Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Pine + Star is stocked at 187 licensed dispensaries across Massachusetts and Maine, 126 of them in Massachusetts, with the deepest coverage in Boston, Springfield, Worcester, Dracut, and Fall River. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

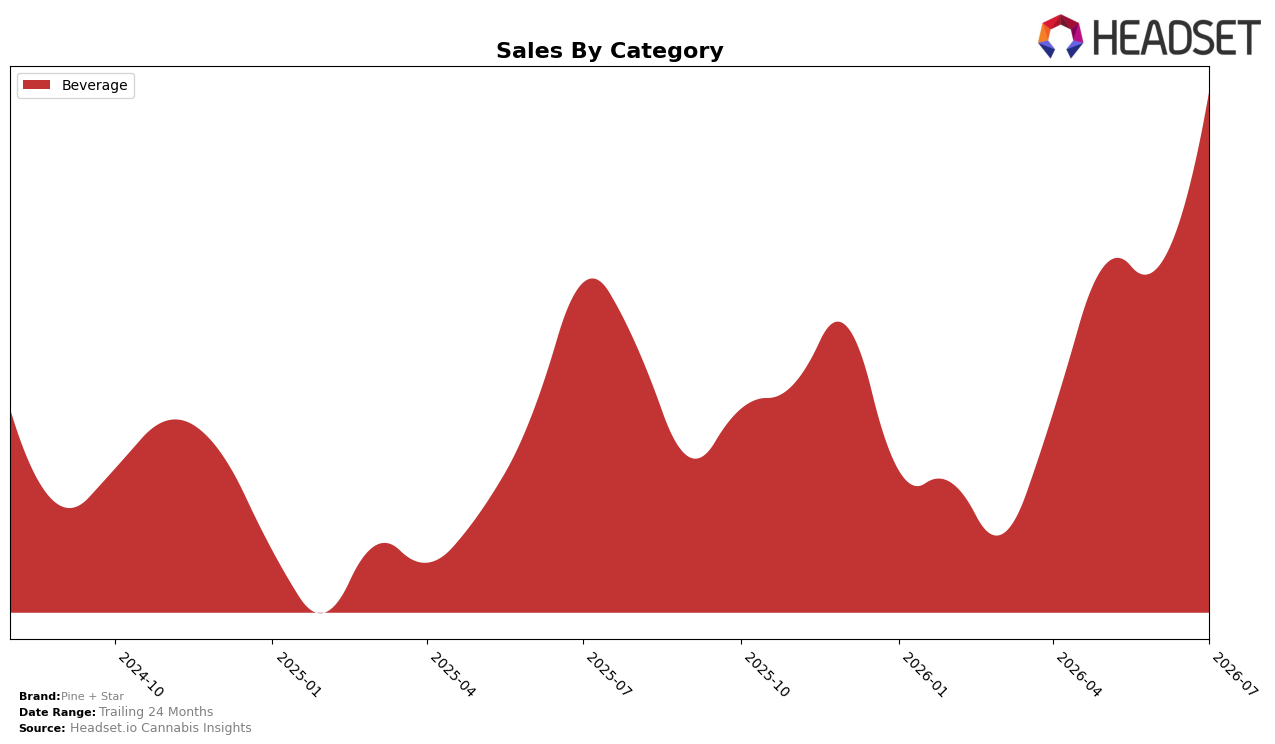

In July 2026, Pine + Star operated as a single-category brand with Beverage at 100.0% mix, up 26.6% year over year and 24.0% month over month, while the brand’s average price declined 1.5% YoY and the statewide Beverage rank in Massachusetts sat at rank 4. The combination of double-digit volume-led gains (26.6% YoY sales growth alongside a 1.5% YoY price dip) and a 24.0% MoM acceleration implies Pine + Star’s July 2026 growth skewed toward unit expansion within Beverage rather than price-driven gains, concentrating performance where the brand is already most visible at rank 4.

These shifts indicate Pine + Star is leaning into a value-accessible Beverage stance: a 1.5% YoY price decrease paired with 26.6% YoY and 24.0% MoM sales growth suggests elasticity is favorable at current price tiers, and the 100.0% category focus amplifies that response. Holding rank 4 in Massachusetts while expanding faster than prices contract positions the brand to convert share via velocity rather than premiumization, implying the near-term path to differentiation is deeper penetration within Beverage rather than category diversification in July 2026.

Competitive Landscape

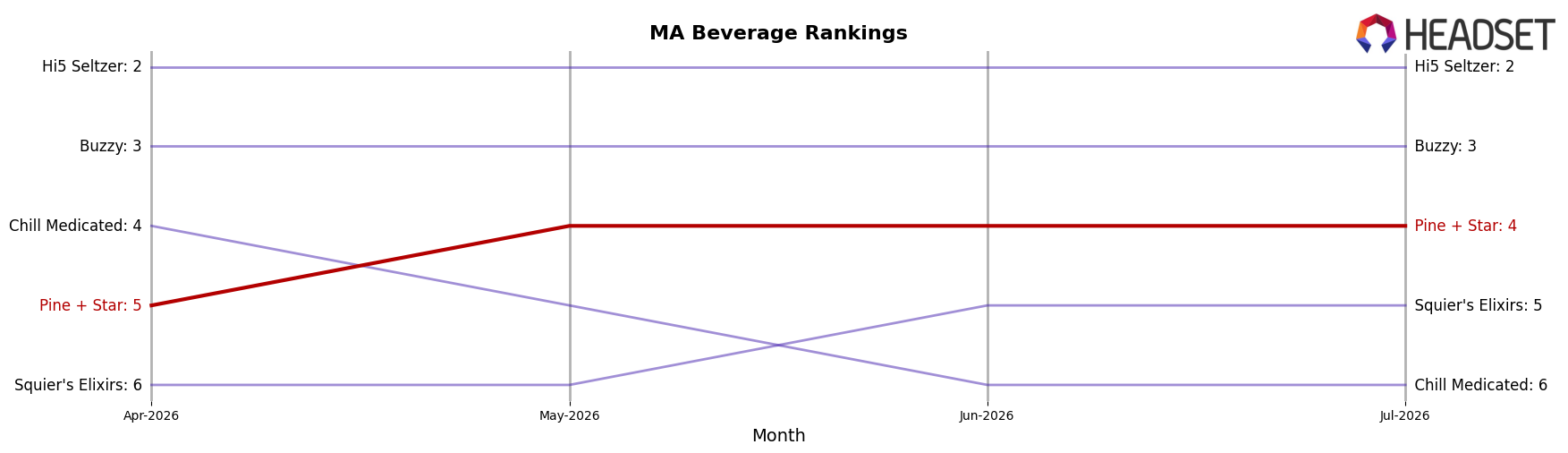

Pine + Star sits at #4 in MA Beverage in July 2026, up 1 rank from #5 year over year and up 1 rank from #5 three months ago, reaching a peak rank of #4 in July 2026 while the #1 spot remains held by Levia which stayed flat at #1 as its sales grew 37.16% YoY, and Hi5 Seltzer held #2 with 38.24% YoY sales growth as Buzzy maintained #3 and Squier's Elixirs improved from #6 to #5; with Pine + Star’s rank improvement of 1 spot contrasted against Squier's Elixirs gaining 1 rank and the top three remaining unchanged, the pattern implies Pine + Star is consolidating a mid-tier position but must displace a stable #3 to advance further.

Notable Products

Classic Grapefruit Sparking Beverage (5mg THC, 12oz) posted the single biggest month-over-month surge at +53.98% to rank 7, while Sparkling Tea Lemonade (5mg THC, 355ml, 12oz) plunged -78.40% to rank 10, indicating a sharp bifurcation in tail SKUs. Blueberry Lemonade Sparkling Beverage (5mg THC, 355ml, 12oz) held rank 1 with +13.23% MoM as Cape Code Cranberry Sparkling Beverage (5mg THC, 355ml, 12oz) climbed +44.14% to rank 2, and five of the top seven gained at least +16% MoM. With all top-10 entries in Beverage and the leading trio sitting at ranks 1–3, the mix points to Pine + Star leaning into flavor-led sparkling formats where upside is concentrated while underperforming variants face quick displacement.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.