Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

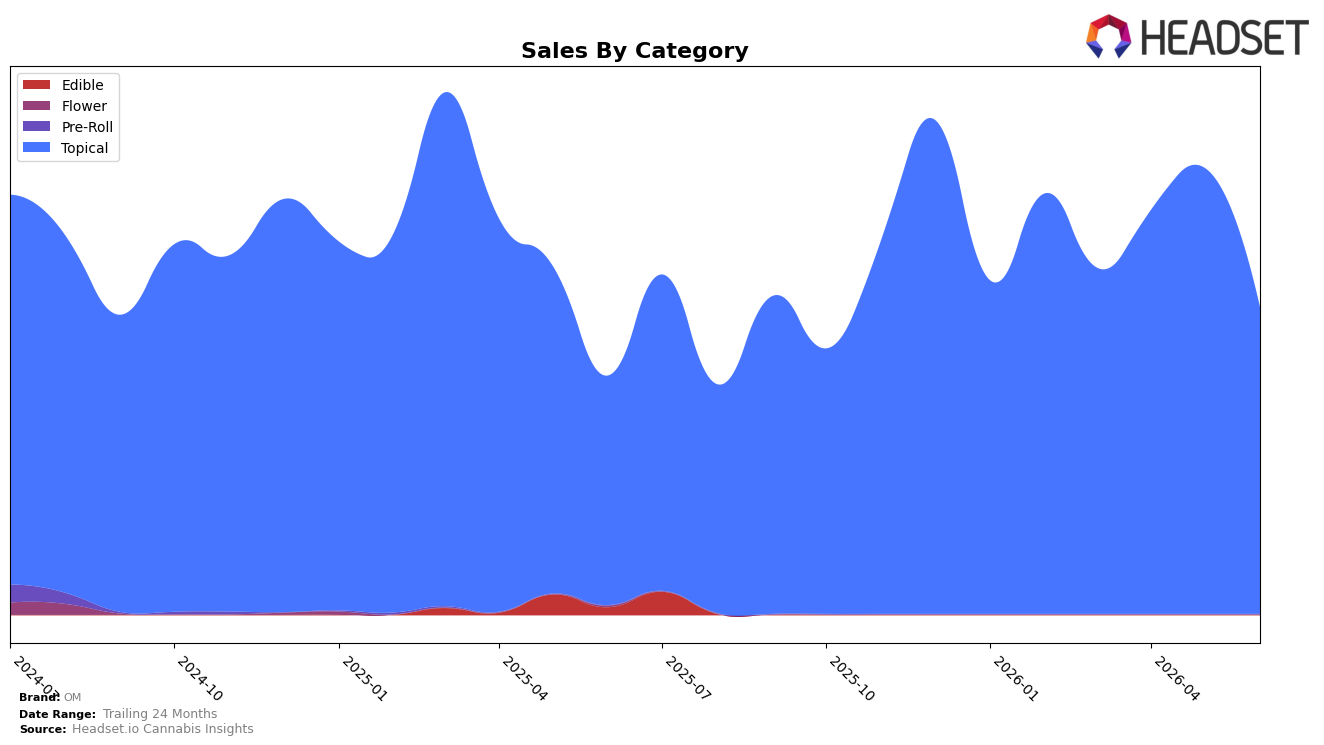

OM’s category mix in June 2026 is concentrated entirely in Topical, with 100.0% share, up 33.8% year over year but down 31.2% month over month; paired with a 0.48% YoY increase in average price and a brand-level sales lift of 28.8% YoY, the mix indicates volume-led YoY gains alongside a sharp MoM pullback. With Topical as the sole contributor, the brand’s rank at 10 in California Topical and the 24‑month sales change of −35.5% set a context where category concentration magnifies month-to-month volatility; the pattern implies OM is trading short-term stability for focused scale in a single category.

The divergence between a 33.8% YoY Topical surge and a 31.2% MoM contraction, alongside a 0.48% YoY price move and an June 2026 rank of 10 in California Topical, implies that OM’s positioning leans on episodic demand or promotional cadence rather than broad-based multi-category insulation. Given 100.0% category concentration and a −35.5% change over 24 months, the mix suggests that sustaining rank will depend on smoothing month-level swings within Topical or selectively diversifying to reduce exposure; the pattern implies OM’s current stance prioritizes depth in Topical over hedging across categories.

Competitive Landscape

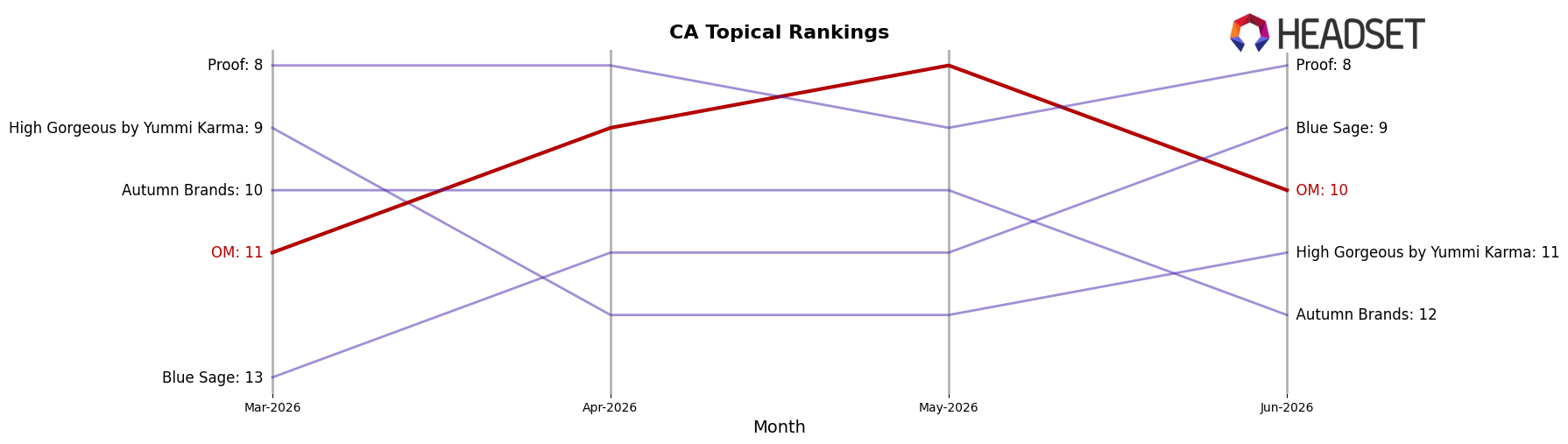

OM sits at #10 in CA Topical in June 2026, improving 4 ranks YoY from #14 while slipping 1 place from #11 three months ago; the brand’s peak at #8 in May 2026 indicates recent momentum that has partially cooled. Competitive dynamics amplify the mixed signal: Buddies held #3 with a 64.5% YoY sales increase as OM moved from #14 to #10, and Liquid Flower rose from #6 to #4 with 58.7% YoY growth, outpacing OM’s rank gains even as category leaders like Papa & Barkley stayed at #1 with a -4.6% YoY decline. This trajectory implies OM is gaining share positioning against weakening incumbents but risks being boxed out of upper tiers by faster-rising challengers unless recent rank improvements convert into sustained advances beyond #8.

Notable Products

Just Peachy Rosin Bath Bomb (100mg) posted the steepest movement in June 2026 with a -49.7% month-over-month drop and slid to rank 2, while Fragrance Free Extra Strength Bath Bomb (1000mg) fell -63.5% and sat at rank 7. In contrast, CBN/THC 1:10 Sweet Dreams Bath Bomb (100mg THC, 10mg CBN) rose 45.6% MoM at rank 5, and CBD/THC 1:1 Recovery Epsom Bath Salts (25mg CBD, 25mg THC, 6.5oz) gained 19.5% at a tied rank 1, indicating mixed momentum within bath formats. With bath bombs and Epsom salts occupying all top-7 slots and CBD/THC 1:1 salts spanning ranks 1 and 3 despite a -22.1% decline for CBD/THC 1:1 Arnica Pain Relief Epsom Bath Salts (25mg CBD, 25mg THC), concentration remains in bathing therapeutics rather than creams or roll-ons. This pattern implies OM is leaning further into bath-centric SKUs where volatility is high but the category still anchors the lineup, suggesting assortment discipline around fewer, higher-velocity bath formats over broader topical diversification.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.