Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

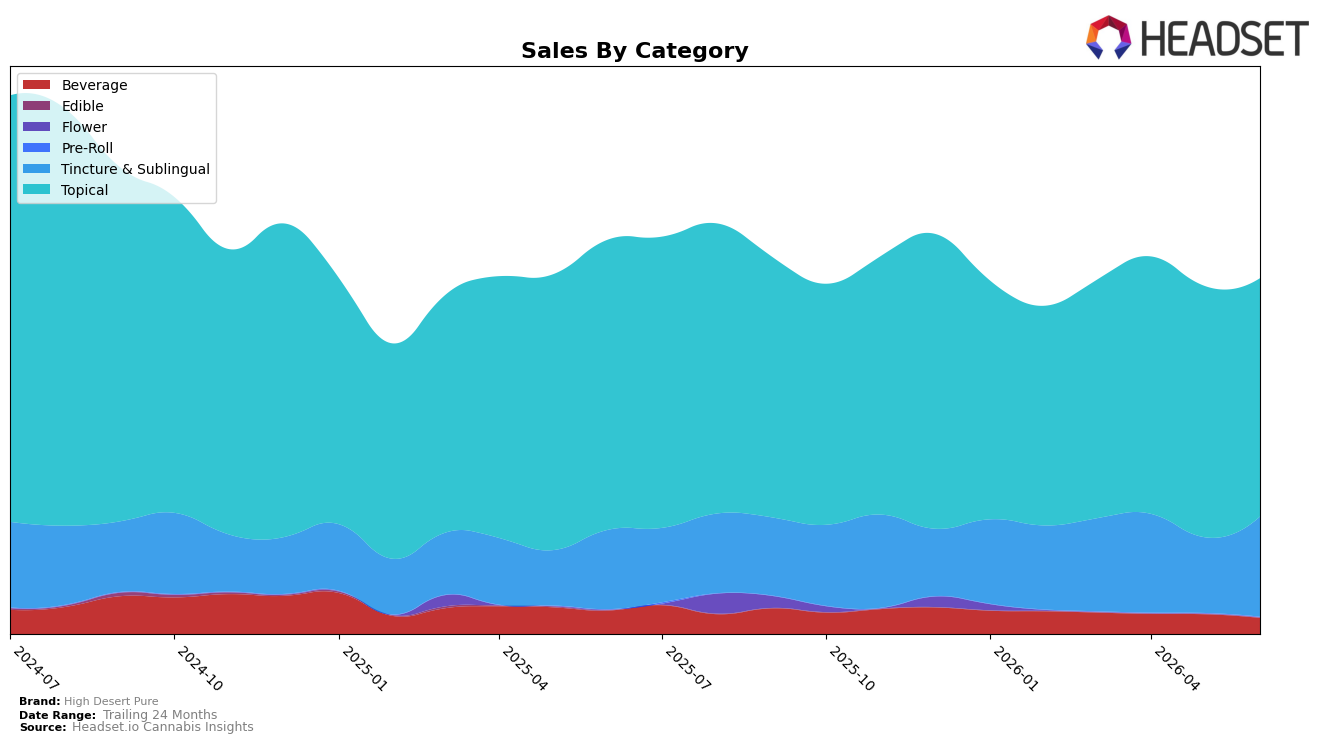

In June 2026, High Desert Pure’s category mix concentrated further in Topical at 67.32% share, even as Topical sales fell 17.90% year over year and 5.16% month over month, indicating contraction in its anchor segment. Tincture & Sublingual expanded to 28.20% share with 26.32% YoY growth and a 32.38% MoM jump, shifting incremental weight toward a faster-moving format. Beverage slipped to 4.48% share with a 31.80% YoY decline and an 18.84% MoM drop, trimming peripheral exposure. The average price fell 8.08% YoY to $36.80 while Topical pricing sat higher at $40.04, suggesting mix and price both pressured June 2026 revenue as overall brand sales declined 9.86% YoY, and the pattern implies the brand is relying on Tincture & Sublingual momentum to offset softening in its core.

The shifts imply a repositioning from a single-segment Topical identity toward a two-pillar portfolio where Tincture & Sublingual acts as the growth hedge while Beverage recedes. With High Desert Pure ranked 1 in Topical in Oregon but facing a 17.90% YoY and 5.16% MoM Topical slide, the brand’s leadership is being maintained through share concentration rather than growth, raising risk if category headwinds persist. The 32.38% MoM surge in Tincture & Sublingual alongside a lower $33.50 average price relative to Topical’s $40.04 indicates a tilt toward accessible price points and potentially higher unit velocity, implying near-term volume defense but continued margin pressure if mix continues shifting away from premium-priced Topical.

Competitive Landscape

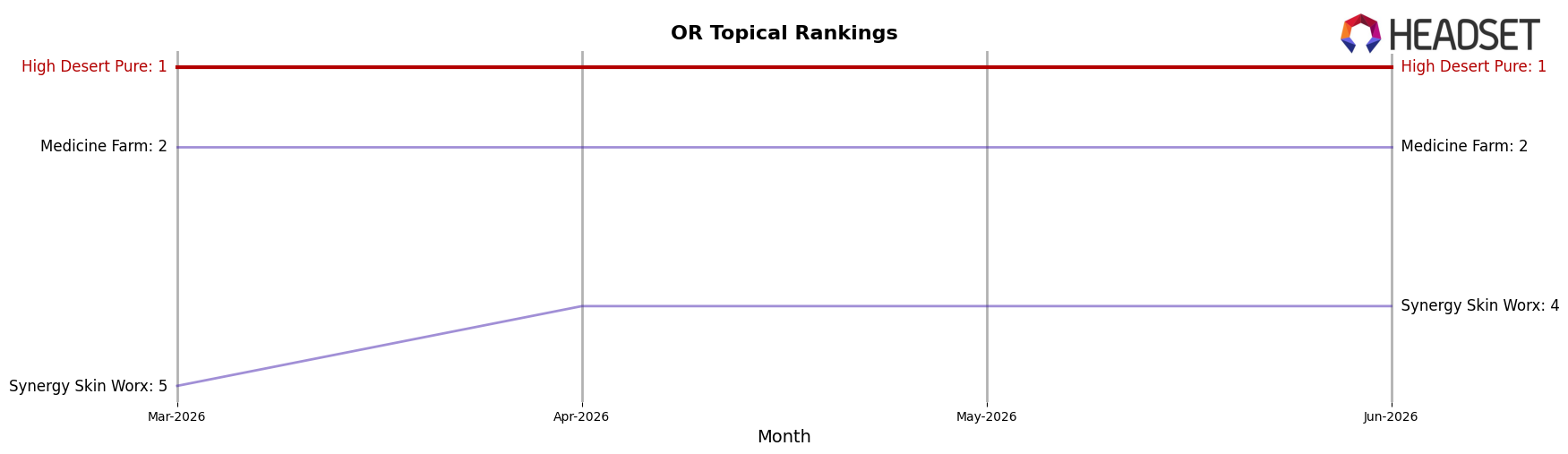

High Desert Pure holds rank #1 in OR Topical in June 2026 with no year-over-year rank change from #1, and no three-month movement from #1, indicating a flat but defended lead while the category shuffled beneath it; Medicine Farm stayed at #2 year-over-year and in June 2026, while Buddies remained at #3 as its sales declined 23.35% year over year, and Synergy Skin Worx climbed from #5 to #4 alongside a 6.19% sales increase. With Angel (OR) sliding from #4 to #5 on a 35.96% sales decline and Medicine Farm’s sales up 5.92% year over year, the competitive pressure concentrates in the #2–#4 corridor rather than threatening #1 directly; the thesis is that a stationary #1 amid downward movement at #3 and #5 and only modest uplift at #2 implies High Desert Pure’s leadership is anchored more by competitors’ mixed momentum than by incremental share capture, which could cap upside if an improving #2 converts its 5.92% growth into rank gains.

Notable Products

CBD/THC 1:1 Light Tropic Lotion (200mg CBD, 200mg THC, 100ml) led the movement with a -27.9% month-over-month decline to rank 5, while the top-ranked CBD/THC 1:1 Ginger Lime Lotion (750mg CBD, 750mg THC, 3.5fl oz) also fell -21.5%, signaling a pullback in flagship Topicals. In contrast, CBD/THC 1:1 Clinical Strength Menthol Lotion (750mg CBD, 750mg THC, 3.5oz) rose +11.6% at rank 3, and Tincture & Sublingual entries—Celebrate Chocolate Coconut Full Spectrum Tincture at rank 2 with +4.1% and CBD/THC/CBN 15:5:2 Hibernate Honey Almond Tincture at rank 4 with +36.1%—gained share, with four of the top ten belonging to Topical SKUs and three to Tincture & Sublingual. The Beverage Nano Chill Mango Elixir slipped -8.9% at rank 7 while the CBD/THC 1:1 Big Balm declined -18.3% at rank 6, consolidating spend toward higher-ranked pain-relief formats despite only one SKU surpassing $30,000 in June 2026. The pattern implies High Desert Pure is leaning into diversified relief formats where Tincture & Sublingual momentum offsets softness in legacy Topicals, pointing to a mix shift rather than category exit.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.