Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Veterans Choice Creations (VCC) is stocked at 119 licensed dispensaries across New York, with the deepest coverage in New York, Albany, Buffalo, Rochester, and Schenectady. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

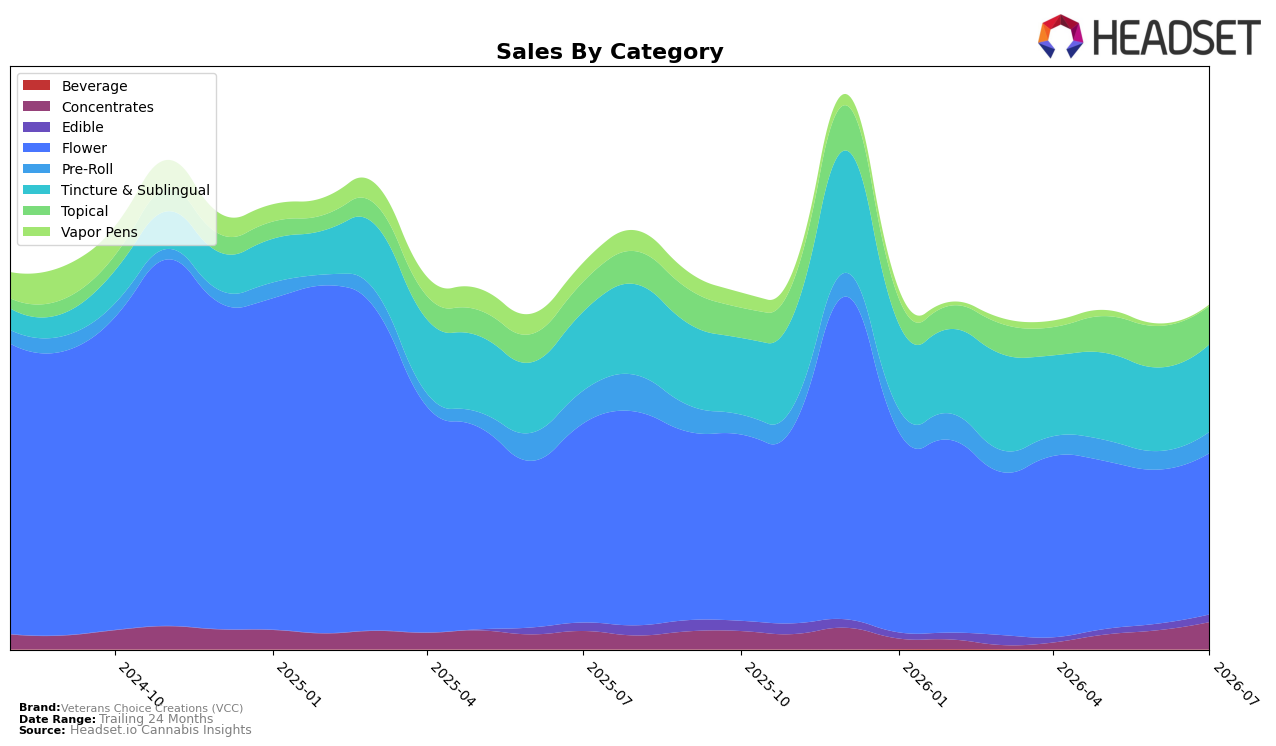

Veterans Choice Creations (VCC) concentrated 46.98% of July 2026 sales in Flower with average price at $70.23, yet Flower declined 18.99% year over year while rising 4.76% month over month; meanwhile Tincture & Sublingual held 25.43% share, growing 10.83% YoY and 4.60% MoM. Concentrates expanded to 7.87% share with 49.20% YoY and 42.84% MoM growth, while Pre-Roll at 6.13% share fell 35.24% YoY despite a 15.66% MoM lift. Topical reached 11.10% share with 28.48% YoY growth but slipped 7.58% MoM, and Vapor Pens collapsed to 0.35% share with a 93.55% YoY and 44.26% MoM decline. The mix indicates a pivot away from Vapor Pens and lagging Flower into higher-momentum niches like Concentrates and steady Tincture & Sublingual, which helps counteract a brand-level 10.85% YoY sales decline amid a slight 1.45% YoY uptick in average price to $51.92.

The shift toward Concentrates (+49.20% YoY, +42.84% MoM) and Tincture & Sublingual (+10.83% YoY, +4.60% MoM) alongside Flower’s drag (−18.99% YoY, +4.76% MoM) positions Veterans Choice Creations (VCC) to compete less on high-ticket Flower and more on efficacy-oriented formats, even as Topical’s 28.48% YoY growth is tempered by a 7.58% MoM pullback. With Pre-Roll down 35.24% YoY but stabilizing MoM (+15.66%), and Vapor Pens shrinking to just 0.35% share (−93.55% YoY), the pattern implies VCC’s near-term differentiation will come from deepening assortment and visibility in Concentrates and Tincture & Sublingual while treating Flower as a scale anchor rather than a growth engine, a stance consistent with a rank of 57 in New York Flower and the need to rebalance mix toward faster-growing, higher-velocity segments.

Competitive Landscape

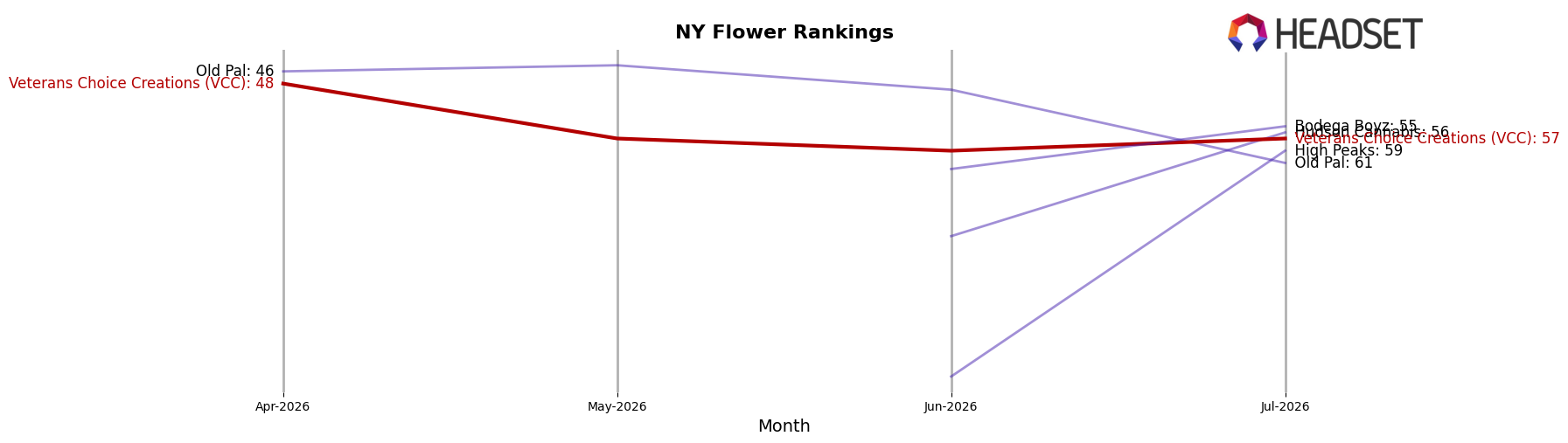

Veterans Choice Creations (VCC) sits at rank #57 in July 2026, down 11 positions YoY from #46 and 9 positions below its April–June three‑month marker at #48, while still far from its peak at #19 reached in November 2024; meanwhile, Find. advanced from #8 to #1 and Grassroots moved from #15 to #5 as their YoY sales shifted by +46.7% and +79.8% respectively, contrasting with Dank. By Definition holding near the top tier at #3 despite a -51.5% YoY sales change. With VCC slipping 9 ranks from its three‑month position and 11 YoY while top rivals climb 4–7 ranks into the top five, the pattern implies VCC is losing relative position in NY Flower and must counter faster-moving competitors to prevent further share erosion.

Notable Products

Spacebuds - Strawberry Slushie Moonrocks (4g) posted the steepest decline at -16.8% and slid to rank 3, while Spacebuds - Grape Bubbly Moonrocks (4g) rose 43.3% to hold rank 1, indicating a share shift within the same Moonrocks family. CBD/THC 1:1 Warrior Balm (900mg CBD, 900mg THC, 30ml) fell -10.7% at rank 4 as Hybrid FECO Syringe Applicator (1g) climbed 38.5% to rank 5, and two Pre-Roll 10-packs advanced with 10.6% and 37.6% MoM gains at ranks 6 and 9, respectively. Four of the top ten are Tincture & Sublingual SKUs clustered between ranks 2 and 8 with MoM changes from 3.1% to 9.3% and only one topical in the top ten showed negative momentum, implying VCC’s mix is tilting toward high-THC novelty Flower and accessible multi-pack formats while tinctures provide steady, moderate growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.