Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Jams is stocked at 536 licensed dispensaries across Illinois, Florida, and 13 other states, 104 of them in Illinois, with the deepest coverage in Chicago, Naperville, Arlington Heights, Joliet, and Schaumburg. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

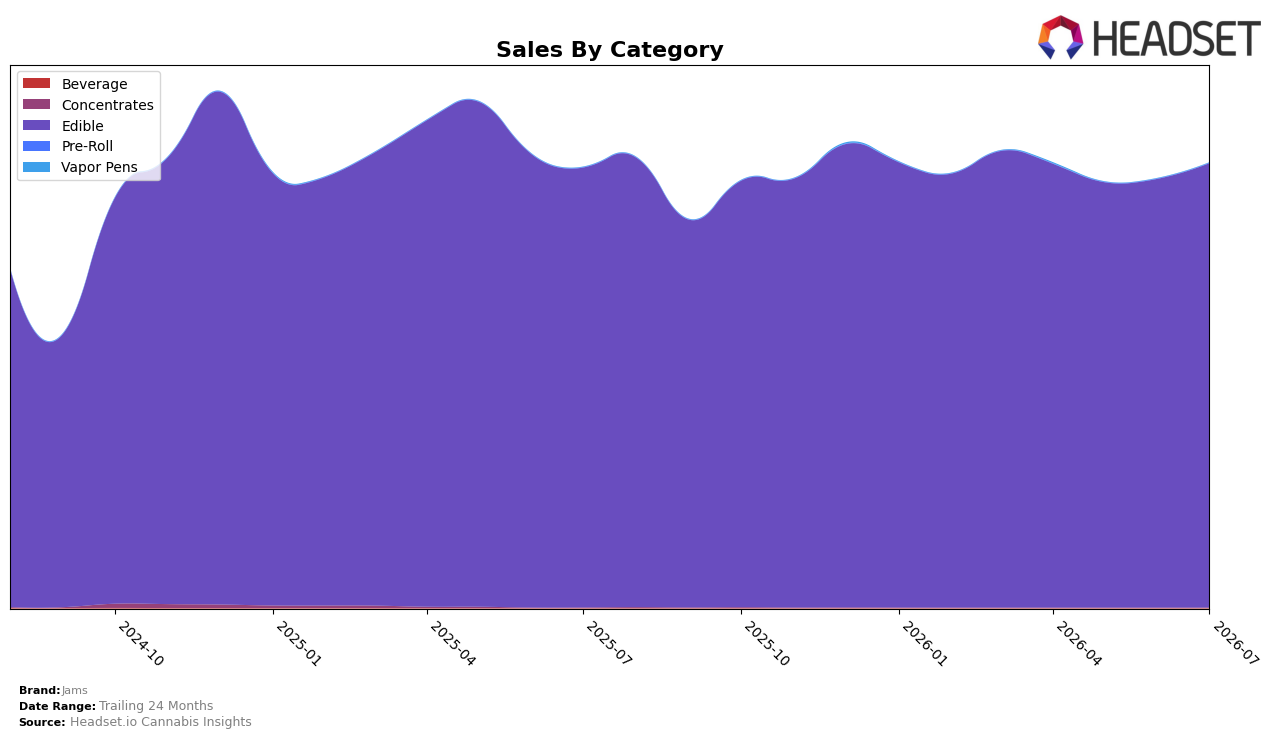

In July 2026, Jams concentrated 100.0% of sales in Edible, with category sales up 100.96% year over year and 3.63% month over month, while brand-level sales rose 98.97% YoY alongside a 12.99% YoY decline in average price. Within New Jersey Edibles, Jams held rank 5, and the category’s 3.63% MoM uplift paired with the brand’s full reliance on Edibles indicates reliance on volume expansion over price to sustain share.

The mix consolidation into a single category and a rank position of 5 in New Jersey imply Jams is competing on accessibility, with a 12.99% YoY price decrease designed to trade price for velocity while leveraging a 100.96% category YoY rise to hold position. Given the 3.63% MoM category lift against a 98.97% YoY brand gain, the pattern points to short-term stability driven by category tailwinds but longer-term risk if Edible growth normalizes, making the current pricing stance pivotal for defending rank 5.

Competitive Landscape

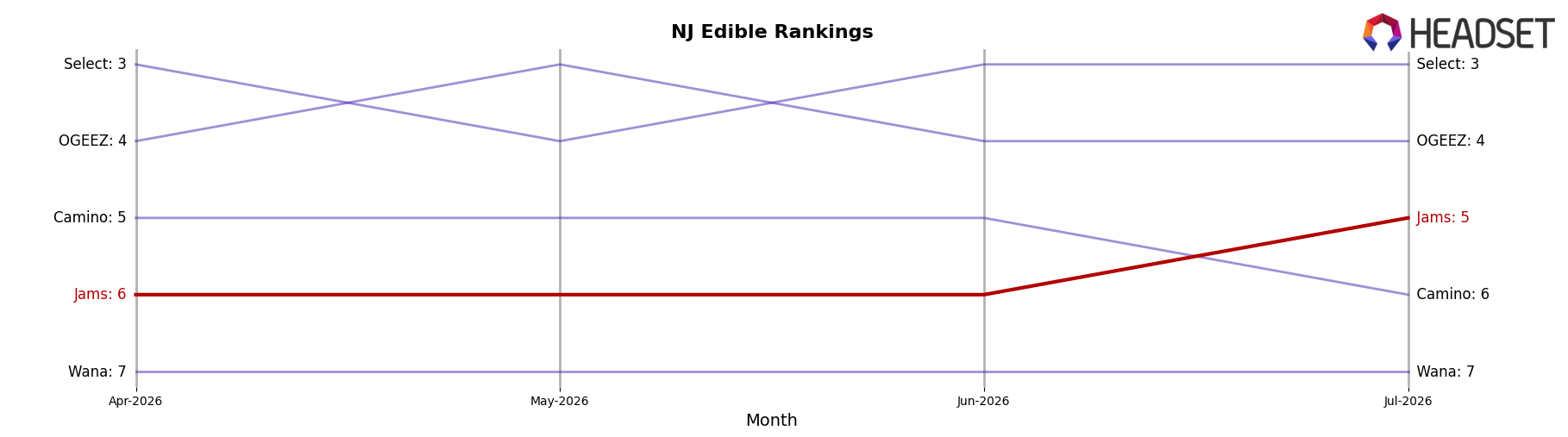

Jams ranks #5 in New Jersey Edible for July 2026, improving 1 position from #6 year over year and holding steady versus April 2026 at #6 to #5 movement; meanwhile, OGEEZ climbed from #7 to #4 and Wyld rose from #3 to #2 with a 2.8% YoY sales increase, while Select slid from #2 to #3 alongside a 34.0% YoY sales decline and category leader Gron / Grön remained #1 despite a 14.9% YoY sales contraction; given Jams’ peak of #4 in November 2025 and current #5 with only a 1-rank YoY gain, the pattern implies share is stable but upward mobility will require displacing a rising #4 challenger and leveraging softness at the top rather than relying on organic drift.

Notable Products

THC/CBD/CBN 2:1:1 Lullaberry Remix Jellies 10-Pack (100mg THC, 50mg CBD, 50mg CBN) set the pace in July 2026 with a 147% month-over-month jump and a climb to rank 1, while Sativa Sour Strawberry Lemonade Fast Acting Jellies 20-Pack (100mg) fell 9.3% to rank 3. Mixed Berry Gummies 10-Pack (100mg) surged 506% to rank 2 and surpassed the previously higher-volume fast-acting format, signaling a pivot toward 10-Pack offerings despite a single-month revenue leader at $366,475.

Eight of the top ten are Edible Jellies or Gummies, concentrating the portfolio in one format while Hybrid Peach Jellies 10-Pack (100mg) advanced 20.2% to rank 6 and Mixed Berry Jellies 20-Pack (100mg) rose 20.6% to rank 10. With rank 4 Sour Green Apple Fast Acting Jellies 20-Pack up only 0.5% and rank 8 Sour Watermelon Lime Fast Acting Jellies 20-Pack essentially flat at -0.1%, the faster growth of 10-Packs over 20-Packs implies Jams is tilting toward smaller-size, mood-targeted SKUs as the commercial focus.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.