Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Drink Loud is stocked at 113 licensed dispensaries across Nevada, Massachusetts, and Illinois, 45 of them in Nevada, with the deepest coverage in Las Vegas, Henderson, North Las Vegas, Reno, and Carson City. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

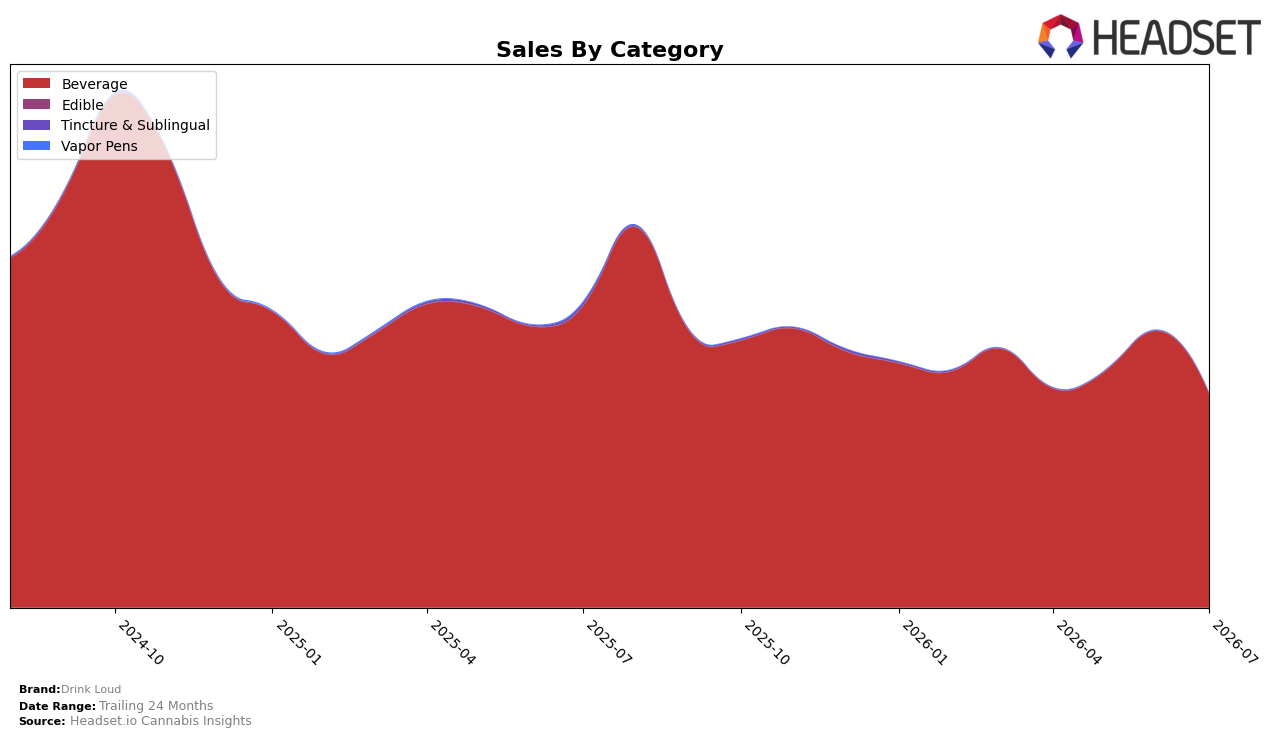

Beverage concentrated to 99.88% of Drink Loud’s mix in July 2026 while holding rank 4 in Nevada Beverage, with year-over-year sales down 29.14% and month-over-month down 22.72%, and average price sliding 16.43% YoY to $9.16 alongside a category-level average of $9.16 that mirrored discounting pressure; by contrast, Tincture & Sublingual sat at 0.12% share with a 593.87% MoM rebound but a 89.93% YoY decline and an average price of $7.77, indicating a tiny base reacting to promotional swings. The juxtaposition of a 29.84% YoY brand sales contraction against a 22.72% MoM dip within a 99.88% Beverage footprint implies overexposure to a single category where pricing compression and seasonal drag are amplifying volatility.

The shift toward an even tighter Beverage concentration at 99.88% share and a 22.72% MoM decline, paired with a 16.43% YoY average price reduction, signals that Drink Loud is leaning on price to defend velocity in Nevada while rank 4 in Beverage suggests volume density but limited cushion for mix-driven offsets; meanwhile, the 0.12% Tincture & Sublingual share with 593.87% MoM growth yet 89.93% YoY erosion points to opportunistic but unsustained trials that are too small to diversify risk. These dynamics imply Drink Loud’s positioning is anchored to value-oriented Beverage in Nevada, where deeper discounting and a thinner secondary category leave the brand sensitive to category headwinds and seasonal troughs.

Competitive Landscape

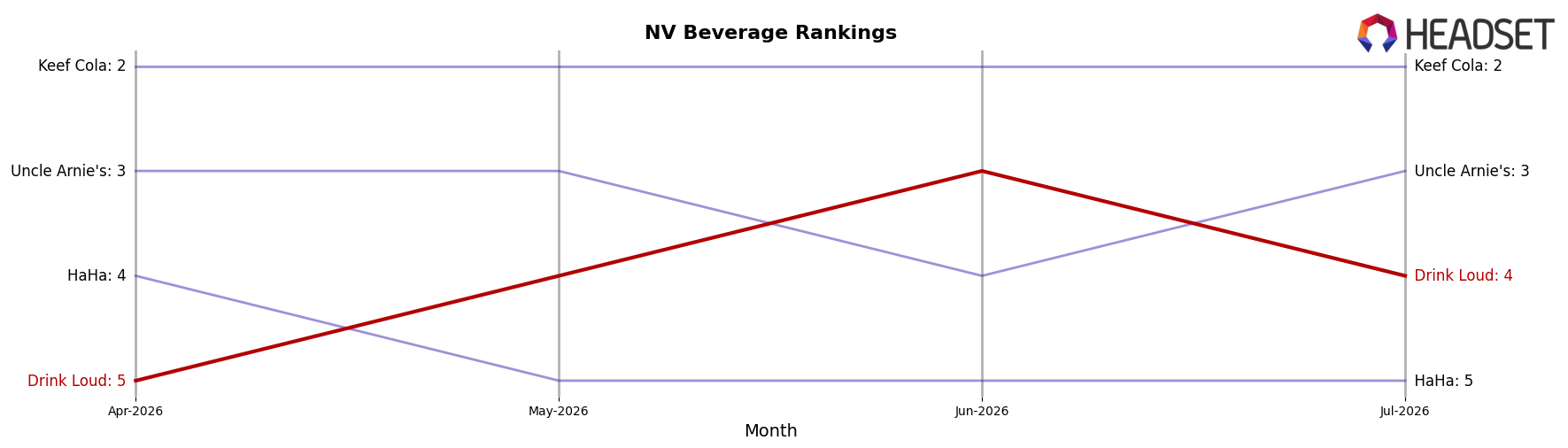

Drink Loud sits at rank #4 in NV Beverage in July 2026, up 1 position from #5 year over year, and has also improved 1 spot versus April 2026 when it was #5; however, it is 1 rank below its peak of #3 reached in June 2026 and trails the category lead by 3 positions. In contrast, Uncle Arnie's climbed from #4 to #3 year over year while expanding sales by 24.7%, and HaHa slid from #3 to #5 with a 40.3% sales decline, indicating Drink Loud’s upward rank movement is occurring amid competitor divergence rather than across-the-board market expansion. The pattern implies Drink Loud’s incremental rank gains are coming from positioning relative to weakening peers rather than overtaking the category’s front-runners, which sets a trajectory of gradual ascent contingent on defending against mid-tier volatility.

Notable Products

Cucumber Haze Tincture (100mg) posted a 611.8% month-over-month jump to rank 7 in July 2026, while Pink Lemonade Live Rosin Potion Shot (100mg THC, 2oz) fell 37.4% to rank 4. At the top, Maui Blast Potion Shot (100mg THC, 50ml) remained rank 1 despite a 25.8% decline, and Chill - THC/CBN 10:1 Kush Berry Shot (100mg THC, 10mg CBN, 50ml) slid 29.3% to rank 3. With six of the top seven SKUs in Beverage and only one Tincture & Sublingual entry surging off a low base, the mix implies Drink Loud is anchored in shots but is testing adjacent formats that could diversify reliance on a few high-volume potions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.