag O' Buds, whereas Back Forty / Back 40 Cannabis fell from #1 YoY to #4 with a 5.4% sales decline. The combination of stable YoY rank at #3 and a recent quarter-on-quarter rise from #4 to #3 suggests Big Bag O' Buds is holding share against upward pressure from faster-growing leaders, implying the brand must convert stability into gains to re-approach its August 2025 #1 peak.

Notable Products

Blueberry Dream (28g) sets the tone in July 2026 with a -9.8% month-over-month slide while holding rank 7, as Purple Cherry Punch (28g) climbs 17.1% to rank 2 and Purple Cherry Punch (3.5g) edges up 2.3% at rank 1. With five of the top ten in Flower and four in Pre-Roll, the mix concentrates around two categories, and the Purple Cherry Punch Pre-Roll 10-Pack (5g) jumps 31.8% at rank 3 versus Blueberry Dream Pre-Roll 10-Pack (5g) dipping -8.2% at rank 4, pointing to consumer pivot within formats rather than across them. The coexistence of modest gains at the very top of Flower and double-digit growth in the lead Pre-Roll signals Big Bag O' Buds is tilting its commercial energy toward scalable pack formats that reinforce flagship strains while allowing underperforming large-format Flower to be managed without broad discounting, despite Blueberry Dream (28g) still contributing $610,619.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.