Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

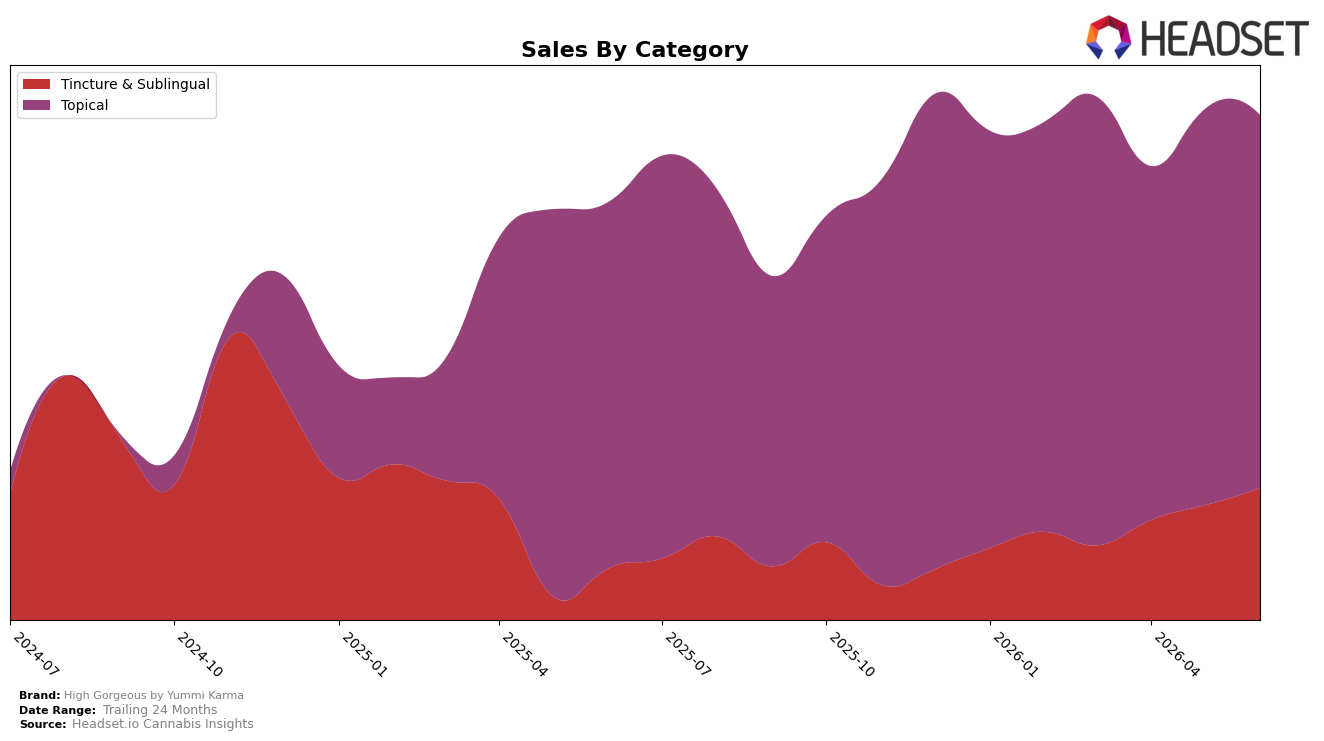

In June 2026, High Gorgeous by Yummi Karma concentrated 73.21% of sales in Topical with a modest year-over-year gain of 1.76% but a month-over-month decline of 5.68%, while Tincture & Sublingual expanded to 26.79% share on 136.89% year-over-year growth and a 14.02% month-over-month rise. The average price across the brand dipped 1.35% year over year to $34.19, with category pricing split between Topical at $31.61 and Tincture & Sublingual at $44.03; this mix, combined with overall brand sales up 20.12% year over year, indicates that growth is being pulled by higher-priced Tincture & Sublingual even as the larger Topical base softens sequentially.

These shifts reposition the brand toward a two-engine model: a stable but cooling Topical anchor ranked 11 in California and a faster-growing, premium-priced Tincture & Sublingual contributor that is lifting revenue despite slight price deflation. With Topical down 5.68% month over month but Tincture & Sublingual up 14.02% month over month, and the brand’s 24-month sales up 132.07%, the pattern implies headroom to trade mix toward higher-value formats without abandoning the core, using the Topical rank position and base to funnel trial into the faster-growth, higher-ticket line.

Competitive Landscape

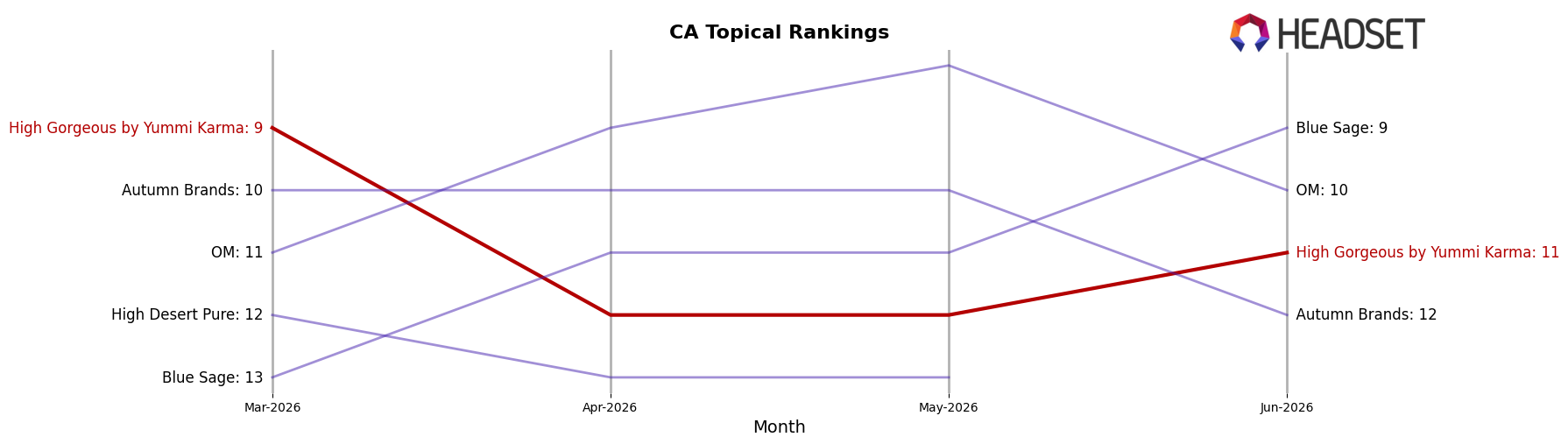

High Gorgeous by Yummi Karma sits at rank #11 in CA Topical for June 2026, unchanged from #11 year over year, after slipping 2 spots from #9 in March 2026 to #11 in June 2026; in contrast, Liquid Flower climbed from #6 to #4 while Carter's Aromatherapy Designs (C.A.D.) fell from #4 to #5 alongside a -22.2% sales change. Meanwhile, category anchors Papa & Barkley held #1 with a -4.6% sales change and Mary's Medicinals stayed at #2 with a -26.7% sales change, while growth brands like Buddies maintained #3 with +64.5% sales growth; this mix of stability at the top and upward movement from #6 to #4 among mid-tier competitors implies High Gorgeous by Yummi Karma’s flat #11 rank is at risk of further erosion unless it recaptures the #9 position momentum seen in March 2026.

Notable Products

CBD/THC/THCA 2:2:1 Pina Co Canna Lotion (200mg CBD, 200mg THC, 100mg THCa) posted the single largest move with a 1777.5% month-over-month surge to rank 3, while CBD/THC 2:1 Ice Queen Cooling Roll-On (300mg CBD, 150mg THC, 89ml) fell 60.5% to rank 5. The lead SKU, CBD/THC 1:1 Ice Goddess Cooling Roll-On (750mg CBD, 750mg THC), dipped 4.3% yet held rank 1, and the CBD Plain Jane Tincture (1000mg CBD, 30ml) rose 14.0% to rank 2. With four of the top five in June 2026 coming from Topical formats and one Tincture & Sublingual entrant holding rank 2, the pattern implies High Gorgeous by Yummi Karma is concentrating demand in pain- and relief-oriented topicals while selectively scaling a single tincture for cross-category reach.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.