Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Fernway is stocked at 805 licensed dispensaries across New York, Massachusetts, and 3 other states, 256 of them in New York, with the deepest coverage in New York, Buffalo, Queens, Rochester, and Albany. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

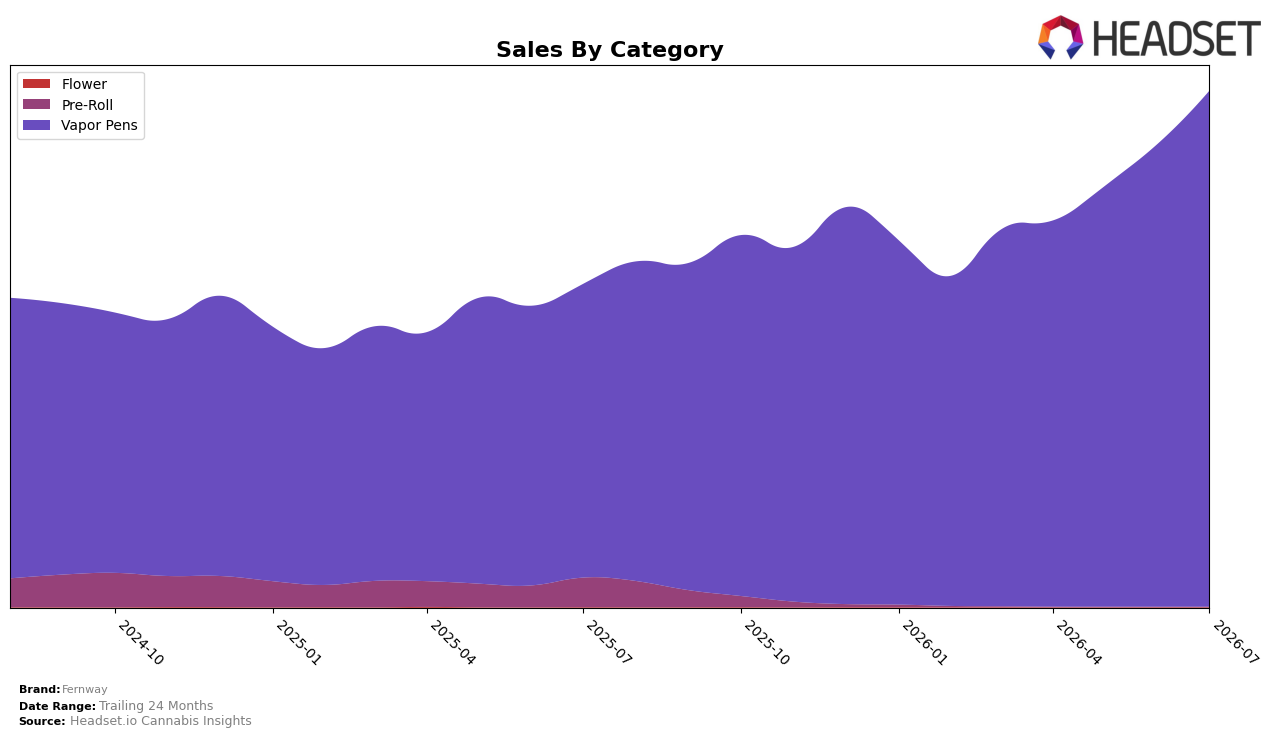

Fernway’s mix in July 2026 was effectively a single-category bet: Vapor Pens held 99.97% share with year-over-year growth of 75.82% and month-over-month growth of 11.42%, while Flower slid 46.35% YoY to 0.01% share despite a 6.97% MoM uptick, and Pre-Roll fell 99.77% YoY to 0.01% share even with a 29.62% MoM lift. Against this concentration, the brand’s overall sales grew 59.92% YoY and average price rose 30.22% YoY to $49.64, implying that July 2026 volume and pricing power were both anchored in Vapor Pens rather than diversified contribution.

This pattern positions Fernway as a Vapor Pens specialist in Massachusetts, where it ranked 1 in Vapor Pens, with the July 2026 price point in Vapor Pens at $49.68 and category share at 99.97% indicating limited cross-category insulation. The combination of a 11.42% MoM gain in Vapor Pens alongside double-digit YoY declines of 46.35% in Flower and 99.77% in Pre-Roll suggests risk concentration: performance is leveraged to maintaining Vapor Pens rank and price realization rather than expanding wallet share in adjacent formats.

Competitive Landscape

Fernway ranks #1 in MA Vapor Pens in July 2026, unchanged from #1 in July 2025, and it also held #1 three months ago, indicating zero rank drift over both 12-month and quarterly windows; in contrast, Dime Industries climbed from #6 to #4 year over year while posting 74.33% sales growth, and Perpetual Harvest stayed at #3 despite a 5.37% sales decline, while Select held #2 with 10.97% growth. This combination—Fernway’s static #1 position alongside upward pressure from faster-growing movers and mixed momentum among nearest followers—implies a durable lead today but a tightening competitive gap if acceleration persists.

Notable Products

Traveler - Key Lime Distillate Pro Disposable (2g) posted the biggest movement in July 2026 with a +45.2% month-over-month gain and rose within the top five at rank 4, while Traveler - Pineapple Funk Distillate Pro Disposable (2g) advanced +38.5% to hold rank 3. Traveler - Berry Haze Distillate Pro Disposable (2g) added +26.1% at rank 2, and Traveler - Alpine Strawberry Distillate Pro Disposable (2g) at rank 1 grew +9.5% to roughly $1.29M, whereas legacy 1g cartridges like White Widow Distillate Cartridge (1g) at rank 7 slipped -1.7%. With all top ten entries in Vapor Pens and a clear tilt toward 2g Traveler Pro Disposables occupying ranks 1–6 with gains from +9.5% to +45.2%, the mix points to Fernway prioritizing higher-capacity disposables over traditional 1g cartridges for near-term velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.