Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Hi5 Seltzer is stocked at 194 licensed dispensaries across Massachusetts, Maine, and 4 other states, 117 of them in Massachusetts, with the deepest coverage in Boston, Worcester, Brockton, Newton, and Pittsfield. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

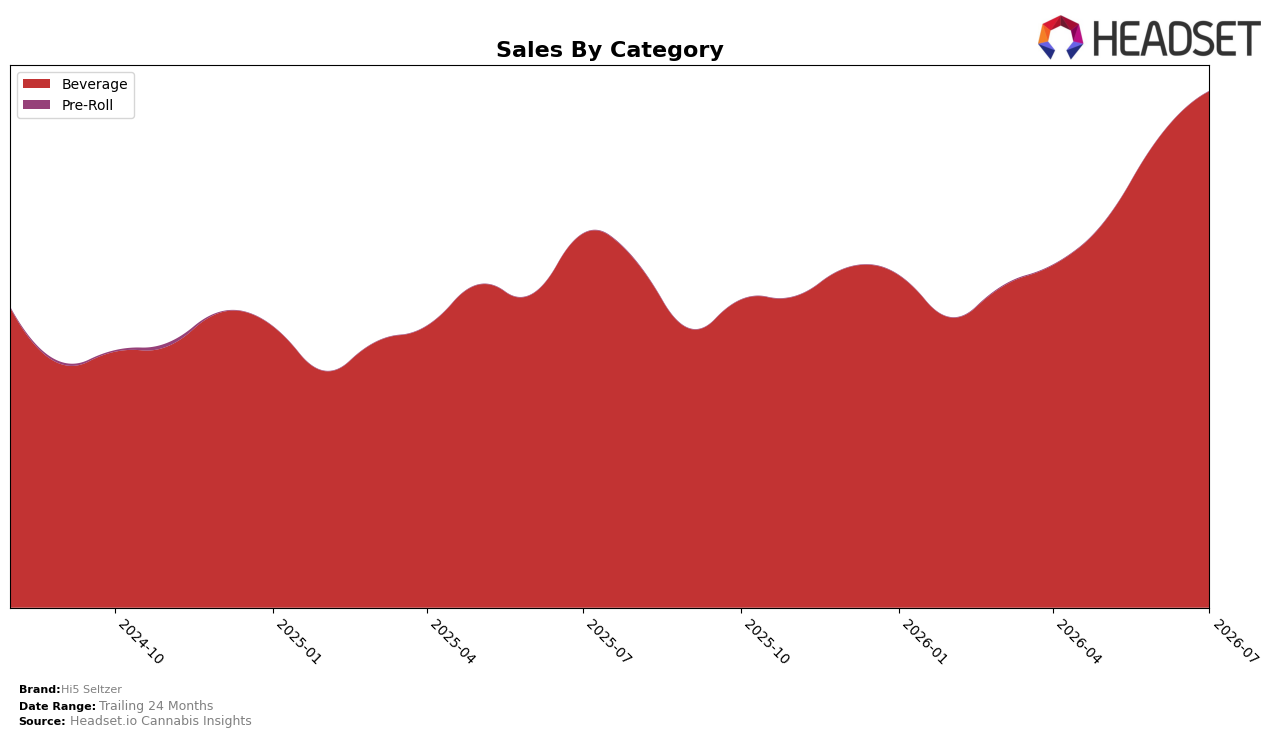

In July 2026, Hi5 Seltzer operated as a single-category brand with Beverage at 100.0% of sales share, posting year-over-year growth of 38.1% alongside month-over-month growth of 10.2%. Average price declined 3.3% year over year to $10.75, while the brand’s rank in Beverage in Massachusetts was 2, indicating share gains despite price compression. The pattern implies that Hi5 Seltzer is trading volume for broader reach within Beverage, using a modest price step-down to convert demand into higher rank and faster sequential velocity.

Given the 38.1% year-over-year rise paired with a 10.2% month-over-month lift, the volume curve is accelerating faster than price, positioning Hi5 Seltzer as a value-led option within the Beverage set rather than a premium-priced niche. Holding the number 2 rank in Massachusetts while maintaining a 100.0% Beverage focus suggests a concentrated, defensible lane where incremental distribution or pack-size optimization could compound gains even if pricing remains 3.3% lower year over year. The implication is that continued growth will hinge on sustaining the current elasticity advantage and defending rank through assortment depth, not category diversification.

Competitive Landscape

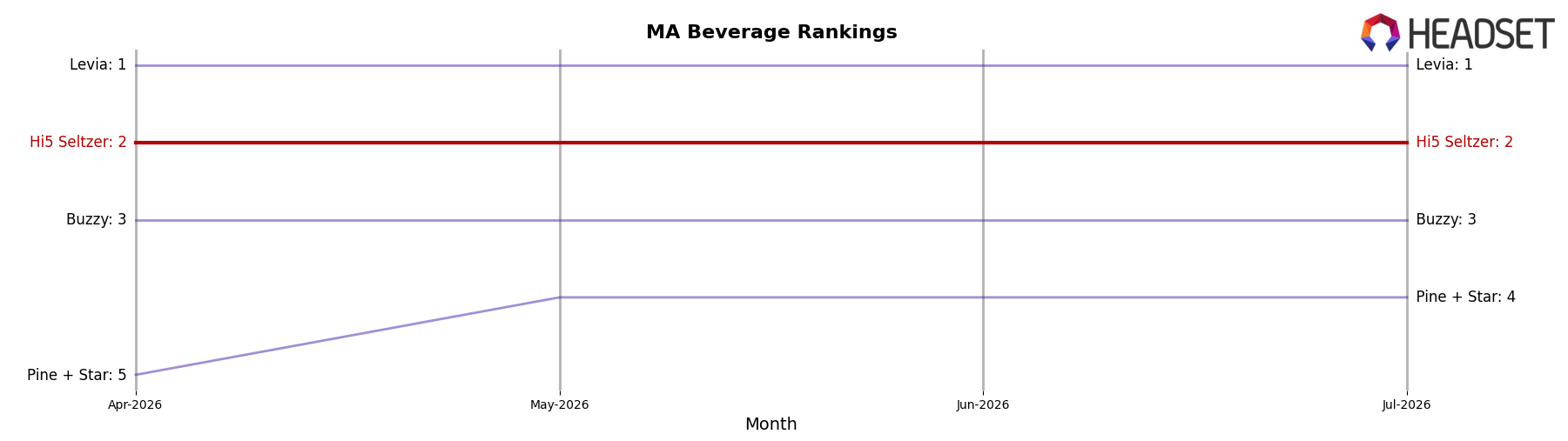

Hi5 Seltzer sits at rank #2 in MA Beverage in July 2026, unchanged year over year from #2, with a prior peak at #1 in March 2026 and no movement over the last 3 months from #2; meanwhile, Levia holds #1 both currently and year over year while posting a 37.2% YoY sales increase, and Buzzy remains at #3 with a 10.7% YoY lift. The competitive gap is further defined by Pine + Star improving from #5 to #4 on 26.6% YoY growth versus Hi5 Seltzer’s flat rank, and Squier's Elixirs advancing from #6 to #5 with 35.8% YoY growth, indicating upward pressure from below as Hi5 Seltzer holds a steady #2 without recent rank gains. The pattern implies that sustained #2 placement alongside March 2026’s brief #1 peak and faster-rising competitors points to a stalling trajectory that risks future share erosion unless momentum is re-accelerated.

Notable Products

Watermelon Infused Seltzer (5mg, 12oz, 355ml) posted the steepest decline in July 2026 at -34.3% MoM while holding rank 8, and Pomegranate Seltzer 4-Pack (20mg, 12oz, 355ml) fell -19.5% MoM at rank 10, signaling price/format sensitivity at the lower-dose and fringe 20mg SKUs. In contrast, Black Cherry Infused Seltzer 4-Pack (20mg THC, 12oz) gained 7.0% MoM to keep rank 1 while the Cranberry Lime Infused Seltzer 4-Pack (20mg THC, 355ml) surged 47.1% MoM into rank 3, and six of the top ten are 20mg 4-Packs, concentrating consumer demand in higher-dose multipacks. The top two items together exceeded $79,883 in July 2026 while ranks 4 and 5 rose 7.1% and 11.5% MoM respectively, implying that Hi5 Seltzer’s commercial direction is tilting toward reinforcing 20mg 4-Pack leadership while de-prioritizing single-can 5mg experiments that are losing velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.