Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

CANN Social Tonics is stocked at 305 licensed dispensaries across California, Connecticut, and 3 other states, 273 of them in California, with the deepest coverage in Los Angeles, San Diego, Santa Rosa, San Francisco, and Costa Mesa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

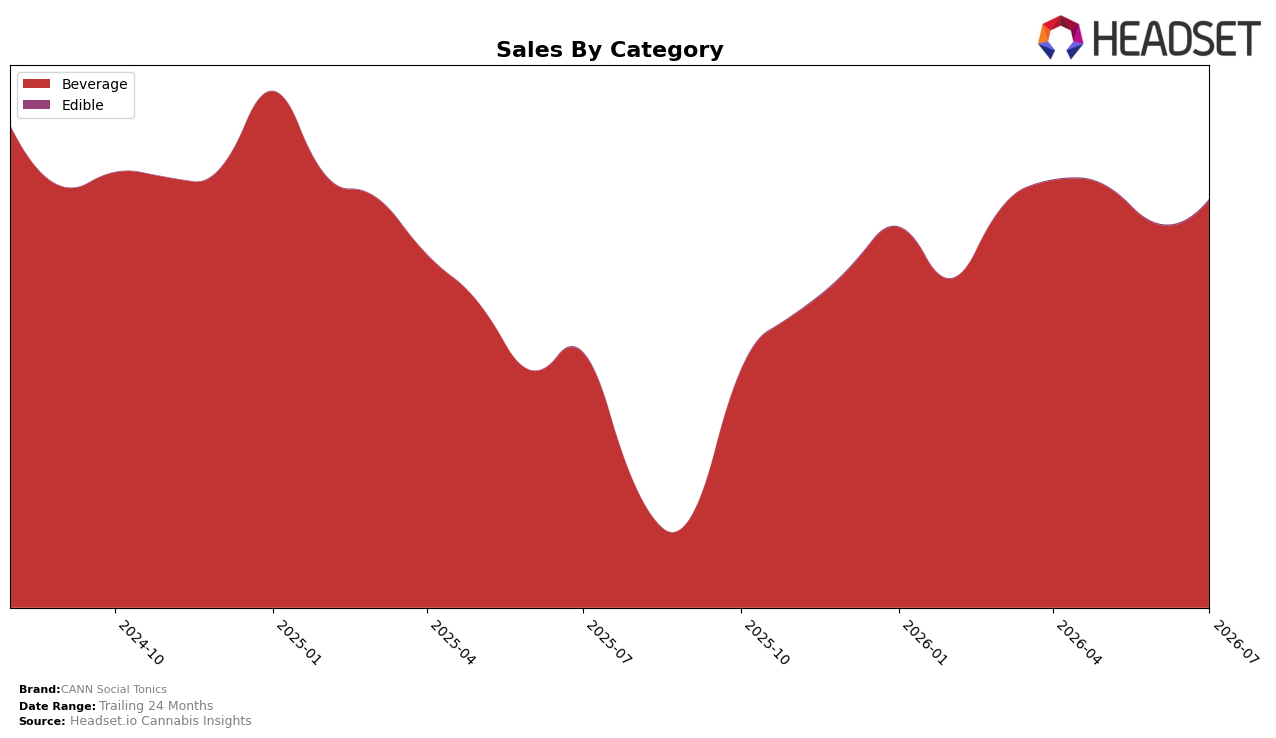

In July 2026, Beverage accounted for 99.72% share with year-over-year growth of 60.25% and month-over-month growth of 6.38%, while Edible held 0.28% share but expanded 51.29% YoY and 55.60% MoM. Average price fell 3.92% YoY to $14.81, with Beverage at $14.81 and Edible at $17.49, and brand-level sales rose 60.22% YoY despite a 24-month decline of 17.30%. With Beverage still the anchor and Edible surging from a small base, the pattern implies CANN Social Tonics is consolidating dominance in its core while testing an adjacent format that is scaling quickly but remains strategically small.

The mix shift—stable Beverage share at 99.72% alongside a 55.60% MoM spike in Edible—suggests the brand is using incremental Edible velocity to complement a 6.38% MoM Beverage climb without diluting focus. Holding a rank of 3 in Beverage in Connecticut while prices eased 3.92% YoY indicates a value-led stance that trades slight price compression for broader throughput, implying positioning as a high-frequency choice in drinks with selective Edible experimentation to capture new occasions.

Competitive Landscape

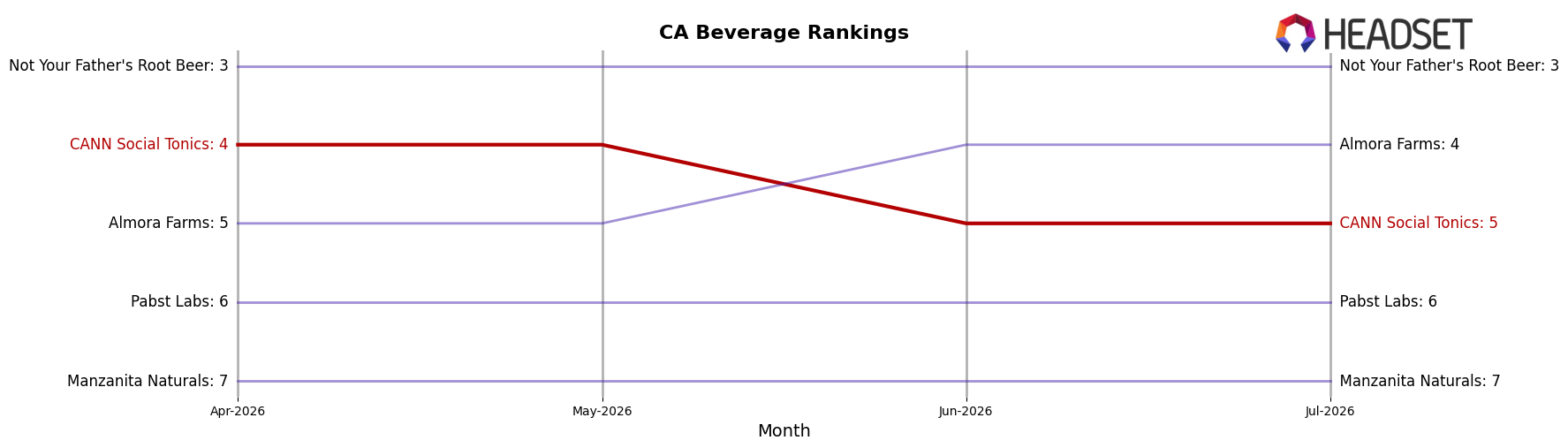

CANN Social Tonics ranks #5 in CA Beverage in July 2026, improving 2 positions year over year from #7 but slipping 1 rank from April 2026’s #4, while its historical peak was #3 in March 2025; against competitors, St Ides held at #1 with 17.2% YoY sales growth and Almora Farms moved up from #5 to #4 with 52.8% YoY growth, indicating that CANN Social Tonics’ modest upward YoY rank shift is being pressured by faster-growing rivals like Uncle Arnie's at #2 with 33.5% YoY growth and Not Your Father's Root Beer at #3 with 52.4% YoY growth; the pattern implies a plateau risk where incremental YoY rank gains are at risk of reversal unless CANN Social Tonics accelerates growth enough to counter recent quarter-over-quarter slippage.

Notable Products

CBD/THC 2:1 Blood Orange Cardamom Social Tonic (6mg CBD, 3mg THC, 12oz, 355ml) delivered the standout move in July 2026 with a +62.6% month-over-month surge to rank 2, while the CBD/THC 2:1 Lemon Lavender Social Tonic 6-Pack (24mg CBD, 12mg THC, 7.5oz, 222ml) held rank 1 with a modest +4.1% gain. Four of the top ten are CBD/THC 2:1 SKUs concentrated in Lemon Lavender and Blood Orange Cardamom, and the CBD/THC 2:1 Blood Orange Cardamom Social Tonic 6-Pack (24mg CBD, 12mg THC, 7.5oz, 222ml) added +10.1% at rank 4 while Hi Boy - Blood Orange Cardamom Social Tonic 4-Pack (20mg THC, 12oz, 355ml) slipped -6.7% at rank 5. The contrasting +20.9% lift for CBD/THC 2:1 Lemon Lavender Social Tonic (6mg CBD, 3mg THC, 12oz, 355ml) at rank 3 and -5.6% softness for Hi-er Boy - Blood Orange Cardamom Social Tonic (10mg THC, 12oz, 355ml) at rank 8 signals a tilt toward balanced CBD/THC formats over higher-THC variants. The product mix implies CANN Social Tonics is consolidating growth around 2:1 flavor families and multi-pack convenience while de-emphasizing single-serve high-THC lines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.