Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Savvy is stocked at 891 licensed dispensaries across Illinois, New Jersey, and 9 other states, 183 of them in Illinois, with the deepest coverage in Chicago, Springfield, Naperville, Normal, and Peoria. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

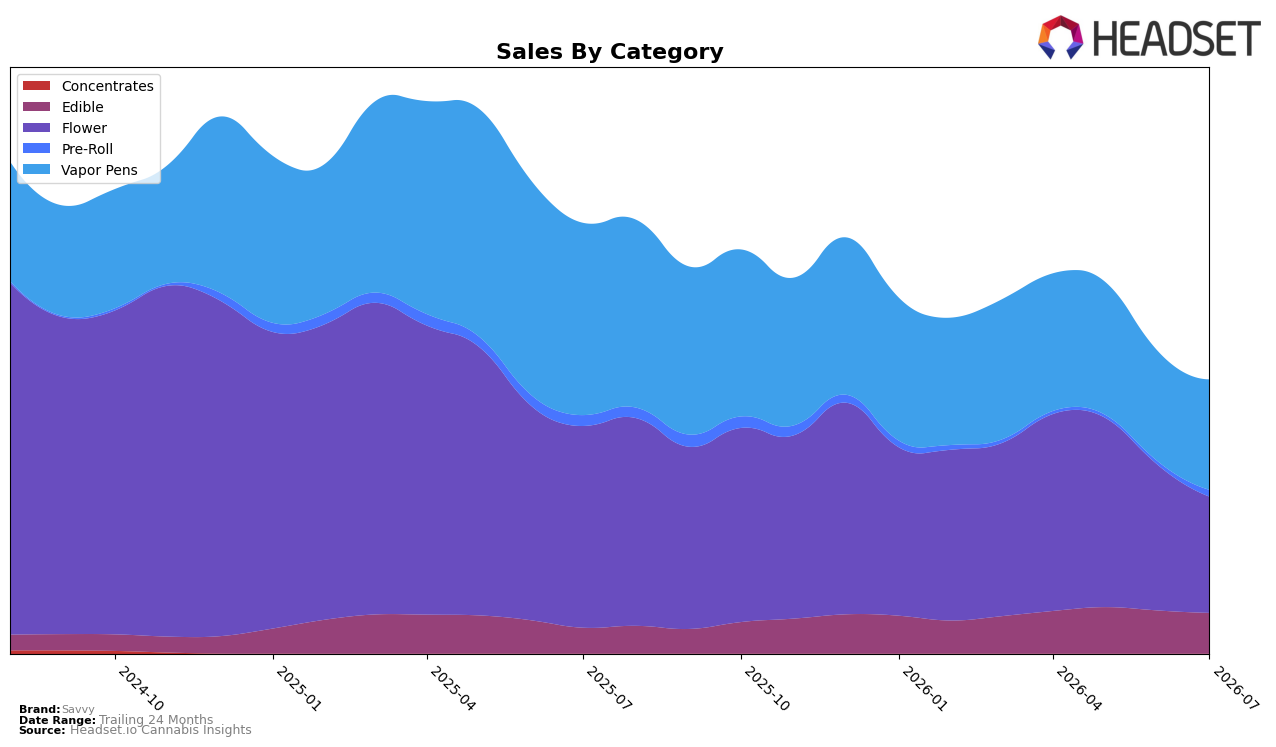

In July 2026, Savvy’s category mix tilted toward Flower at 42.45% share and Vapor Pens at 40.35% share, while Edible held 14.83% and Pre-Roll 2.37%. Flower contracted sharply with a year-over-year decline of 42.46% and a month-over-month drop of 20.09%, whereas Vapor Pens fell 42.61% year-over-year but edged up 0.20% month-over-month, indicating stabilization within a declining annual base. Edible grew 57.81% year-over-year but slipped 5.65% month-over-month, and Pre-Roll surged 97.22% month-over-month despite a 38.65% year-over-year decline, suggesting tactical gains from a low base. With Savvy ranked 6 in Vapor Pens in Illinois and brand-wide average price down 21.63% year-over-year to $26.73, the pattern implies a pivot toward price-accessible formats where monthly momentum can offset annual contraction.

The mix shift signals a repositioning away from reliance on Flower toward Vapor Pens and value-oriented formats, as Vapor Pens’ flat month-over-month change of 0.20% alongside a 42.61% year-over-year decline contrasts with Flower’s steeper 20.09% month-over-month drop and 42.46% year-over-year slide. Edible’s 57.81% year-over-year expansion paired with a 5.65% month-over-month pullback indicates demand elasticity responding to the 21.63% pricing reduction, while the 97.22% month-over-month lift in Pre-Roll against a 38.65% annual decline implies opportunistic fill-in rather than a core pillar. Together with the number 6 rank in Vapor Pens in Illinois, these moves imply Savvy is consolidating around mid-price inhalables and selective value entries where slight month-over-month gains can defend share even as total brand sales fell 36.44% year-over-year.

Competitive Landscape

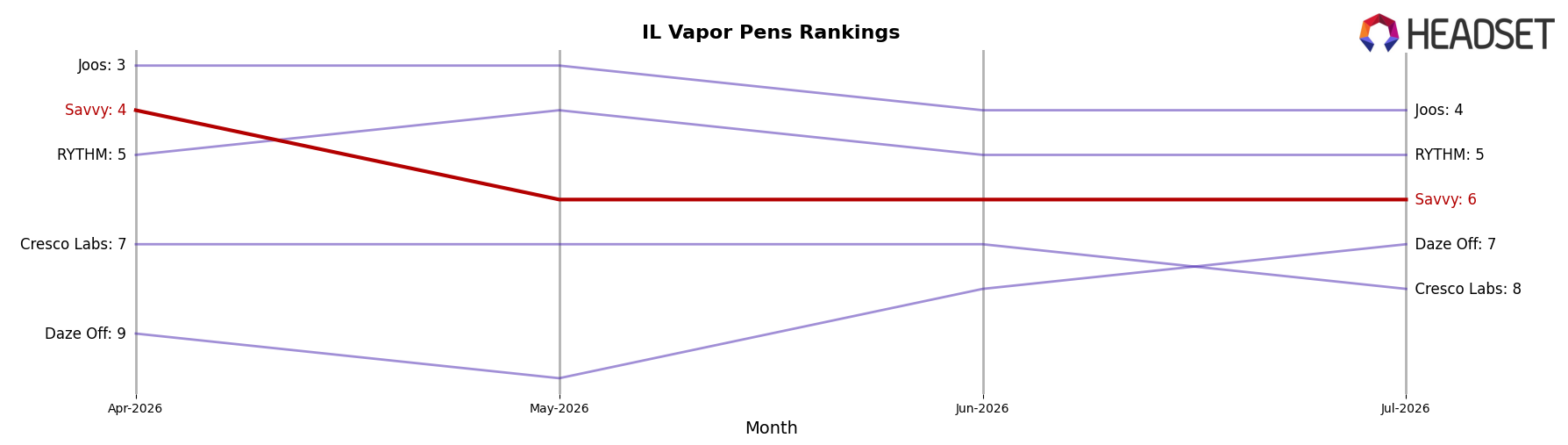

Savvy sits at rank #6 in Illinois Vapor Pens in July 2026, down 3 positions year over year from #3, and off 2 places from April 2026 when it was #4; this follows a prior peak of #3 in December 2025, indicating a 3-rank slide from that high. Meanwhile, &Shine held #1 with an 11.1% YoY sales lift while RYTHM edged into #5 with a 23.0% YoY increase, placing Savvy just behind a faster-climbing peer; additionally, Joos advanced to #4 alongside a 31.9% YoY gain, widening the gap versus Savvy’s two-position quarter-over-quarter decline from April 2026 to July 2026. The pattern implies Savvy’s trajectory is negative on rank momentum versus accelerating competitors, and absent a reversal, the brand risks ceding further share to adjacent positions.

Notable Products

Guap - CBD/THC 1:1 Peachy Punch RSO Gummy (100mg CBD, 100mg THC) posted the steepest decline at -13.6% and slipped to rank 4, while Guap - Berry Drip Macro Dose RSO Gummy (100mg) fell -11.6% yet held rank 2, indicating demand pressure at the top alongside rank resilience. In contrast, Guap - Blue Magic Macro Dose Gummy (100mg) jumped +28.8% to rank 3 as Guap - Blue Magic Macro Dose Gummy (25mg) dropped -16.0% at rank 7, signaling a trade-up within the same flavor line toward higher-dose formats. Eight of the top ten are Edible SKUs, and the leading Edible, Guap - Tangie Crush Macro Dose RSO Gummy (100mg), declined -5.7% at rank 1 while a new Vapor Pens entry, Extra Savvy - Rainbow Belts Distillate Cartridge (2g), debuted at rank 9 with $178,800, pointing to a category-heavy mix that is starting to diversify via vapes. The pattern implies Savvy is consolidating around macro-dose Edibles while selectively seeding Vapor Pens to hedge against softening growth in key gummy leaders.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.