Where to Buy

Cosmec Healing is stocked at 63 licensed dispensaries across Maryland, with the deepest coverage in Baltimore, Silver Spring, Annapolis, Rockville, and Bethesda. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

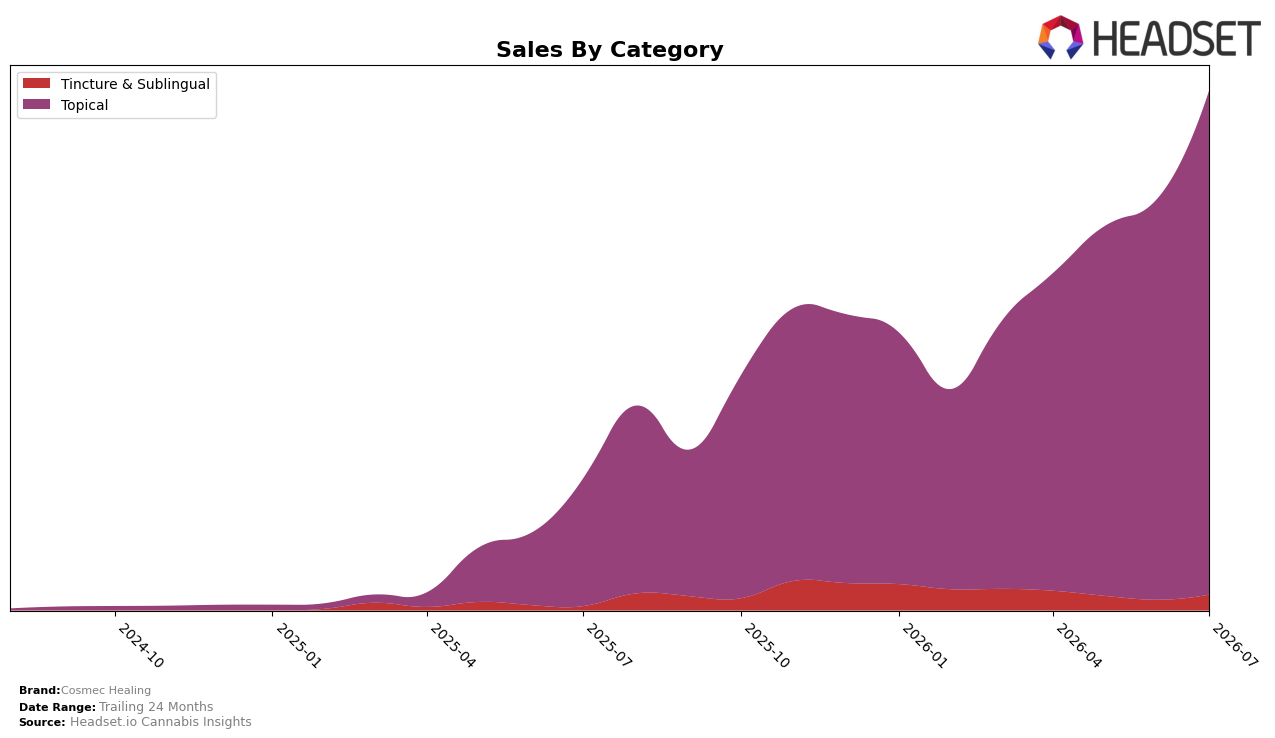

Cosmec Healing is concentrated in Topical at 97.01% share with a 25.56% month-over-month lift in July 2026, while Tincture & Sublingual holds 2.99% share with a faster 49.61% MoM rise; the overall brand averaged $43.18 per unit with a 12.34% year-over-year price decline. Year over year, Topical expanded 296.32% and Tincture & Sublingual rose 290.15%, positioning July 2026 as a mix where the core keeps pace with the niche even as price steps down; this implies volume-led growth is carrying the brand rather than pricing, and the tilt toward Topical is still the anchor.

With Topical ranked 1 in Maryland and holding 97.01% of sales mix versus 2.99% for Tincture & Sublingual, the 25.56% MoM gain in the core alongside a 49.61% MoM surge in the secondary signals headroom to extend the brand’s positioning from a single-category leader to a two-category presence. The parallel YoY lifts of 296.32% in Topical and 290.15% in Tincture & Sublingual, coupled with a 12.34% YoY price decrease, imply the brand’s July 2026 posture is about widening patient reach and unit throughput, using Topical leadership to seed trial into Tincture & Sublingual without diluting the primary rank or mix.

Competitive Landscape

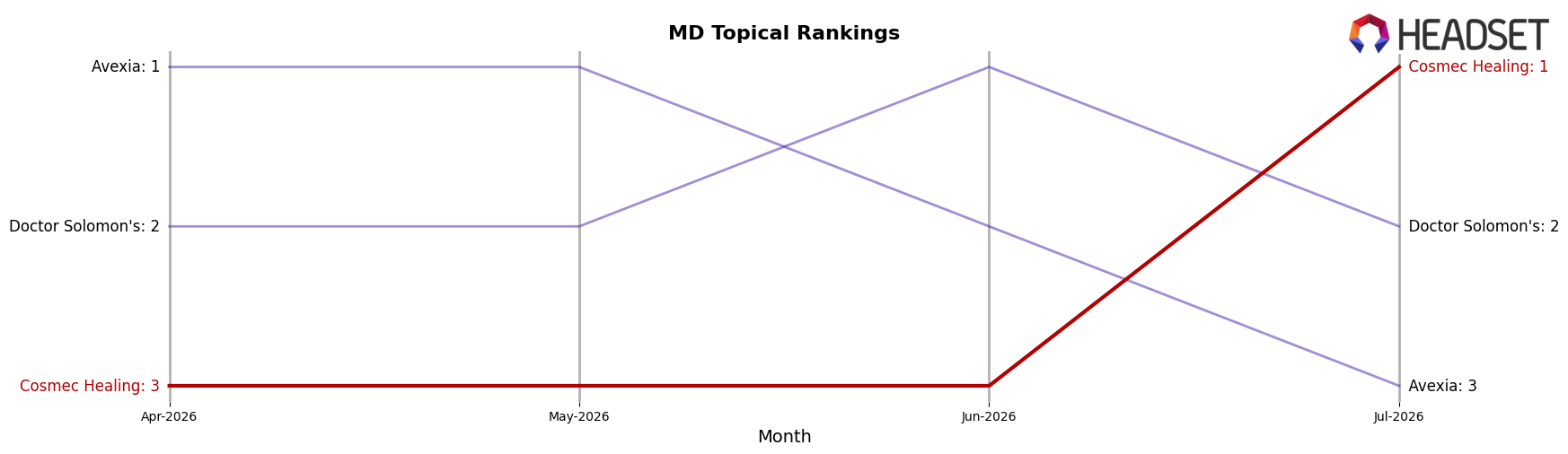

Cosmec Healing is currently ranked #1 in MD Topical, up three places year over year from #4 to #1, and two places since April 2026 when it sat at #3; July 2026 also marks its peak at #1. In contrast, Doctor Solomon's is at #2 with a year-over-year decline in sales of 29.9%, and Avexia sits at #3 with a 41.5% year-over-year sales contraction; meanwhile, Eastern Shore Extracts holds #5 despite a 35.4% year-over-year sales increase, indicating share gains are not mapping directly to rank for mid-pack players. This pattern implies Cosmec Healing’s upward rank trajectory—from #4 in July 2025 to #1 in July 2026—owes as much to competitor retrenchment as to its own positioning, suggesting retention at #1 will hinge on sustaining relative momentum against declining incumbents and selectively rising challengers.

Notable Products

CBN/CBD 2:1 Relax Tincture (600mg CBN, 1200mg CBD, 30ml) posted the largest movement in July 2026 with a 260.3% month-over-month surge to rank 3, while CBG/THCV/CBD Dayshift Tincture (600mg CBG, 300mg THCV, 1200mg CBD) collapsed 84.1% MoM to a shared rank 7, indicating volatile demand around functional tinctures. Topicals concentrated the leaderboard with three of the top five positions as CBD/CBN/THC 4:2:1 Recovery Salve (1000mg CBD, 500mg CBN, 250mg THC) rose 35.7% MoM to rank 1 and CBD/CBC/THC HeadZen Gold Salve (750mg CBD, 100mg CBC, 125mg THC) slipped 8.1% MoM to rank 2, pointing to a tilt toward recovery-oriented formats over niche daytime tinctures. The CBD/CBG 2:1 Activate Salve Balm (1000mg CBD, 500mg CBG) jumped 308.8% MoM to rank 5 despite low absolute dollars near $278, while the CBD/CBC 7:1 Headache Transdermal Salve Stick (750mg CBD, 100mg CBC) fell 22.4% MoM to rank 7, implying shopper preference is consolidating around broader relief SKUs rather than targeted micro-categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.