Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Smokiez Edibles is stocked at 2,348 licensed dispensaries across California, Oklahoma, and 20 other states, 459 of them in California, with the deepest coverage in Los Angeles, Sacramento, San Francisco, San Diego, and Fresno. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

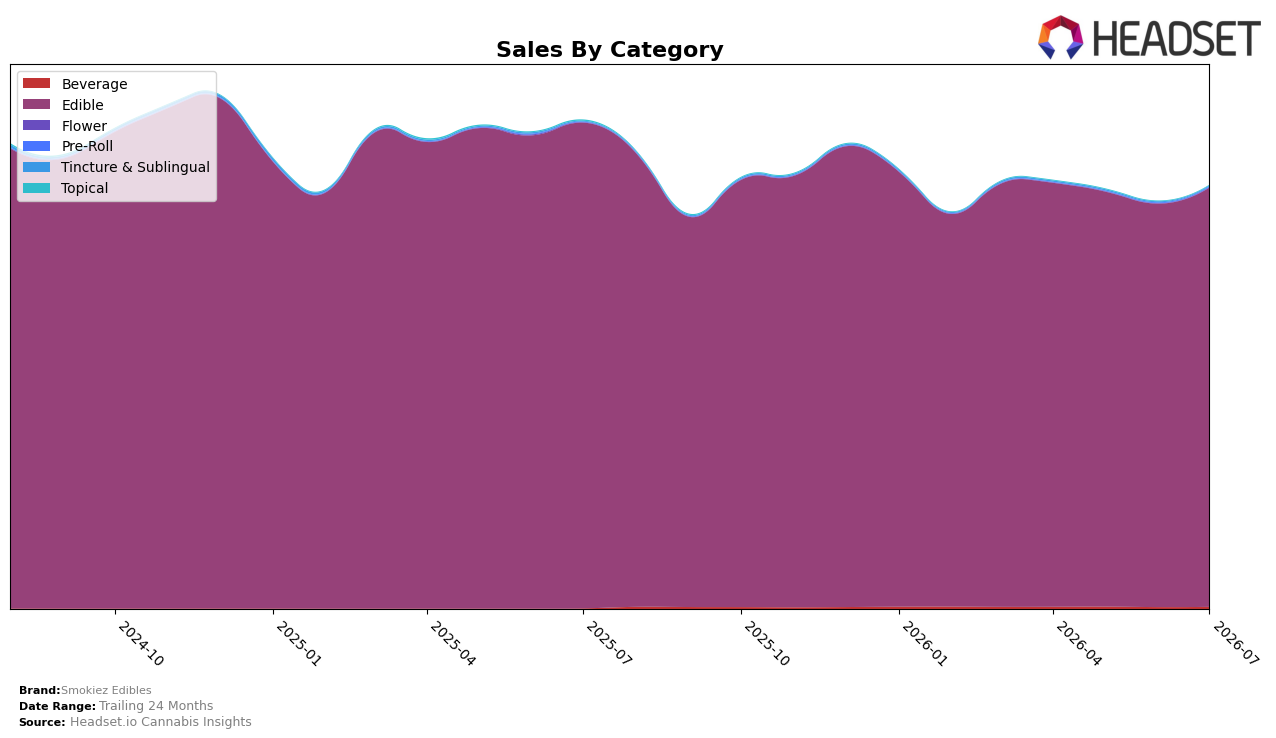

In July 2026, Smokiez Edibles remained concentrated in Edible at 99.36% share with a 3.93% month-over-month lift even as year-over-year declined 13.69%, while Beverage expanded to 0.41% share with 14.84% MoM and 650.73% YoY growth off a small base. Tincture & Sublingual held 0.11% share with a 22.55% YoY increase but fell 24.24% MoM, and Topical slipped to 0.05% share with a 75.79% YoY and 25.79% MoM decline; Pre-Roll entered at 0.07% share with 9.32% MoM. With overall brand sales down 13.39% YoY and average price down 0.59% YoY to $15.03, the mix signals a core Edible rebound in the near term while peripheral categories are testing traction without yet offsetting the Edible YoY drag.

The mix shift implies Smokiez Edibles is consolidating around Edible while probing adjacent formats to protect rank position, evidenced by a rank of 5 in Edible in Missouri and a 3.93% MoM rise that contrasts with a 13.39% brand-level YoY decline. Beverage’s 650.73% YoY and 14.84% MoM growth at a 0.41% share, alongside Tincture & Sublingual’s 22.55% YoY growth but 24.24% MoM pullback, indicates early-stage trials that can add incremental reach but currently dilute focus; the thesis is that sustaining the Edible MoM momentum while selectively scaling Beverage is the clearest path to stabilizing YoY performance without overextending into categories posting double-digit MoM declines.

Competitive Landscape

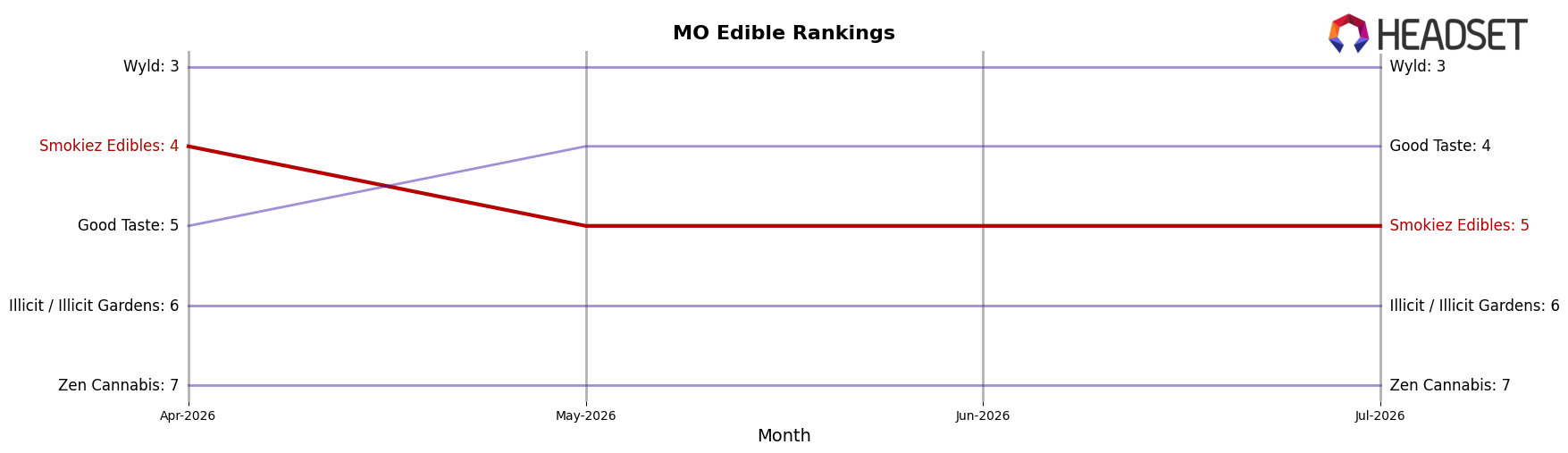

Smokiez Edibles sits at rank #5 in Missouri Edible for July 2026, a drop of 3 positions from its July 2025 peak at #2 but a 3-position improvement versus three months ago when it was #8; meanwhile, Gron / Grön holds #1 despite a -5.5% year-over-year sales change, and Good Taste rose from #8 year-over-year to #4 with a 63.8% sales increase, indicating that Smokiez Edibles’ rank stabilization at #5 amid faster upward moves by rivals implies it must convert recent quarter-on-quarter recovery into share gains or risk being outpaced.

Notable Products

Sour Blackberry Fruit Chews 10-Pack (100mg) posted the steepest setback in July 2026 with a -16.5% month-over-month drop to $132,019, falling to rank 10 while Sour Watermelon Live Resin Fruit Chews 10-Pack (100mg) inched up 3.6% to hold rank 1. Indica Sour Blue Raspberry Fruit Chews 10-Pack (100mg) advanced 8.5% to rank 4 as Sativa Sour Peach Fruit Chews 10-Pack (100mg) slipped -3.1% at rank 2, and with ten of the top ten SKUs concentrated in Edibles and multiple peach, watermelon, and blue raspberry variants in the top five, the portfolio is clustering around familiar fruit formats. The mix implies Smokiez Edibles is leaning into flavor-led line extensions where modest gains at the top counterbalance sharper softness in trailing SKUs, signaling a need to refresh lagging flavors while protecting flagship positions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.