Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Manzanita Naturals is stocked at 75 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Francisco, Santa Rosa, San Jose, and Santa Ana. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

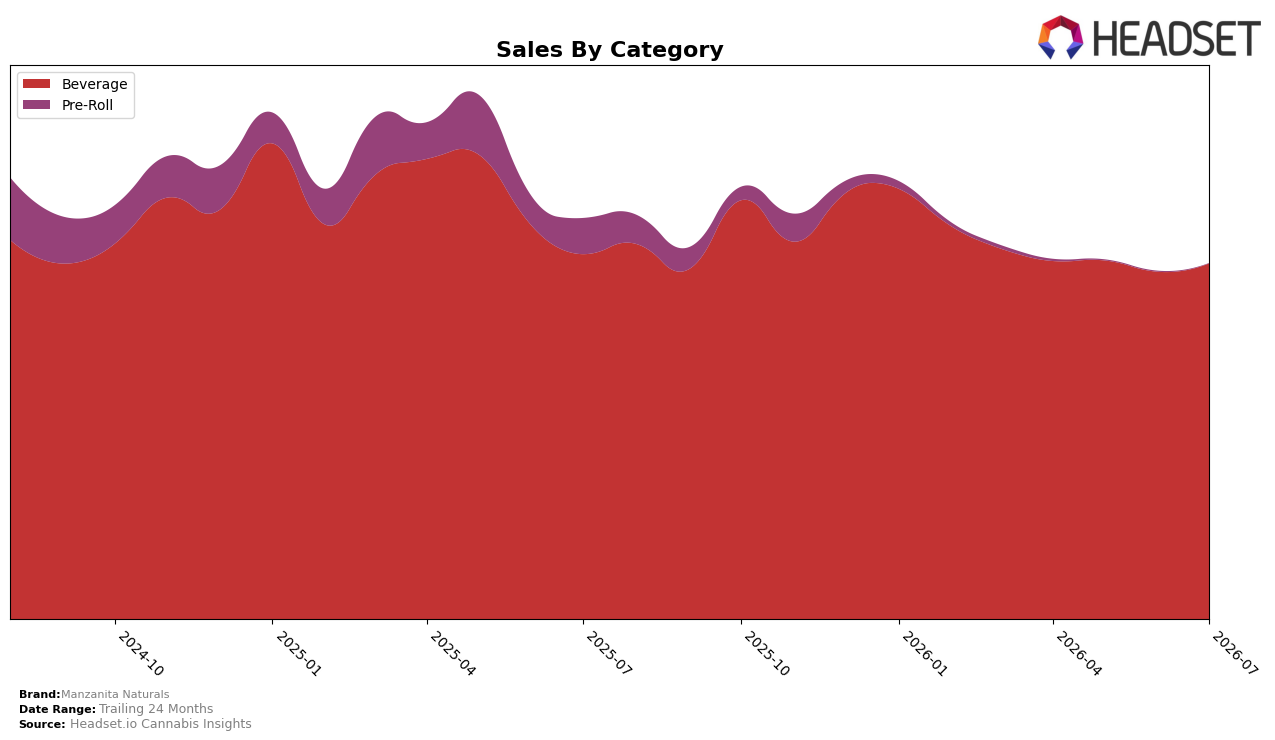

Manzanita Naturals concentrated 99.92% of July 2026 sales in Beverage, up 2.40% month over month while Pre-Roll fell 68.29% MoM to 0.08% share; year over year, Beverage declined 2.54% as Pre-Roll contracted 99.19% YoY. Average price decreased 8.42% YoY to $6.57 alongside a 2.40% MoM volume lift in Beverage implied by mix stability, while total brand sales fell 11.23% YoY, indicating price pressure outpacing any category-led volume offsets; the pattern implies a deliberate retrenchment to a single-category core with pricing concessions used to defend throughput rather than expand breadth.

Within California Beverage, the brand’s rank at 7 and a 2.40% MoM Beverage gain alongside a 2.54% YoY Beverage decline suggest share defense locally while ceding ground year over year; combined with an 8.42% YoY price cut and a 99.19% YoY collapse in Pre-Roll, the mix points to a value-forward Beverage posture rather than multi-category reach. With 99.92% of sales anchored in Beverage and total sales down 11.23% YoY, the implication is that near-term positioning centers on depth in a single aisle to protect rank 7, trading margin for velocity, while the near-elimination of Pre-Roll reduces optionality for cross-category shopper capture.

Competitive Landscape

Manzanita Naturals sits at #7 in CA Beverage in July 2026, down 1 rank from #6 year over year, and unchanged from #7 over the latest three months, while its historical peak of #3 in November 2024 underscores a multi-quarter comedown. In contrast, St Ides held #1 both this year and last (+17.2% YoY sales), and CANN Social Tonics climbed from #7 to #5 with +65.0% YoY sales, indicating share reallocation toward faster-growing rivals. Meanwhile, Almora Farms moved from #5 to #4 with +52.8% YoY sales and Uncle Arnie's stayed at #2 alongside +33.5% YoY sales, two moves that bookend Manzanita Naturals at #7 and reduce upward mobility; the pattern implies the brand is ceding relative position to competitors with double-digit YoY momentum and needs a catalyst to reverse a 1-rank YoY decline and recover toward its #3 peak.

Notable Products

The Fizz - Lime Sparkling Water (100mg THC, 355ml) posted the steepest move in July 2026 with a -20.6% MoM drop while sliding to rank 10, contrasted by The Fizz - Ganja Blast Soda (100mg THC, 12oz, 355ml) rising +34.6% to rank 3. Kwik Zzz's - Indica Kushberry Shot (100mg, 2oz, 59ml) held rank 1 with a modest +2.4% MoM, while The Fizz - Orange Cola Soda (100mg THC, 12oz, 355ml) climbed +26.3% to rank 2; meanwhile, The Fizz - Strawberry Sparkling Water (10mg THC, 12oz, 355ml) fell -15.0% at rank 8. With eight of the top ten SKUs in Beverage and multiple The Fizz variants splitting between 100mg soda gains and 10mg sparkling water declines, the mix points to a tilt toward higher-potency, flavor-forward sodas over lighter sparkling formats, implying near-term focus on reinforcing 100mg soda depth over breadth in low-dose line extensions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.