Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

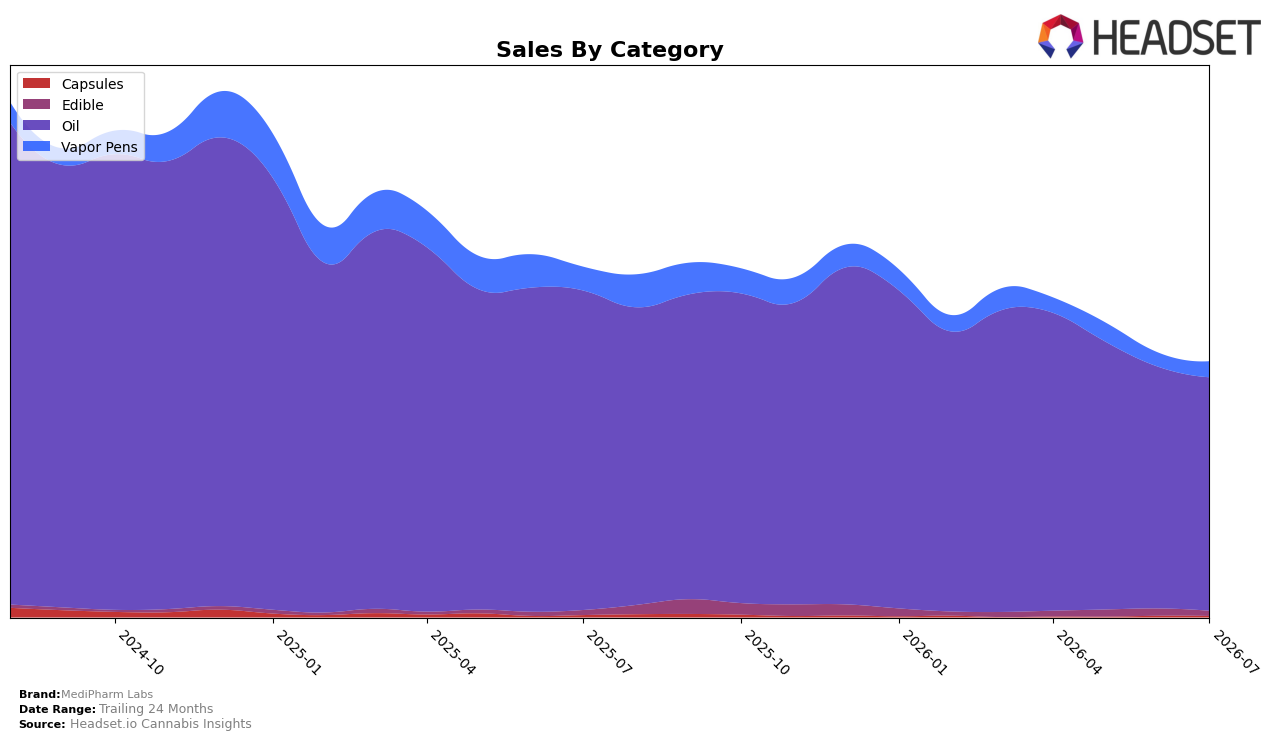

In July 2026, MediPharm Labs concentrated 90.69% of sales in Oil, where category sales fell 26.87% year over year and 3.41% month over month, while Vapor Pens held 6.39% share with a 32.16% year-over-year decline but a 12.47% month-over-month rebound. Edible remained a small 2.15% share with a 1.55% year-over-year increase offset by a 28.36% month-over-month drop, and Capsules at 0.77% declined 30.46% year over year and 7.27% month over month; against this mix, total brand sales were down 26.83% year over year and average price decreased 3.94%. The pattern implies the brand’s heavy Oil dependence is amplifying overall contraction despite a short-term lift in Vapor Pens, and the month-over-month volatility in Edible suggests limited cushion for demand swings.

Positionally, the Oil-led concentration coincides with a number 1 rank in Oil in Alberta, yet Oil’s 26.87% year-over-year contraction and 3.41% month-over-month slip indicate that leadership is tied to a shrinking core, while the 12.47% month-over-month increase in Vapor Pens offers only a 6.39% share base to diversify. The 1.55% year-over-year growth in Edible alongside a 28.36% month-over-month drop shows testing rather than traction, and the 30.46% year-over-year decline in Capsules reinforces that peripheral formats are not offsetting the -26.83% brand-level year-over-year decline and -3.94% pricing change. This mix suggests the brand’s positioning remains defined by Oil dominance that preserves rank status but limits resilience, making incremental gains in Vapor Pens necessary to moderate category risk.

Competitive Landscape

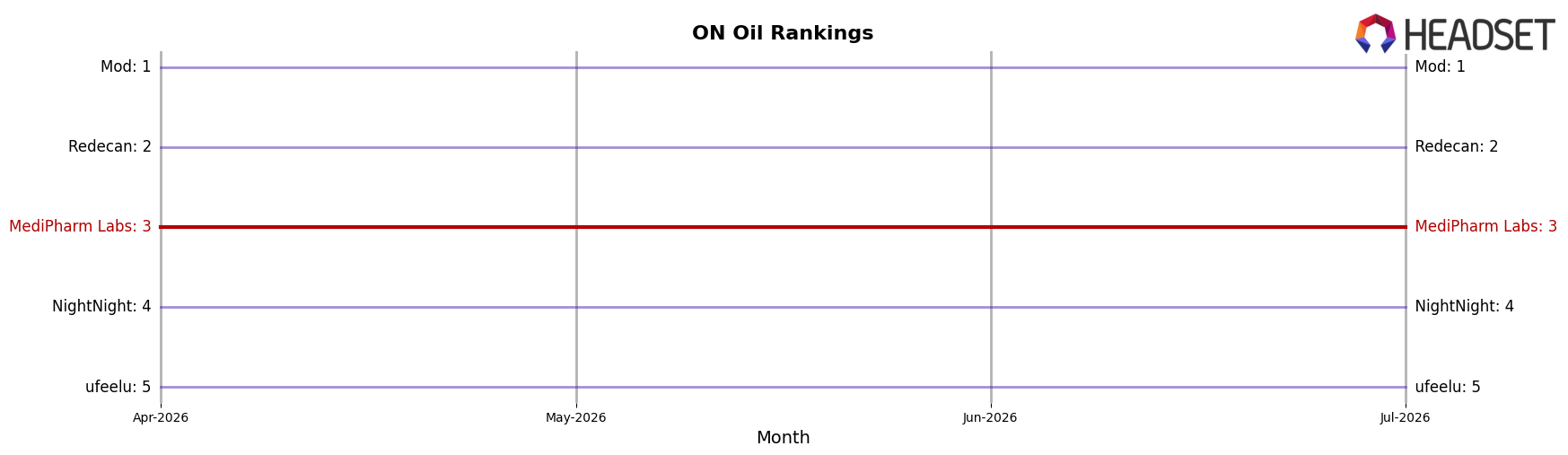

MediPharm Labs sits at rank #3 in ON Oil in July 2026, unchanged from #3 year over year, and steady versus three months ago at #3, while its peak of #2 in December 2024 marks a one-spot decline from that high; meanwhile, Mod climbed from #2 to #1 with a 11.5% year-over-year sales increase, and Redecan slid from #1 to #2 with a -26.8% year-over-year sales change, indicating MediPharm Labs is boxed between an advancing leader and a retreating rival. With NightNight holding #4 year over year and still #4 with 12.4% growth, and ufeelu improving from #6 to #5 on 15.5% growth, the pressure from below is rising even as the gap to the top narrows due to Redecan’s decline; this rank trajectory implies a stable floor at #3 but a contested path upward that favors timely share capture rather than price-led volume alone.

Notable Products

CBN:THC 1:2 Nighttime Formula Oil (30ml) posted a -89.3% month-over-month drop while holding rank 1, outpacing the next steep slides of -37.6% at rank 8 and -29.1% at rank 4, which indicates a sharp compression at the very top of the lineup despite the anchor position. THC 30 Regular Formula Oil (30ml) at rank 2 declined -5.4% versus THC Dissolving Drops Oil (30ml) at rank 3 rising 19.7%, and Oils account for 9 of the top 10 SKUs, implying July 2026 demand consolidated into a few stalwart formats while sleep- and ratio-focused variants lost momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.