Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Ayrloom is stocked at 434 licensed dispensaries across New York, Connecticut, and 2 other states, 428 of them in New York, with the deepest coverage in New York, Buffalo, Rochester, Queens, and Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

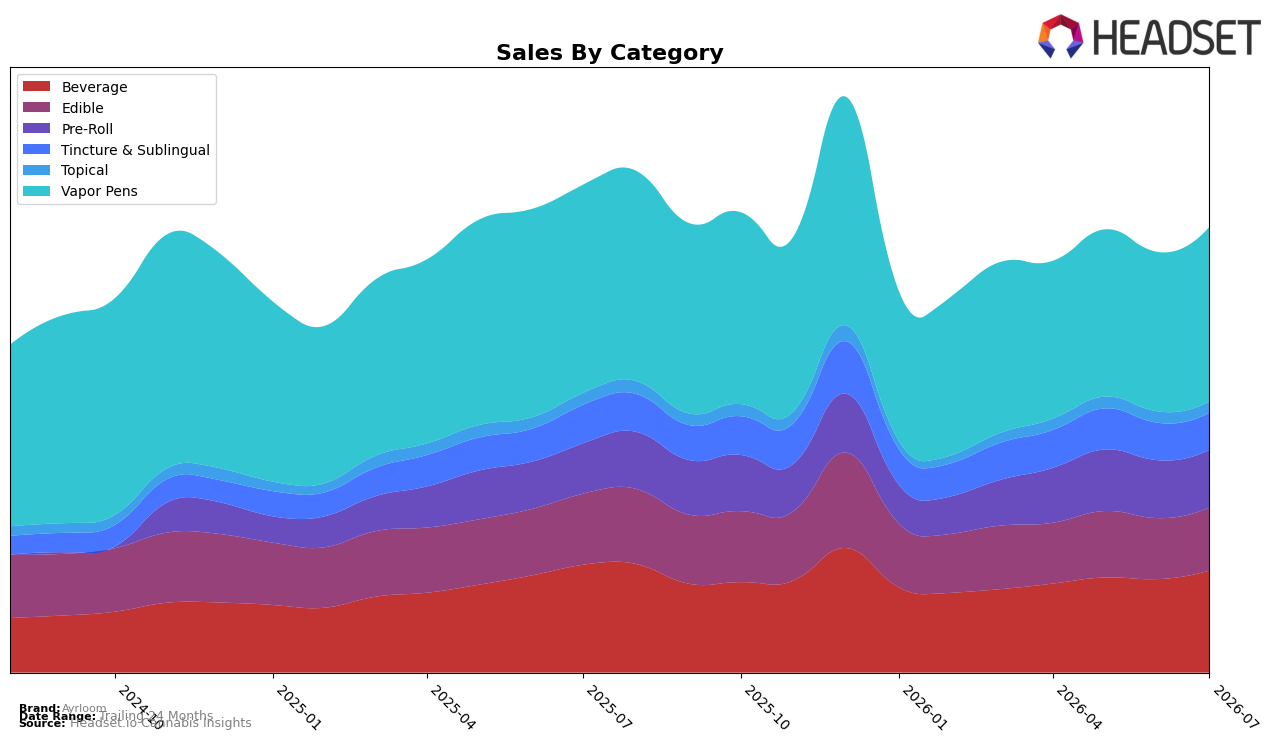

In July 2026, Ayrloom leaned on Vapor Pens at 38.81% share with a month-over-month gain of 9.50% but a year-over-year decline of 16.03%, while Beverage held 22.78% share with an 8.96% MoM lift and a 5.36% YoY drop. Edible contributed 14.20% share with MoM up 3.46% and YoY down 11.06%, contrasted by Pre-Roll at 12.98% share with YoY up 14.02% but MoM slipping 0.53%. Tincture & Sublingual sat at 8.48% share with MoM down 0.56% and YoY down 3.05%, and Topical at 2.75% share contracted 1.60% MoM and 5.85% YoY. Despite brand-wide sales down 8.51% YoY and average price down 10.46% YoY, category momentum is bifurcated: growth is concentrating MoM in Vapor Pens and Beverage even as YoY softness persists, implying near-term mix recovery is riding short-cycle demand rather than structural share gains.

The mix shifts imply Ayrloom’s positioning is tethered to a high-velocity headliner in Vapor Pens while margin support relies on Pre-Roll’s 14.02% YoY growth offsetting MoM drag of 0.53%, pointing to a price–volume recalibration rather than category expansion. With Beverage up 8.96% MoM yet still down 5.36% YoY, and Tincture & Sublingual slipping both 0.56% MoM and 3.05% YoY, the portfolio is tilting toward impulse and inhalables over wellness formats; maintaining a number 3 rank in Vapor Pens in New York while total sales are down 8.51% YoY suggests share defense is concentrated in a single category, which implies competitive resilience is product-line specific and dependent on sustaining double-digit MoM surges like 9.50% in Vapor Pens.

Competitive Landscape

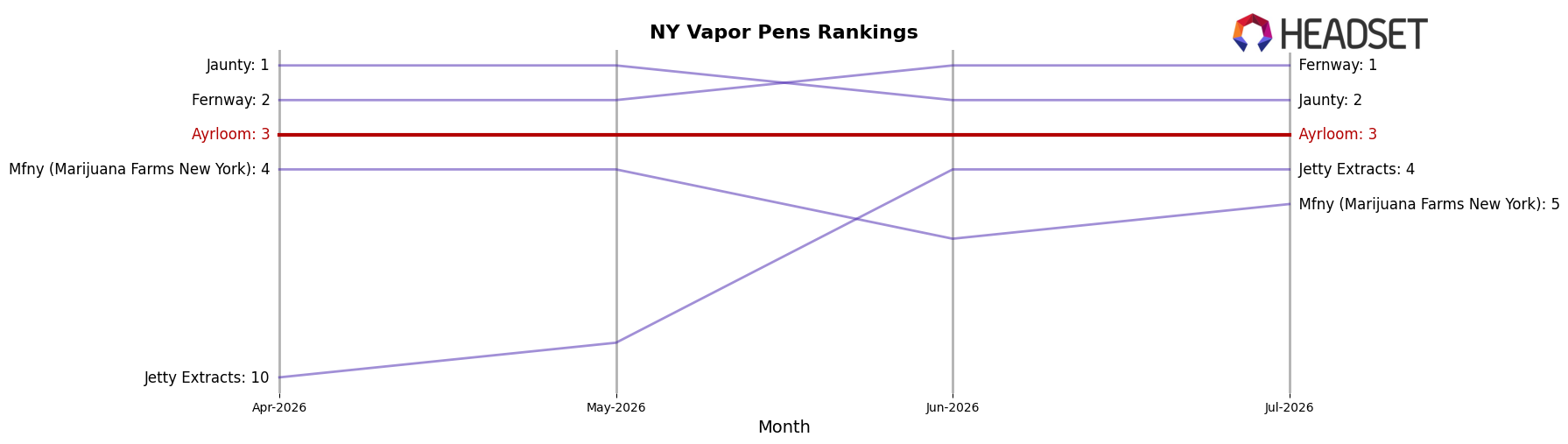

Ayrloom sits at rank #3 in NY Vapor Pens in July 2026, sliding 1 position year over year from #2 while holding flat versus April 2026 at #3, and that stability contrasts with Fernway advancing from #3 to #1 alongside a 46.8% YoY sales increase and Jaunty easing from #1 to #2 with a 24.8% YoY decline; further pressure is visible as Jetty Extracts rose from #22 to #4 on 199.3% YoY growth while Ayrloom’s peak at #1 in December 2024 has not been revisited, implying that without recapturing upward momentum in rank over the next quarter, Ayrloom risks being bracketed between a rising leader and a fast-climbing challenger.

Notable Products

CBD/THC 1:2 Black Cherry Sparkling Water (5mg CBD, 10mg THC, 12oz) posted the steepest move in July 2026 with a -23.2% month-over-month change while sliding to rank 7, contrasting with CBD/THC 1:2 Half & Half Lemonade Iced Tea UP (5mg CBD, 10mg THC, 12oz) rising 35.0% to hold rank 1. CBD/THC 1:2 Cran Apple Cider Up Drink (5mg CBD, 10mg THC, 12oz, 355ml) advanced 28.4% to rank 6, and nine of the top ten SKUs are Beverages, concentrating the mix around a single category. The lead SKU generated $200,025 alongside ranks 2 through 5 growing between 5.8% and 12.9%, while the only other decline among the top ten was a modest -1.4% at rank 10. Together these shifts indicate Ayrloom is consolidating around flavored beverage formats with selective pruning of underperforming sparkling water variants, tilting commercial focus toward higher-velocity citrus and cider profiles.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.