Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Head & Heal is stocked at 220 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Rochester, Syracuse, and Brooklyn. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

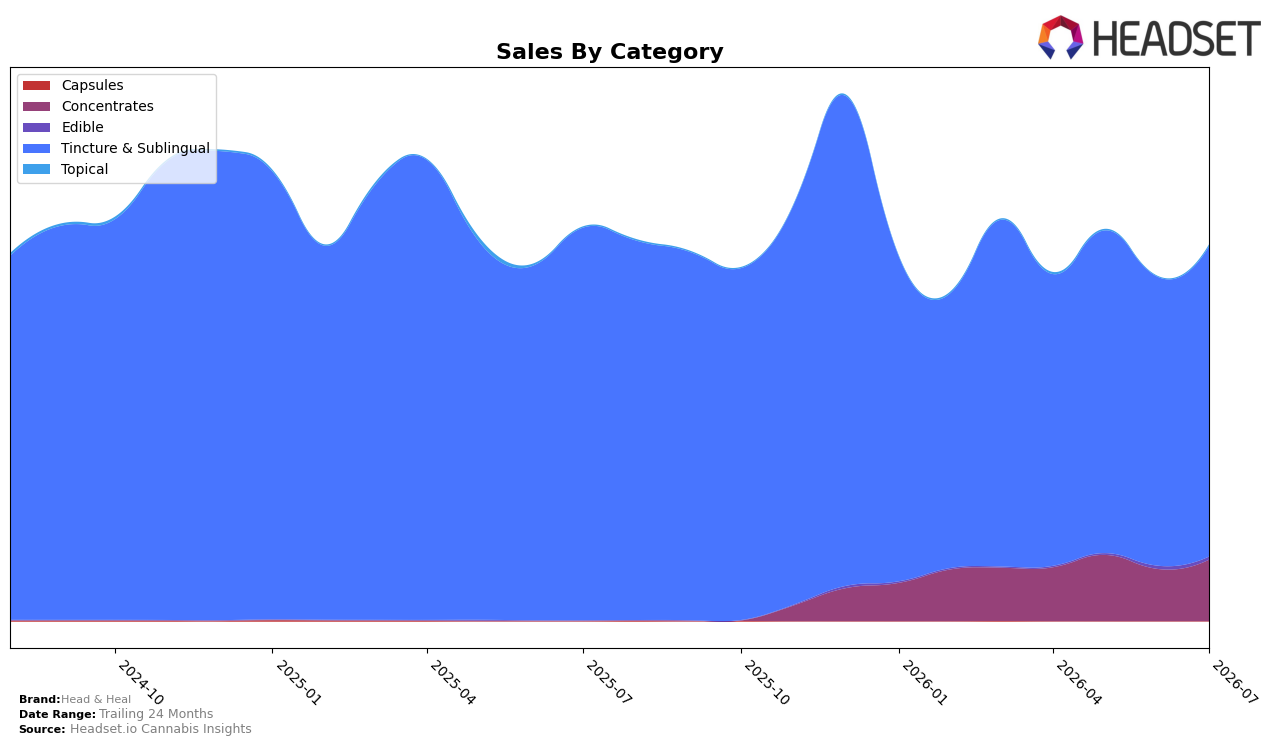

Head & Heal concentrated 82.59% of July 2026 sales in Tincture & Sublingual, where sales were down 21.00% year over year but up 7.42% month over month, while Concentrates rose to 16.28% share with a 17.88% month-over-month gain; Edible held just 0.72% share with a 2.98% month-over-month decline, and Topical, though only 0.41% share, surged 196.30% month over month and 78.33% year over year. Despite a brand-level sales decline of 4.55% year over year and an average price down 11.97% year over year to $76.11, the mix shift toward faster-growing Concentrates and a spiking Topical niche suggests near-term volume is being buttressed by non-core formats even as the core Tincture & Sublingual engine recalibrates.

With Tincture & Sublingual still the anchor at 82.59% share but carrying a 21.00% year-over-year drop against a 7.42% month-over-month rebound, and Concentrates adding 16.28% share on a 17.88% month-over-month rise, Head & Heal’s positioning tilts toward maintaining depth in its flagship while cultivating an option set that can buffer category-specific headwinds. The 196.30% month-over-month and 78.33% year-over-year growth in Topical, paired with a lower average price point in Concentrates at $62.54 versus $80.22 in Tincture & Sublingual, implies a price-sensitive pathway to defend rank 2 in New York Tincture & Sublingual while incrementally diversifying demand into adjacent use-cases.

Competitive Landscape

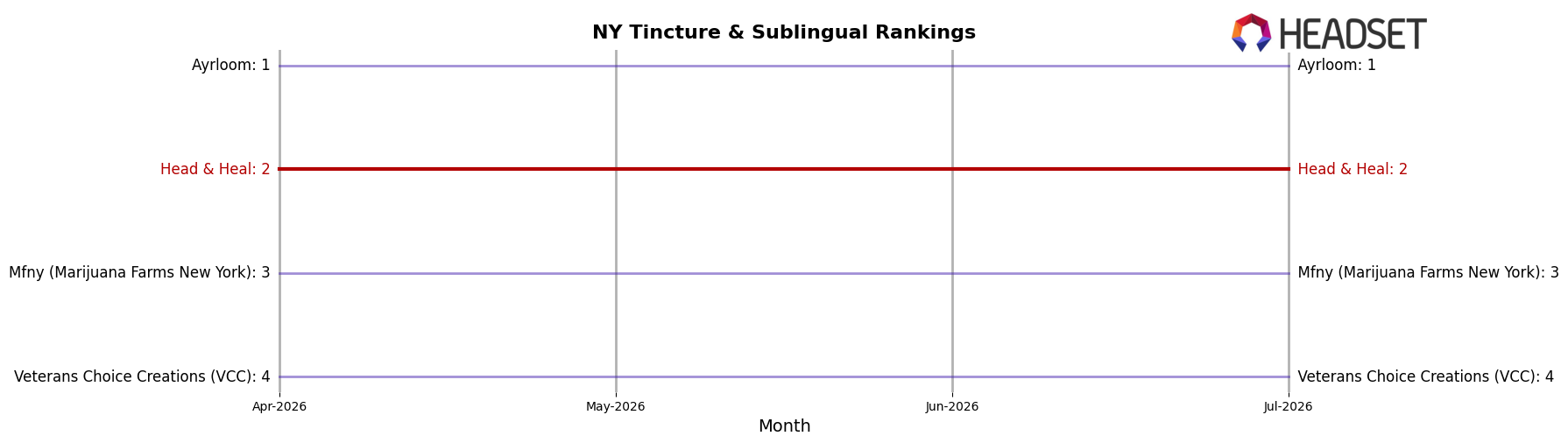

Head & Heal sits at rank #2 in New York Tincture & Sublingual for July 2026, unchanged from #2 year over year, and it has held #2 for three consecutive months while previously peaking at #1 in December 2024; meanwhile, Ayrloom holds #1 now and also held #1 a year ago as its sales slid 3.1% year over year, and Mfny (Marijuana Farms New York) remains at #3 with a steeper 11.6% year-over-year decline. In contrast, Veterans Choice Creations (VCC) stays at #4 while growing sales 10.8% year over year, and OMO - Open Minded Organics improved its rank from #6 to #5 despite a 23.9% sales contraction. The pattern—stable #2 positioning alongside a cooling #1 and a growing #4—implies Head & Heal’s path back to #1 depends less on broad category lift and more on converting Ayrloom’s 3.1% decline into share capture before VCC’s 10.8% growth narrows the gap.

Notable Products

CBD Medium Dog Oil Tincture (600mg CBD, 30ml) posted a -56.7% month-over-month drop and slid to rank 9 in July 2026, signaling a sharp pullback in pet-oriented demand while the broader lineup mostly held or grew. In contrast, CBG/THC 4:1 Focus Tincture (600mg CBG, 150mg THC, 30ml, 1oz) rose 23.9% MoM at rank 5 and CBD/THC/CBN 2:1:2 Sleep Tincture (600mg CBD, 300mg THC, 600mg CBN, 30ml) climbed 16.1% MoM at rank 2, indicating that function-led human formats are gaining traction against pet SKUs. Five of the top ten are Tincture & Sublingual products, with Max Strength THC Tincture (1000mg THC, 30ml, 1oz) steady at rank 1 on a 2.4% MoM lift and approximately $113,879 in sales, reinforcing a concentration in tinctures over edibles and topicals. This mix implies Head & Heal is consolidating around high-potency and targeted-effect tinctures while de-emphasizing peripheral categories like pet products.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.