Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Rove is stocked at 2,266 licensed dispensaries across California, New York, and 14 other states, 489 of them in California, with the deepest coverage in Los Angeles, Sacramento, Santa Ana, Long Beach, and San Diego. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

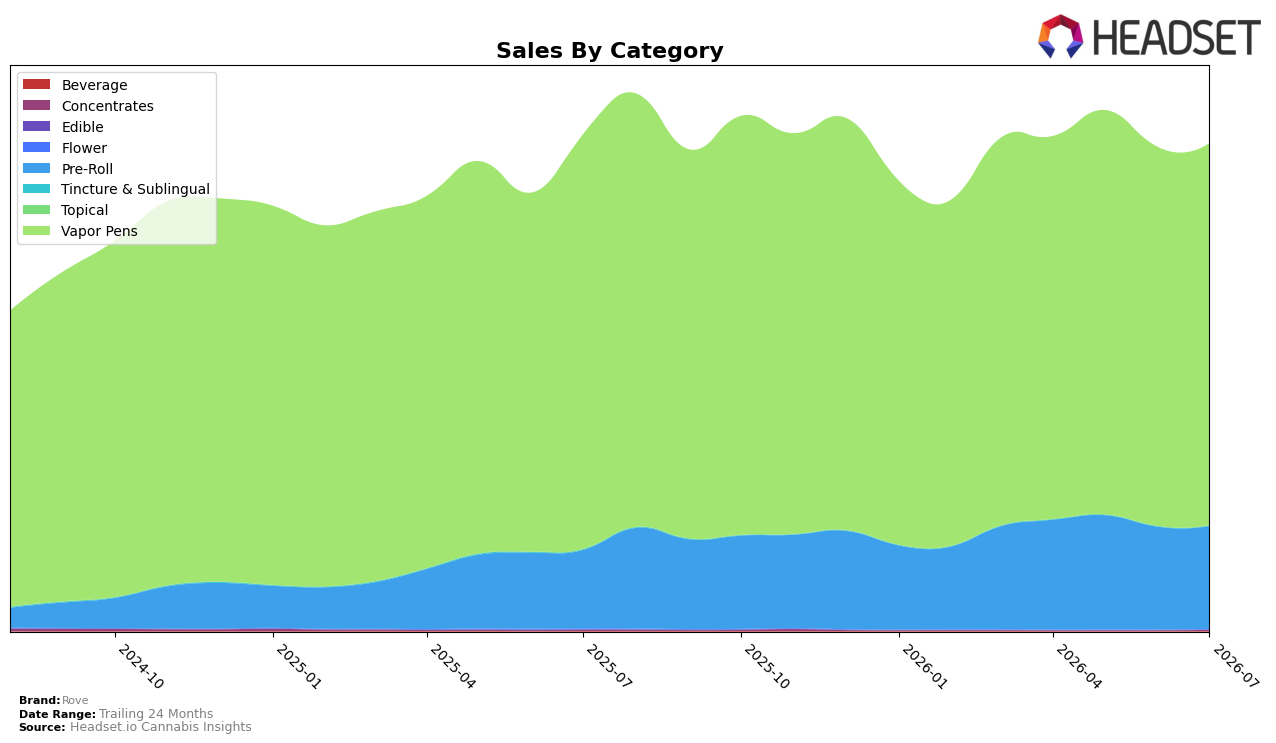

Rove’s mix in July 2026 remained concentrated in Vapor Pens at 78.65% share, yet that anchor declined year over year by 7.88% while inching up month over month by 0.82%; meanwhile, Pre-Roll expanded to 21.15% share with a 31.64% YoY increase and a 0.28% MoM lift. Smaller lines were volatile: Concentrates held 0.15% share with a 149.29% MoM spike despite a 12.18% YoY drop, Beverage sat at 0.04% share with 18.07% MoM growth alongside a 9.72% YoY decline, and Tincture & Sublingual fell 16.08% MoM and 88.98% YoY to 0.01% share as Flower contracted 26.33% MoM and 97.63% YoY to near-zero share. With average price down 6.43% YoY to $37.73 and total brand sales down 1.82% YoY despite a 35.31% 24‑month gain, the pattern implies the brand is using price to protect a Vapor Pens-led base while leaning on Pre-Roll growth to offset category softness.

The combination of a 7.88% YoY decline in Vapor Pens against a 31.64% YoY rise in Pre-Roll signals a portfolio reweighting toward formats that add incremental shoppers rather than pure trade-down within pens, and the 0.82% MoM pen lift versus the 0.28% MoM Pre-Roll gain indicates near-term stability anchored in the core. The 149.29% MoM jump in Concentrates from a 0.15% share base and the 18.07% MoM uptick in Beverage at 0.04% share suggest targeted experimentation rather than material diversification, while the 88.98% YoY collapse in Tincture & Sublingual and 97.63% YoY decline in Flower indicate deliberate pruning of low-velocity tails. Taken together with a number 1 rank in Vapor Pens in Nevada, the mix shift implies Rove is defending a leadership position in its primary category while allocating incremental effort to Pre-Roll to reduce reliance on a single format without diffusing focus.

Competitive Landscape

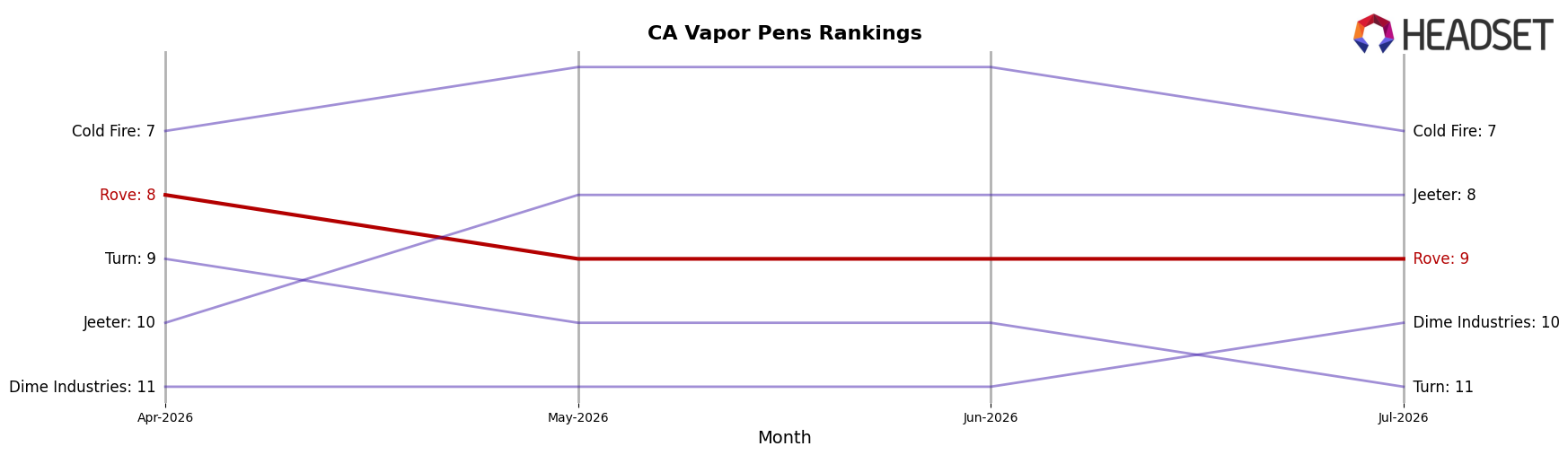

Rove ranks #9 in CA Vapor Pens in July 2026, improving 1 position from #10 year over year, but slipping 1 rank from #8 in April 2026 when it hit its peak; in contrast, Jetty Extracts climbed from #4 to #3 while posting a 41.7% YoY sales increase, and Plug Play fell from #3 to #4 alongside an 8.5% YoY sales decline. Against the category’s anchor, STIIIZY held #1 with a 6.8% YoY sales contraction while Raw Garden stayed #2 with a 4.6% YoY gain, indicating that Rove’s modest rise in annual rank but quarter-to-quarter dip positions it in a crowded middle tier where minor share shifts can swap ranks quickly.

Notable Products

Blue Dream Live Resin Liquid Diamond Disposable (1g) set the tone with a -9.9% month-over-month slide while holding rank 1 in July 2026, and Fruit Punch Gull Spectrum Melted Diamond Reload Pod (1g) at rank 10 fell -7.7%, indicating pressure at both the top and tail of the leaderboard. Seven of the top ten are Vapor Pens, with Pineapple Express Live Resin Melted Diamonds Reload Pod (1g) up 8.2% at rank 2 versus Maui Waui Live Resin Liquid Diamond Reload Pod (1g) up 4.7% at rank 8, pointing to gains concentrated in reload formats while disposables soften. This mix suggests Rove is tilting toward reloadable pods where smaller MoM gains are paired with sustained top-5 ranks, signaling a shift to formats that deepen repeat usage rather than one-time disposable purchases.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.