Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

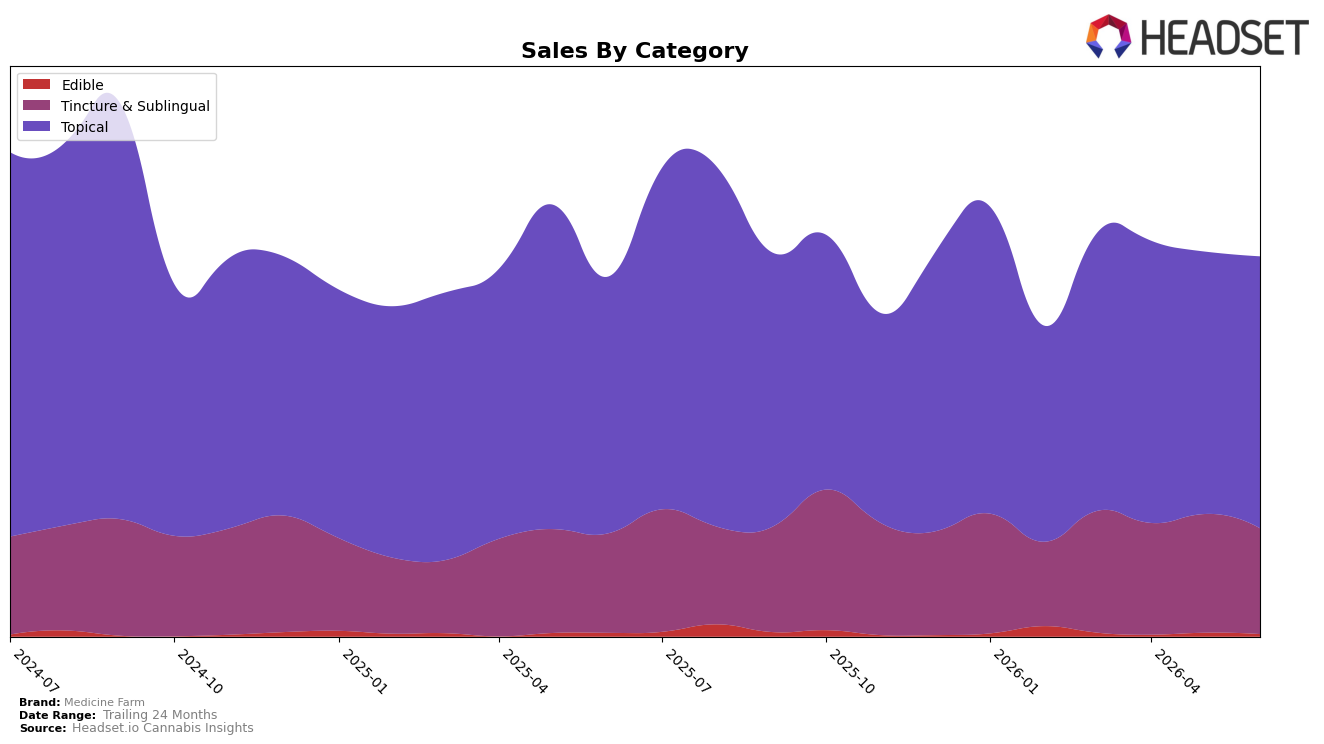

Medicine Farm concentrated 71.54% of June 2026 sales in Topical, up 3.61% month over month and 5.92% year over year, while Tincture & Sublingual held 27.80% with a 10.90% month-over-month decline but a 6.31% year-over-year gain. Edible remained marginal at 0.66% share with a 34.79% month-over-month drop and a 32.80% year-over-year decline. The mix shift indicates deeper reliance on Topical as the stabilizer for month-to-month variability and as the primary growth engine relative to June 2025.

With a Topical category rank of 2 in Oregon and an average price down 4.64% year over year to $34.33, Medicine Farm is trading price for share resilience in its core, while Tincture & Sublingual volatility (-10.90% month over month versus +6.31% year over year) signals episodic demand that won’t reliably lift total rank. The pattern implies Medicine Farm’s positioning is anchored in Topical leadership where incremental price flexibility can sustain rank, and that subscale Edible at 0.66% share with a 34.79% month-over-month contraction should be treated as optional rather than a near-term growth pillar.

Competitive Landscape

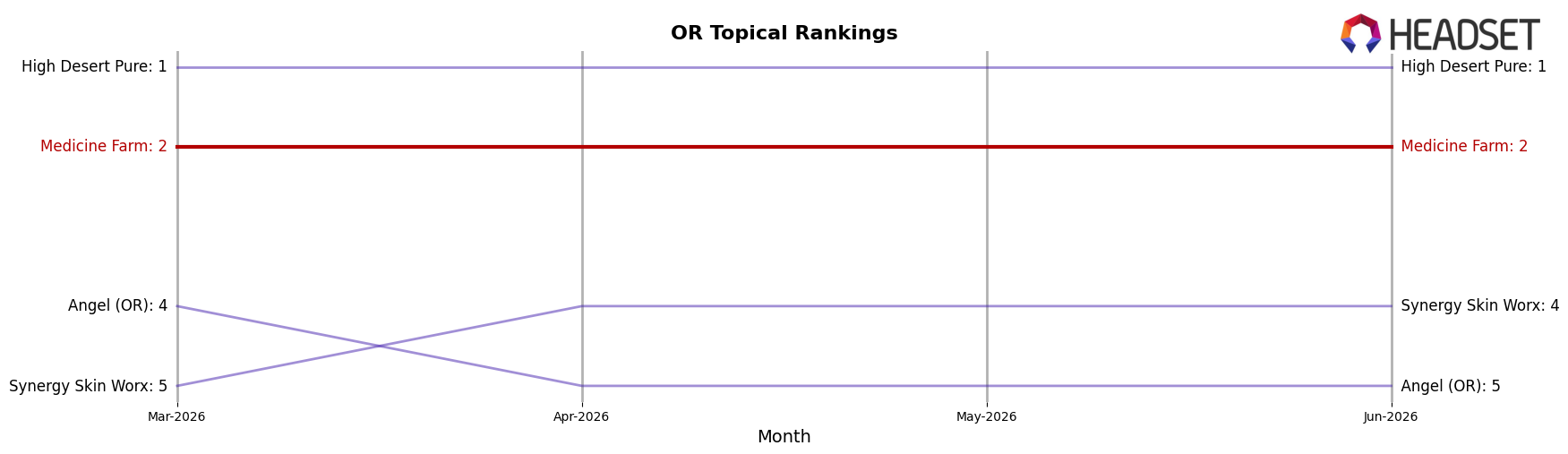

Medicine Farm sits at rank #2 in OR Topical in June 2026, unchanged year over year from #2, and also flat versus three months ago at #2, while category leader High Desert Pure holds #1 both now and a year ago with an estimated −15.0% YoY sales change and Buddies remains at #3 with an estimated −23.3% YoY sales change. Meanwhile, Synergy Skin Worx improved from #5 to #4 with an estimated +6.2% YoY sales change, whereas Angel (OR) slid from #4 to #5 with an estimated −36.0% YoY sales change; against this mix of declines above and below, Medicine Farm’s static position at #2 and peak-at-#2 status in June 2026 imply a durable ceiling just below the leader unless share shifts accelerate.

Notable Products

Extra Strength Dragons Blend Balm (65mg THC, 0.25oz) posted the standout movement in June 2026 with a 229.3% month-over-month surge into rank 5, while CBD/THC 6:1 Mini Dragon's Blend Balm (30mg CBD, 5mg THC 0.25oz) slipped 10.5% to rank 9. At the top, CBD/THC 1:1 Mini Phoenix Blend Salve (125mg CBD, 125mg THC, 0.25oz) inched up 8.0% to hold rank 1 as Phoenix Blend Balm (1000mg THC, 2oz) climbed 30.7% to rank 2. With seven of the top ten in Topical, the outsized gains in compact balms suggest Medicine Farm is tilting toward fast-turn, smaller-format topicals that can scale velocity even as some tinctures retreat 14.5% and 13.7% at ranks 4 and 8, respectively.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.