Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Luminous Botanicals concentrated 100.0% of sales in Tincture & Sublingual, with category sales down 44.19% year over year and 40.15% month over month, while brand-wide sales fell 48.75% year over year and average price declined 8.62%. With no measurable mix outside Tincture & Sublingual and average price at $33.97, the absence of diversification combined with double-digit YoY and MoM contractions implies that the brand’s single-category exposure is amplifying downside volatility relative to broader market pacing in Oregon.

The shift toward a narrower price ladder and a 40.15% MoM sales drop within the sole category suggests a demand elasticity issue rather than a share reallocation across categories, and the 44.19% YoY category decline alongside a 48.75% brand YoY decline points to under-indexing even within Tincture & Sublingual. Given 100.0% category concentration and an 8.62% YoY price decrease, the pattern implies that price cuts have not offset volume erosion, so positioning requires either a differentiated value tier or selective expansion into adjacent formats to reduce the sensitivity that comes from single-category exposure in Oregon.

Competitive Landscape

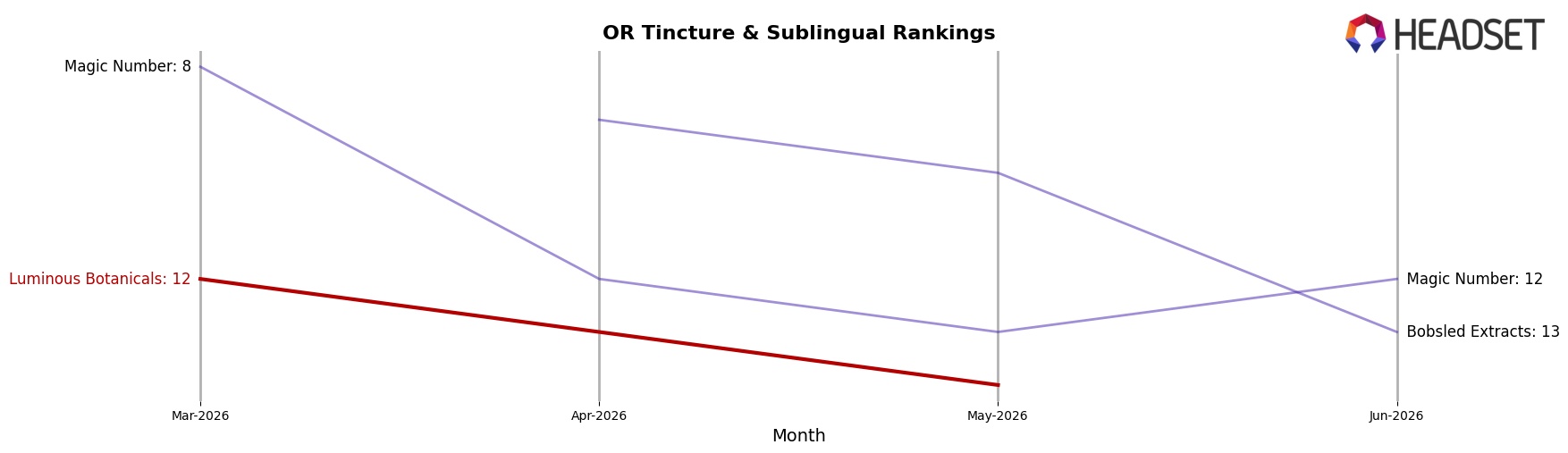

Luminous Botanicals is currently ranked #14 in OR Tincture & Sublingual in June 2026, a 2-place decline from #12 year over year, and flat versus March 2026 at #12 moving to #14 by June 2026; this contrasts with Angel (OR) holding #1 year over year at #1 and Farmer's Friend Extracts rising from #3 to #2 alongside a 28.6% sales growth, while Luminous Botanicals’ peak of #11 in July 2025 now sits three spots higher than its current #14. With category leaders such as High Desert Pure steady at #4 and Crown B Alchemy climbing from #7 to #5 as their sales grew 22.8%, the brand’s 2-rank YoY slide and 3-position gap from its peak imply share is consolidating upward, suggesting Luminous Botanicals must improve velocity or assortment to avoid further drift from the top 10.

Notable Products

CBD:THC Sky Blend Tincture (40mg CBD, 340mg THC, 15ml, 0.5oz) posted the largest movement in June 2026 with a 142% month-over-month surge into a tied rank 1 position, while CBD/THC 1:1 Meadow Blend Tincture (375mg CBD, 375mg THC,30ml) fell 79% to rank 3, signaling a pivot toward higher-THC micro-size formats. The 1:1 Meadow Blend Tincture (189mg CBD, 180mg THC, 15ml, 0.5oz) rose 45% at rank 1, whereas the CBD/THC 9:1 Earth Blend Tincture (675mg CBD, 75mg THC, 1oz) dropped 34% at rank 2, concentrating wins at the top while eroding mid-tier CBD-forward options. With all listed top-10 items in Tincture & Sublingual and one 1oz Sky Blend variant down 41% despite the 15ml Sky Blend’s triple-digit rise, the pattern implies demand is consolidating in potent, smaller bottles, guiding assortment toward compact SKUs even if it cannibalizes larger formats and CBD-heavy ratios.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.