Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

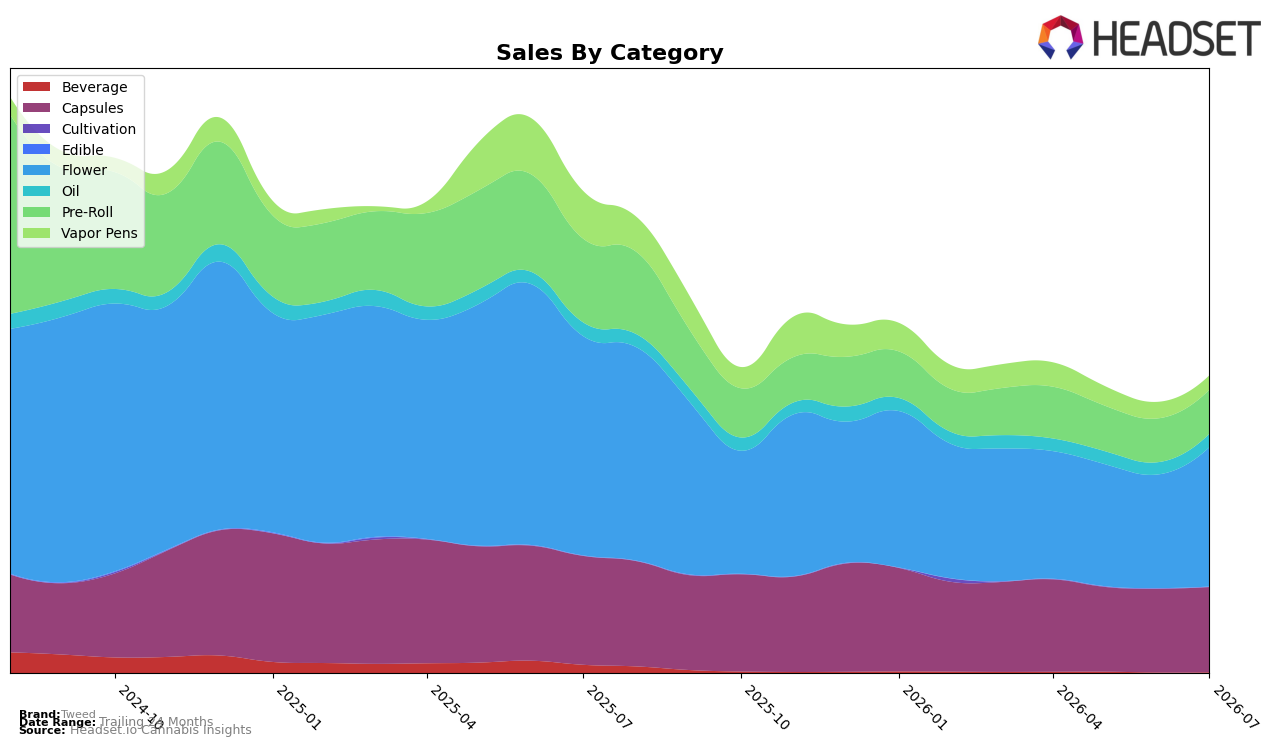

Tweed’s category mix in July 2026 concentrated 47.03% of sales in Flower with a 22.68% month-over-month increase but a 36.48% year-over-year decline, while Capsules held 28.71% share with modest 1.84% MoM growth and a 21.82% YoY drop; this split coincides with a 22.73% YoY rise in average price to $44.96 and an overall brand sales contraction of 38.40% YoY. Pre-Roll at 14.82% share inched up 0.72% MoM but fell 47.45% YoY, and Vapor Pens at 4.76% share declined 13.70% MoM and 70.39% YoY; Oil at 4.46% share grew 9.86% MoM with a relatively mild 2.21% YoY decrease, while Beverage is a 0.22% niche with 35.62% MoM growth after a 91.88% YoY collapse. The pattern implies Tweed is leaning back into higher-ticket inhalables — particularly Flower’s MoM rebound — to offset steep YoY attrition in discretionary formats, while Capsules and Oil function as steadier volume anchors that limit further erosion.

Positioning-wise, a 21st rank in Flower in British Columbia alongside a 22.68% Flower MoM lift and a 47.45% YoY drop in Pre-Roll suggests Tweed is more competitive where consumers trade up within inhalables than where they seek lower-price convenience. The 70.39% YoY slide in Vapor Pens versus a 9.86% MoM gain in Oil, combined with a 22.73% YoY increase in average price, indicates a shift toward formats that support premiumized price points without volatility, implying Tweed’s near-term positioning favors price-led recovery in core Flower while de-emphasizing peripheral categories that dilute margin and rank progress.

Competitive Landscape

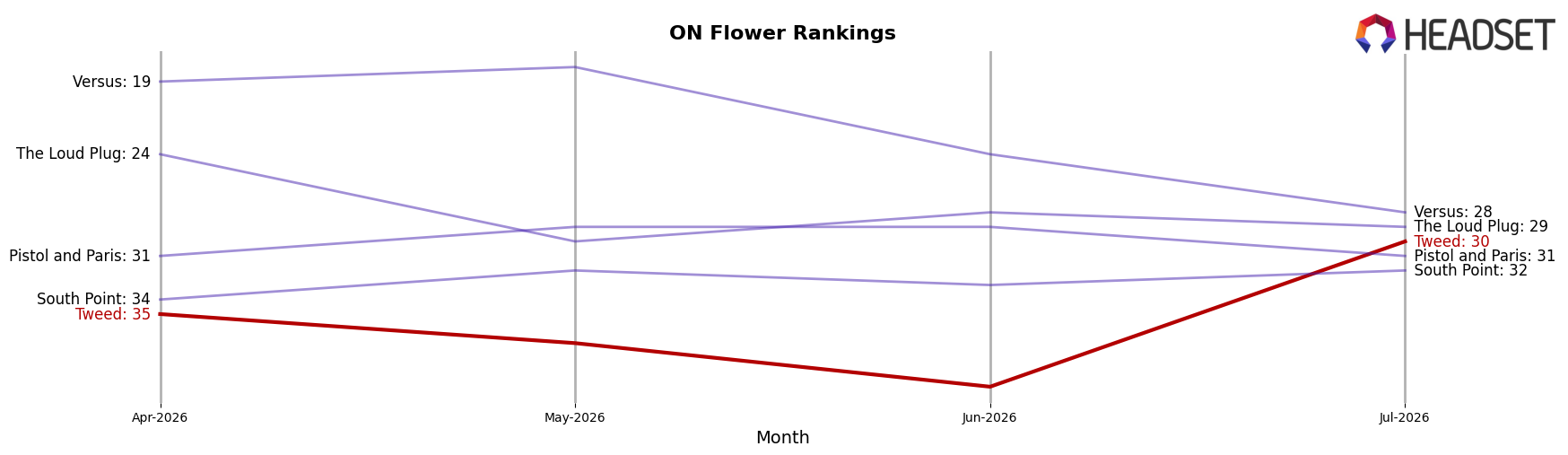

Tweed ranks #30 in ON Flower in July 2026, down 11 positions year over year from #19, while improving 5 spots versus April 2026 when it sat at #35; against its historical peak of #15 in October 2024, the current placement is 15 ranks lower. In the same period, Shred moved up to #1 from #2 year over year with sales up 17.23%, and Spinach advanced to #2 from #4 with 31.07% sales growth, indicating category leaders are consolidating share as Tweed slips. The pattern implies Tweed’s downward rank trajectory and widening gap from its October 2024 peak require either assortment repositioning or promo intensity to counter leaders’ upward momentum.

Notable Products

Blood Orange Kush (28g) posted the largest movement in July 2026 with a 71.6% month-over-month increase, jumping into rank 4, while Chemsicle (14g) fell 12.9% MoM to rank 10. Quickies - Chemsicle Pre-Roll 10-Pack (3.5g) gained 9.5% MoM to hold rank 1, and two Pre-Roll SKUs sit in the top three even as Capsules occupy three of ranks 2, 7, and 8 with mixed MoM trends from -6.3% to +9.7%. With Flower anchoring two of the top five and Pre-Rolls leading at rank 1 and rank 3, the mix tilts toward inhalables over ingestibles, implying Tweed is concentrating assortment and pricing to drive higher-velocity inhalable formats over Capsules.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.