Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

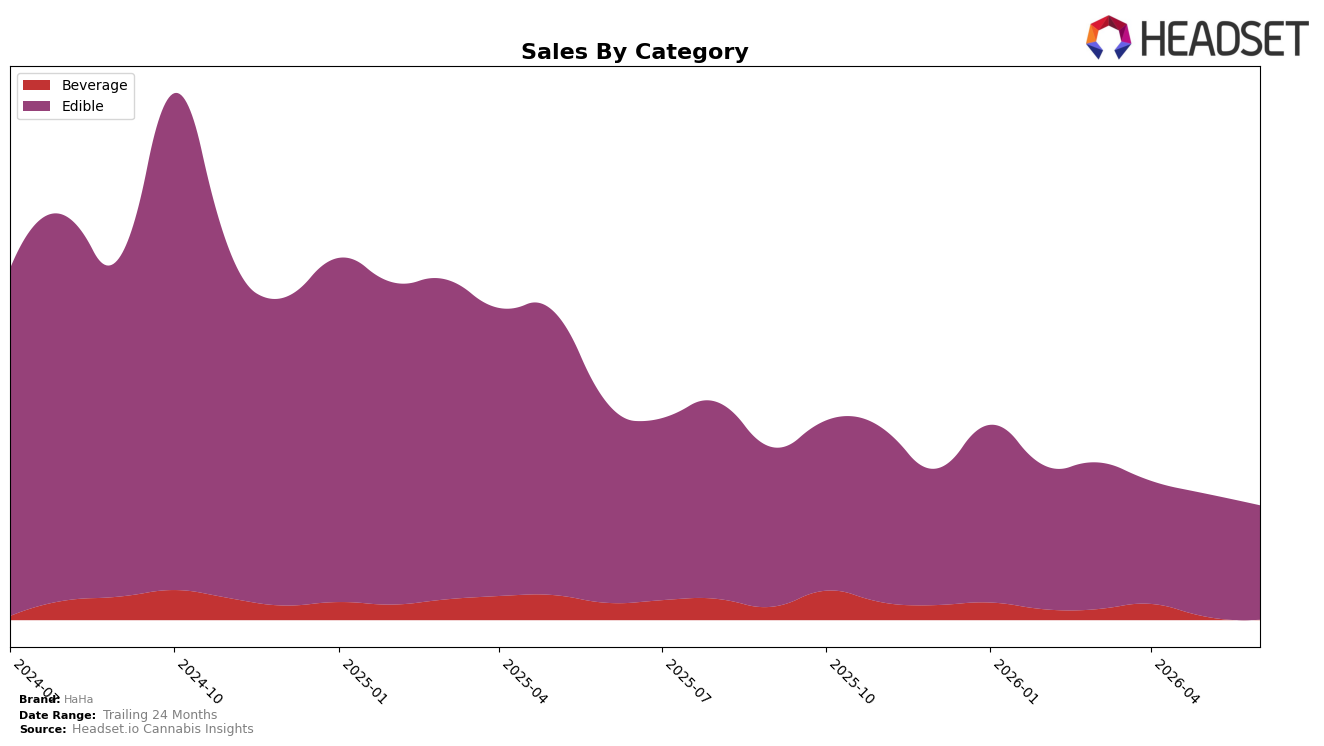

HaHa concentrated 85.30% of sales in Edible during June 2026, with Edible down 37.94% year over year and 5.86% month over month, while Beverage contributed 14.70% and declined 41.44% year over year and 12.09% month over month; the brand’s overall average price slipped 3.68% as Edible pricing sat at $20.04 versus Beverage at $10.16. In Nevada Edible, HaHa held rank 6 in June 2026, indicating category leadership depth despite a brand-level sales decline of 38.48% year over year and a 60.54% drop versus 24 months, implying the mix is anchored to Edible scale while Beverage contraction limits diversification.

The widening performance gap between Edible (down 5.86% month over month) and Beverage (down 12.09% month over month), paired with Edible’s 85.30% share and rank 6 positioning in Nevada Edible, implies HaHa competes on depth within a single category rather than breadth across formats. With Beverage’s 41.44% year-over-year decline outpacing Edible’s 37.94% and pricing spread of roughly $9.88 between categories, the current structure points to a defensive posture around core Edible velocity while Beverage under-indexing drags aggregate growth, suggesting the near-term path to stability relies on sustaining Edible rank while selectively rebuilding Beverage contribution.

Competitive Landscape

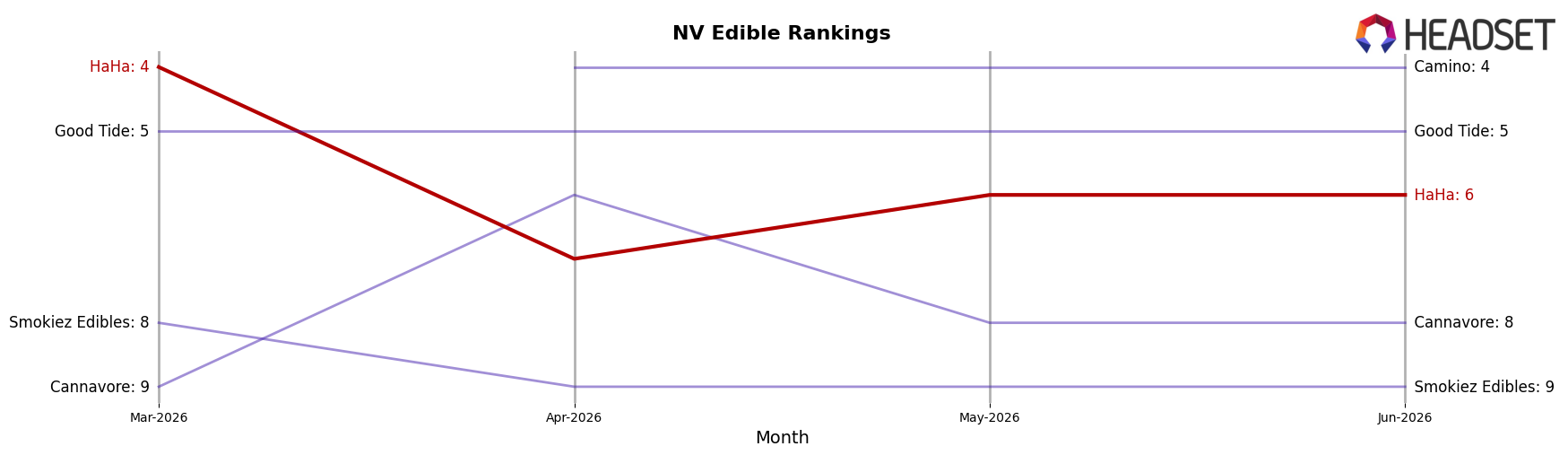

HaHa sits at rank #6 in NV Edible for June 2026, down 3 places year over year and off 2 spots from March 2026’s #4, despite having peaked at #2 in December 2024; meanwhile, Wyld held #1 while posting a -1.9% YoY sales change and Good Tide advanced to #5 with a 43.2% YoY sales increase. The middle-tier reshuffle is evident as Kanha / Sunderstorm moved to #3 on a 191.2% YoY sales jump while Incredibles stayed #2 with a -14.0% YoY decline, indicating that HaHa’s slippage from #4 to #6 over three months coincides with faster-moving rivals gaining share, implying that HaHa’s rank trajectory points to share pressure from momentum brands rather than top-heavy dominance.

Notable Products

Strawberry Lover Lemonade Gummies 10-Pack (250mg) posted the standout move with a 67.1% month-over-month gain to rank 3 in June 2026, while CBD/THC 2:1 Blue Raspberry Gummies 10-Pack (200mg CBD,100mg THC) slid 25.7% and Pineapple Paradise Gummies 10-Pack (100mg) fell 26.8%, indicating volatility within flavor extensions. CBG/THC 3:1 Mighty Mango Gummies 10-Pack (300mg CBG,100mg THC) held rank 1 despite a 1.3% dip, and Strawberry Lemonade Gummies 10-Pack (100mg) advanced 4.8% at rank 2, suggesting core SKUs are anchoring the lineup as beverages at ranks 6, 8, 9, and 10 logged declines between 8.8% and 23.4%. With four of the top ten in Beverage but all posting negative or unreported momentum and Edibles occupying ranks 1 through 7 with mixed results, the mix points to HaHa concentrating demand around higher-dosage and fruit-forward gummies rather than expanding beverage velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.