Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

HiColor is stocked at 175 licensed dispensaries across New York, Maryland, and New Mexico, 101 of them in New York, with the deepest coverage in New York, Bronx, Buffalo, East Syracuse, and Bedford-Stuyvesant. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

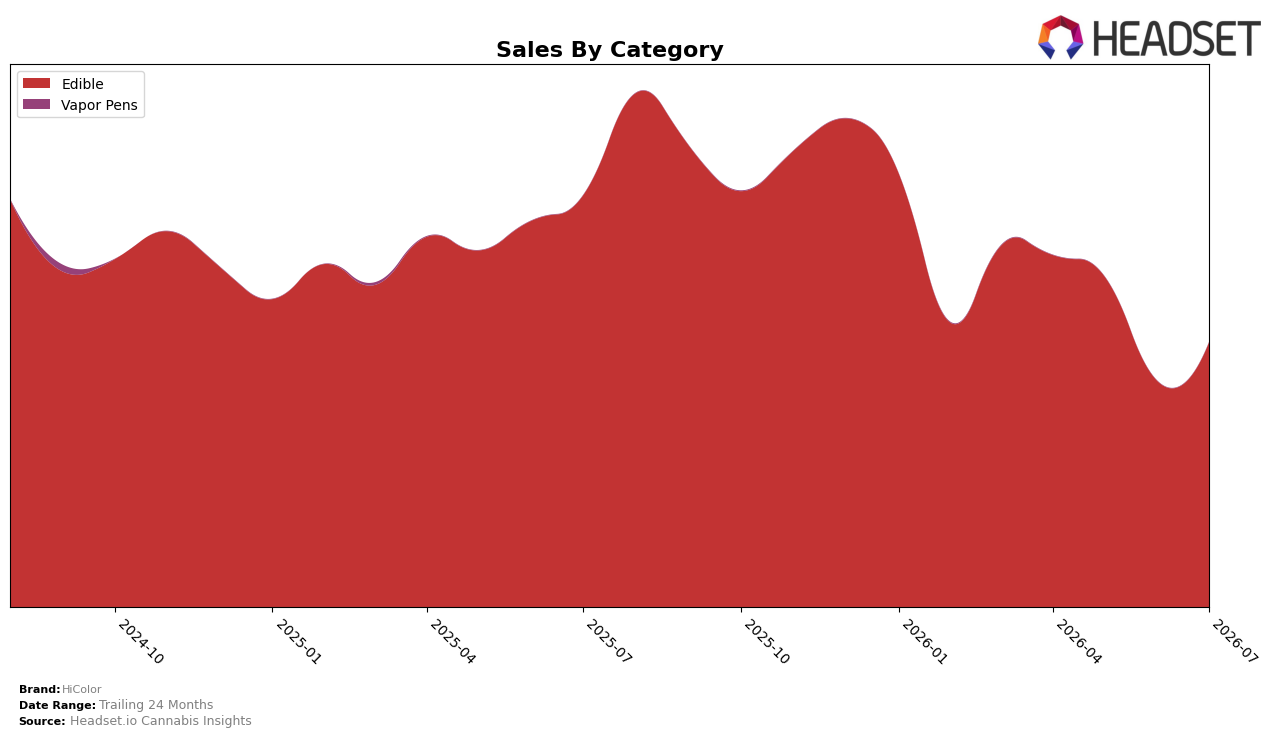

HiColor operated as a single-category brand in July 2026, with Edible at 100.0% mix and a rank of 15 in Maryland’s Edible set, combining a -35.7% year-over-year sales change with a 17.3% month-over-month gain. Average price rose 1.0% YoY to $19.22 while category share held at 100.0%, indicating that July 2026 growth was driven by intra-category velocity rather than mix expansion; the pattern implies a rebound within Edibles that is not yet offsetting the prior-year contraction.

The pairing of a 17.3% MoM lift against a -35.7% YoY contraction, alongside a 1.0% YoY price increase and a rank of 15 in Maryland, signals that July 2026 momentum is timing-sensitive and concentrated in Edible, not diversified. Given a 24-month sales change of -32.4% and a stable 100.0% category mix, the implication is that near-term gains are episodic and price-led rather than portfolio-led, positioning HiColor as an Edible specialist that must convert MoM spikes into sustained share capture to improve its rank trajectory.

Competitive Landscape

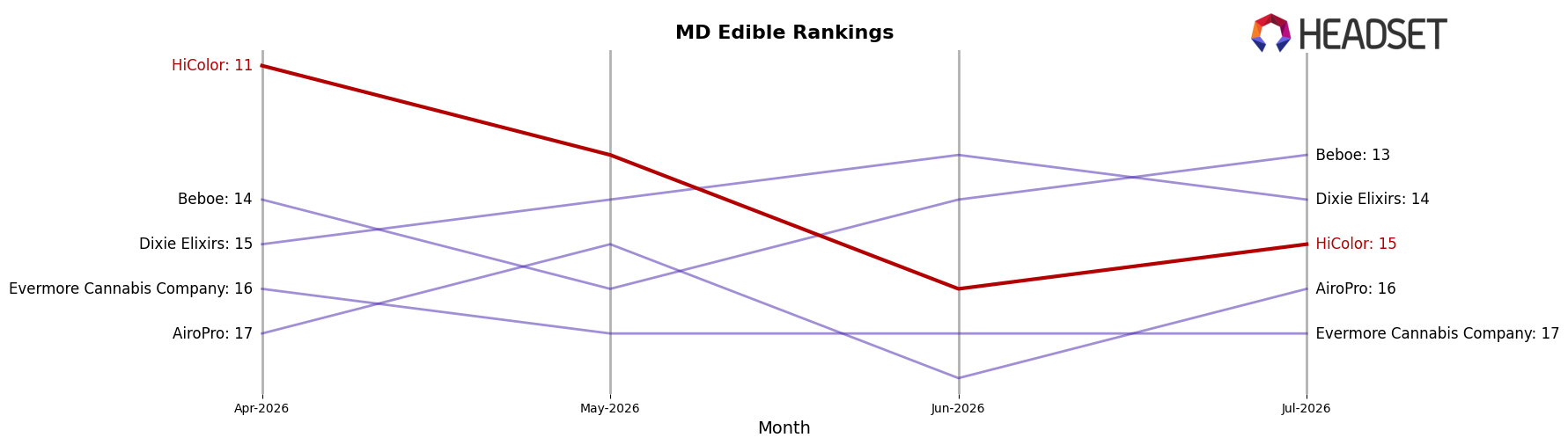

HiColor sits at rank 15 in MD Edible in July 2026, sliding 5 places year over year from rank 10 while also dropping 4 spots from rank 11 in April 2026; the brand is now 8 positions below its peak rank 7 from August 2025, indicating a sustained downshift rather than a one-month fluctuation. In contrast, Incredibles climbed from rank 3 to rank 1 year over year with 26.0% sales growth, and In House moved up from rank 6 to rank 3 alongside a 75.5% sales increase, while Wyld fell from rank 1 to rank 4 with an 18.0% sales decline, collectively signaling that HiColor’s trajectory is being outpaced by both ascending and reshuffling leaders and implies a need to reassert relevance in faster-growing subsegments.

Notable Products

Cherry RSO Gummies 10-Pack (100mg) posted the standout move in July 2026 with +84.4% month over month to rank 2, while Sour Lemon Drop RSO Gummies 10-Pack (100mg) followed closely at +82.2% MoM at rank 4. Blueberry RSO Gummy Gummies 10-Pack (100mg) held rank 1 with +42.4% MoM, but Passionfruit RSO Gummies 10-Pack (100mg) slid -30.4% MoM at rank 10, indicating divergence within flavor variants. With all top 10 positions occupied by Edible SKUs and five RSO gummy flavors in the top seven, the mix tilts toward RSO-led confections. The pattern implies HiColor is consolidating around fast-accelerating RSO gummies while pruning or repositioning lagging flavors to sustain momentum at the top ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.