Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Buzzy is stocked at 211 licensed dispensaries across Massachusetts and Maine, 147 of them in Massachusetts, with the deepest coverage in Boston, Worcester, Lowell, Springfield, and Northampton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

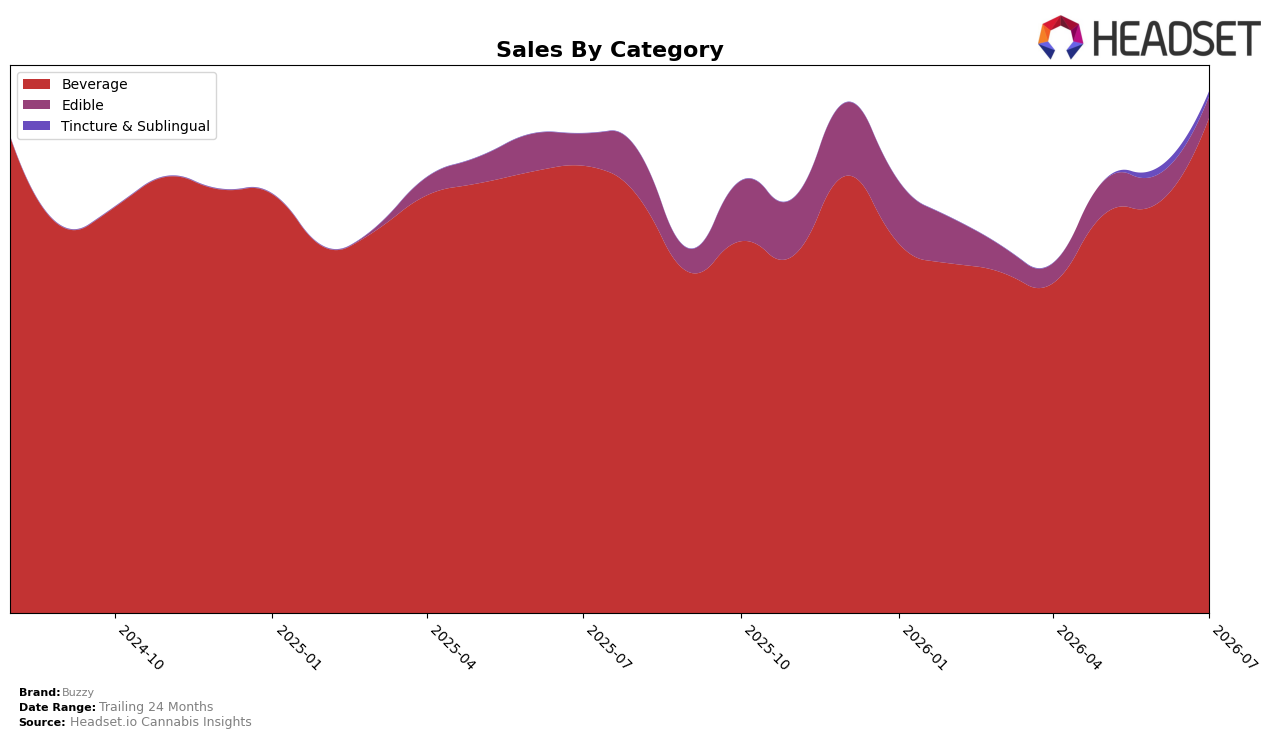

Buzzy concentrated 95.06% of July 2026 sales in Beverage, up 20.85% month over month and 10.69% year over year, while Edible fell to 4.02% share with a -25.81% MoM and -34.25% YoY decline; Tincture & Sublingual slipped to 0.92% share with a -25.36% MoM change and no year-ago baseline. Overall brand sales rose 8.71% YoY as the average price declined 6.90%, and Beverage pricing at $5.62 contrasted with Edible at $13.09. This mix shift implies Buzzy is consolidating around lower-priced Beverage volume to drive unit-led growth while exiting slower Edible demand.

With Beverage anchoring rank 3 in Massachusetts and expanding 20.85% MoM alongside a 10.69% YoY gain, Buzzy’s pricing at $5.62 positions it to win on velocity versus higher-ticket Edible at $13.09, even as the brand-wide average price dropped 6.90%. The -25.81% MoM in Edible and -25.36% MoM in Tincture & Sublingual compress assortment breadth while Beverage’s 95.06% share concentrates resources, indicating a strategy that prioritizes price-accessible Beverage scale to defend and potentially improve category rank.

Competitive Landscape

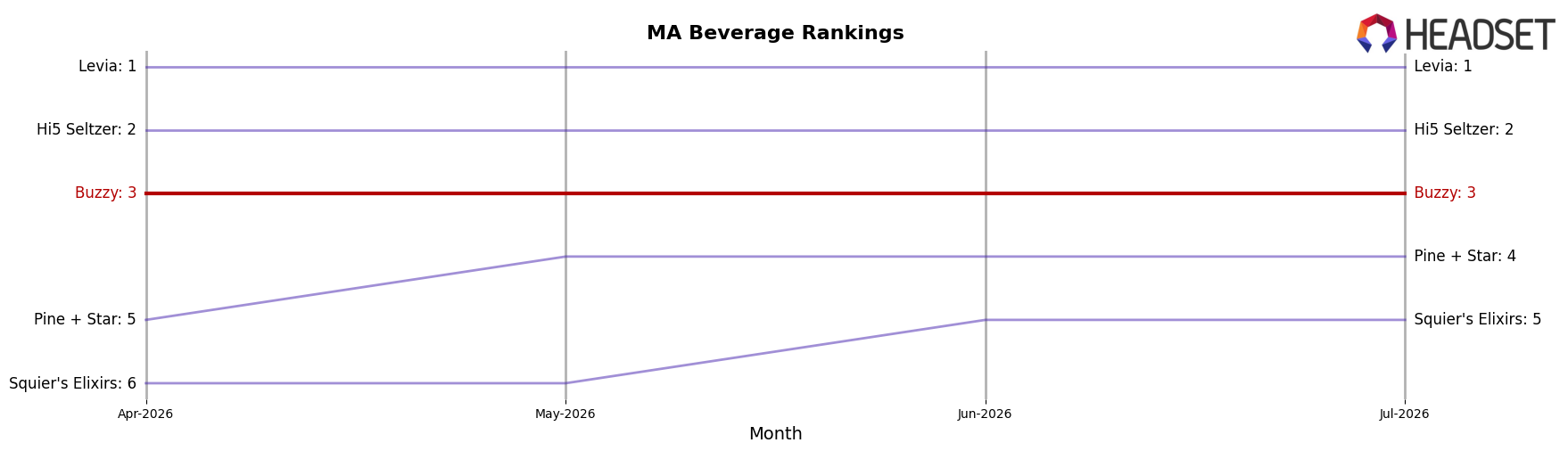

Buzzy sits at rank #3 in MA Beverage with a year-over-year rank change of 0 positions, holding #3 in April 2026 and remaining #3 in July 2026 while its peak rank of #3 also lands in July 2026; meanwhile, Levia stayed at #1 year over year with sales up 37.2% and Hi5 Seltzer held #2 with sales up 38.2%, whereas Pine + Star improved from #5 to #4 with a 26.6% sales lift. With no rank movement from April 2026 to July 2026 and peers gaining share above 26%, the pattern implies Buzzy’s trajectory is stable but risks entrenchment behind faster-climbing leaders unless a share-accretive move disrupts the #1–#2 lock.

Notable Products

Grape Soda (5mg THC, 355ml, 12oz) delivered the most interesting swing with a +38.7% month-over-month lift into rank 4, while Root Beer Soda (5mg THC, 355ml, 12oz) rose +47.6% to rank 1, indicating flavor-led momentum concentrated at the top. Orange Soda (5mg THC, 355ml, 12oz) held rank 2 on a +10.3% MoM gain as Blue Raspberry Soda (5mg THC, 355ml, 12oz) slipped -5.1% at rank 8, and eight of the top ten are Beverage SKUs, concentrating share in sodas rather than seltzers. With Root Beer Soda generating $33,555 alongside double-digit MoM gains for Grape and Ginger Ale (+29.9% at rank 3), the mix points to Buzzy deepening its soda-first strategy and prioritizing classic flavors over incremental seltzer extensions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.