Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Not Your Father's Root Beer is stocked at 708 licensed dispensaries across California, with the deepest coverage in Los Angeles, Sacramento, San Francisco, San Diego, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

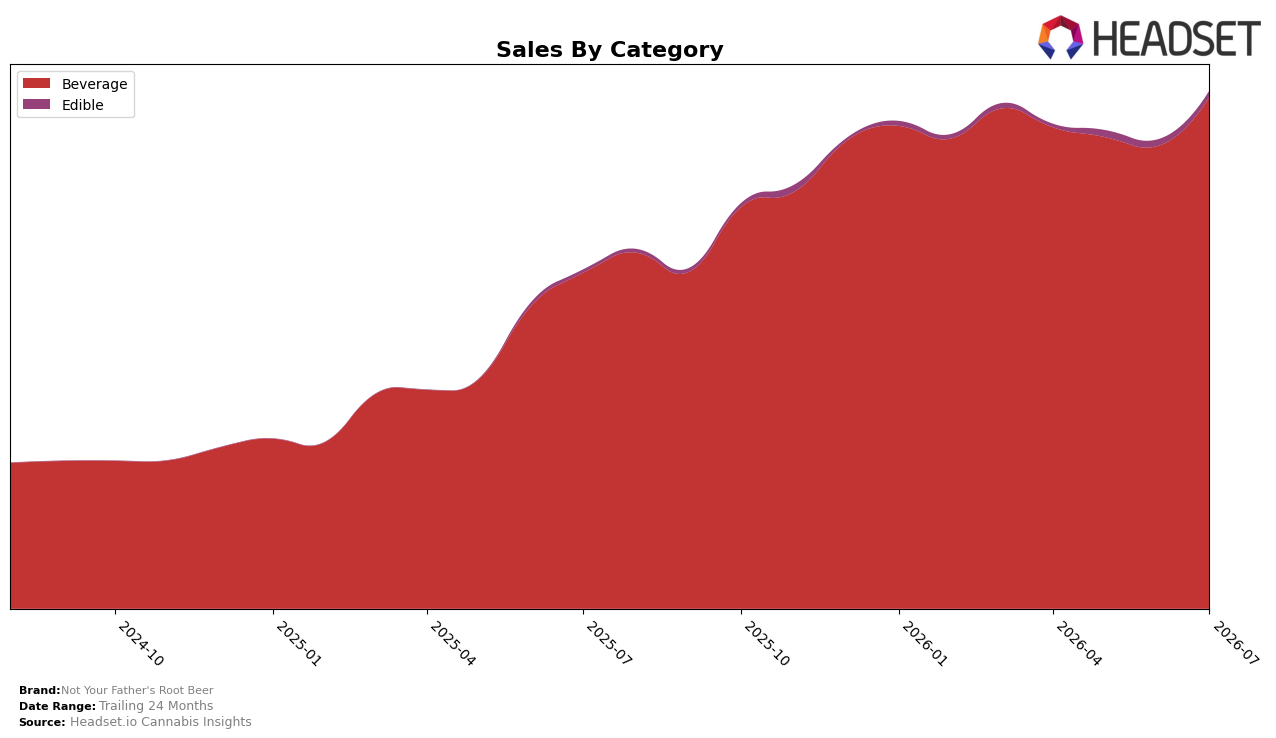

Not Your Father's Root Beer concentrated 98.81% of July 2026 sales in Beverage, with Edible at 1.19%, and the brand’s overall year-over-year growth of 52.86% aligned with Beverage’s 52.36% YoY while Edible outpaced at 109.15% YoY. Month over month, Beverage advanced 10.55% as Edible dipped 0.54%, and the average price declined 3.99% YoY to $7.90, keeping Beverage’s $7.90 roughly in line with the brand average while Edible priced at $7.64. The pattern implies that July 2026 growth was volume-led within Beverage rather than price-led, with a small but faster-growing Edible niche that is not yet contributing meaningfully to mix despite outsized YoY growth.

Within California Beverage, the brand held rank 3 while leaning into a near-single-category posture (98.81% share of mix) that amplified month-over-month gains of 10.55% in Beverage and de-emphasized the 0.54% MoM softness in Edible. With 24-month sales up 257.50% against a concurrent 3.99% YoY price decrease, the trajectory suggests a scale strategy predicated on share capture via accessible pricing rather than category diversification, implying that sustaining rank 3 will depend on defending Beverage velocity more than expanding the 1.19% Edible footprint.

Competitive Landscape

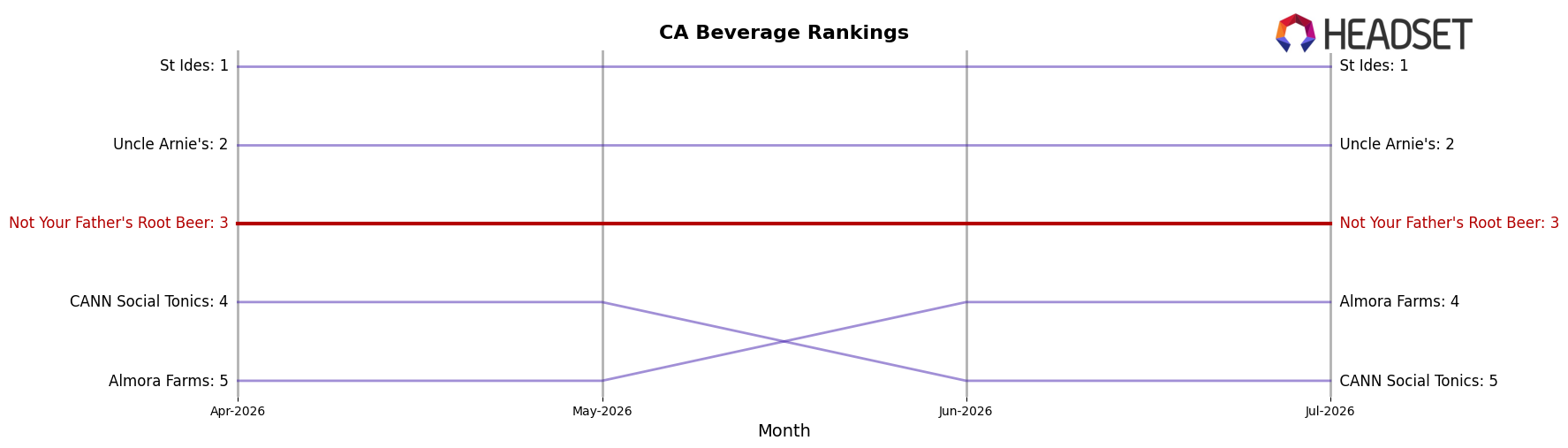

Not Your Father's Root Beer is ranked #3 in CA Beverage in July 2026, unchanged from #3 year over year, with a flat 0-place shift since April 2026 and no movement from its #3 position over the last three months; by contrast, St Ides holds #1 with a +0 YoY rank change and 17.2% YoY sales growth, while Uncle Arnie's sits at #2 with a +0 YoY rank change and 33.5% YoY sales growth, and Almora Farms moved up from #5 to #4 alongside 52.8% YoY growth; this stable #3 rank coupled with competitors’ upward momentum implies a holding pattern where Not Your Father's Root Beer must either gain share from #2 or defend against a rising #4 to avoid downward pressure on its position.

Notable Products

CBD/THC 1:4 Orange Cream Live Resin Soda (25mg CBD, 100mg THC, 16oz) posted the largest movement in July 2026 with +25.1% MoM at rank 3, while Root Beer Soda (100mg THC, 16oz, 355ml) rose +15.1% to hold rank 1, indicating mix shift toward functional/cannabinoid-blended SKUs alongside the flagship. Alpine Splash Live Resin Soda (100mg THC, 16oz) advanced +12.2% at rank 2, and eight of the top ten are Beverage SKUs within the soda family, concentrating demand around format rather than flavor experimentation; the only decline among the top ten was Fruit Punch Soda (100mg THC, 16oz, 355ml) at -1.4% and rank 9. With rank 1, 2, and 3 all growing double digits and the flagship alone generating $230,853, the pattern implies that Not Your Father's Root Beer is consolidating share by leaning into high-dosage, live-resin and CBD/THC ratio variants that reinforce a single-package, high-potency consumption occasion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.