Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Incredibles is stocked at 1,229 licensed dispensaries across Colorado, Illinois, and 11 other states, 271 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Aurora, Boulder, and Longmont. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

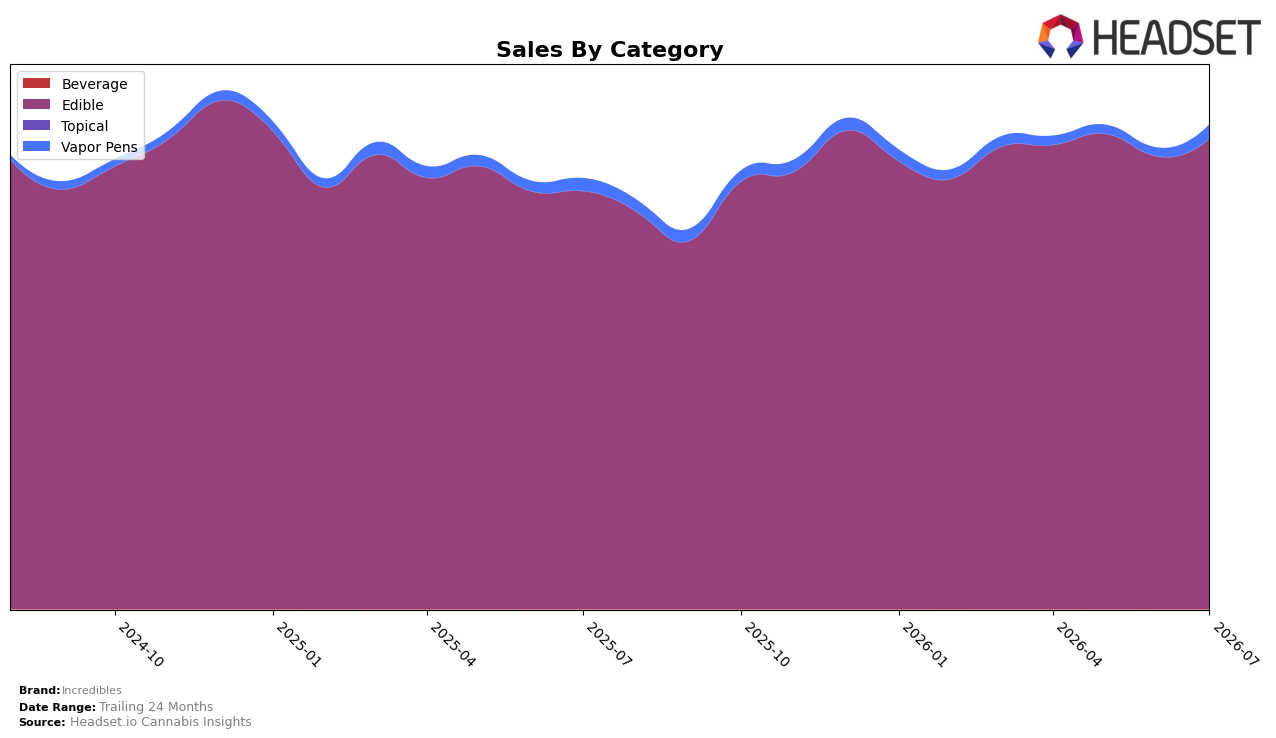

In July 2026, Incredibles concentrated 97.08% of sales in Edible, with Vapor Pens at 2.91% and Beverage near 0.00%; Edible grew 12.52% year over year and 3.91% month over month, while Vapor Pens advanced 14.36% YoY and 69.69% MoM. Average price moved down 4.46% YoY to $14.82, alongside a 3.91% MoM lift in Edible volume and a 69.69% MoM surge in Vapor Pens, indicating mix-driven unit gains; concurrently, Beverage contracted 48.91% YoY despite a 45.77% MoM uptick off a minimal base. With Incredibles ranked 1 in Edible in Illinois and MD as the top market, the pattern implies category dominance is anchored in Edible while opportunistic testing is accelerating in Vapor Pens without diluting the Edible share position.

The mix shift implies Incredibles is leveraging price elasticity in Edible (down 4.46% YoY) to sustain 12.52% YoY sales growth and incremental 3.91% MoM gains, while using a small 2.91% share in Vapor Pens to capture outsized 69.69% MoM momentum. The contrast between a 12.52% YoY increase in the core Edible line and a 48.91% YoY decline in Beverage suggests a deliberate pruning of underperforming sub-lines as the brand reinforces its number 1 Edible rank in Illinois; taken together, the data indicates a defend-and-expand posture where Edible scale funds selective expansion into Vapor Pens, preserving category leadership while testing a second pillar.

Competitive Landscape

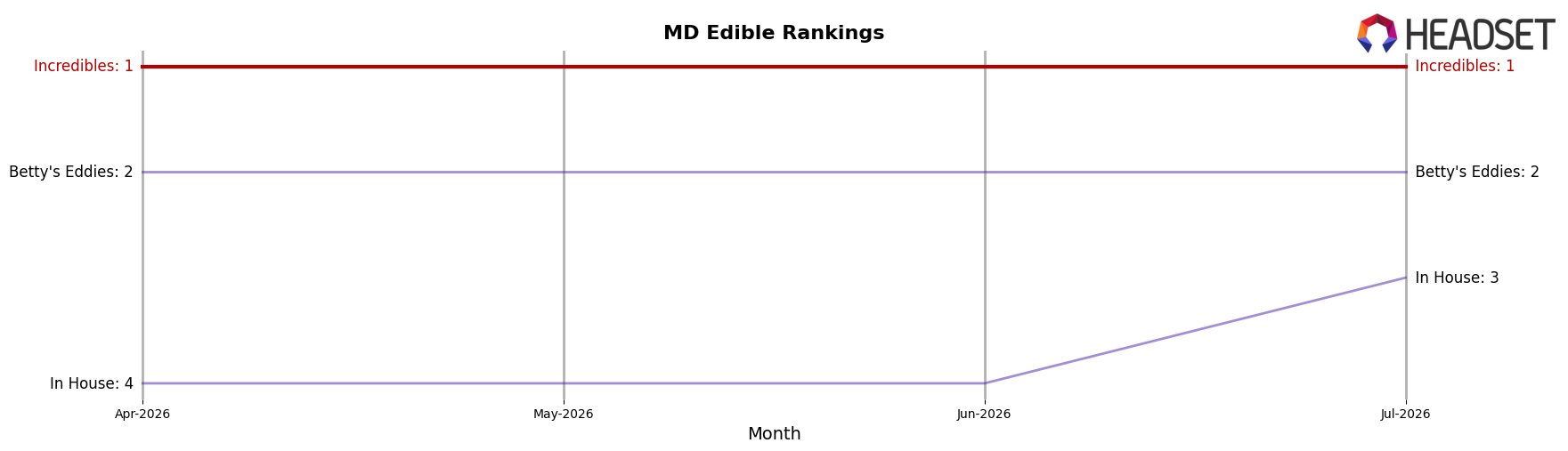

Incredibles holds rank #1 in MD Edible in July 2026, improving 2 positions year over year from #3, and retaining #1 since April 2026, while the category leader peak coincides with July 2026; by comparison, Betty's Eddies sits at #2 with a 6.6% year-over-year sales increase yet no rank gain from #2, and Wyld slid from #1 to #4 alongside an 18.0% sales decline, indicating that Incredibles’ ascent is less about broad category lift and more about displacing prior leaders. The competitive gap also widened as In House climbed from #6 to #3 on 75.5% sales growth while Curio Wellness stayed at #5 with an 11.1% decline, which implies Incredibles’ current #1 trajectory is anchored by outperformance versus both declining incumbents and fast-rising challengers rather than transient seasonality.

Notable Products

Pineapple Express Fast Acting Gummies 10-Pack (100mg) posted the steepest movement in July 2026 with a -24.3% month-over-month decline at rank 6, while THC/CBN 5:1 Snoozzzeberry Gummies 10-Pack (100mg THC, 20mg CBN) advanced +13.7% to hold rank 2. The category is concentrated, with all top ten SKUs in Edible, and CBN/CBG/THC 1:1:2 Snoozzzierberry Gummies 10-Pack (50mg CBN, 50mg CBG, 100mg THC) in rank 1 grew +2.5% despite mixed momentum across the list. With Greener Apple Fast Acting Gummies 10-Pack (100mg) up +34.5% at rank 5 against a -7.8% slide for THC/CBG 1:1 Sour Blue Razzberry Gummies 10-Pack (100mg THC, 100mg CBG) in rank 8, the tilt favors fast-acting fruit variants over balanced minor-cannabinoid formats. The mix implies Incredibles is leaning into fast-acting and sleep-adjacent gummies to anchor share, with selective pruning likely where balanced CBG formats underperform.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.