Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

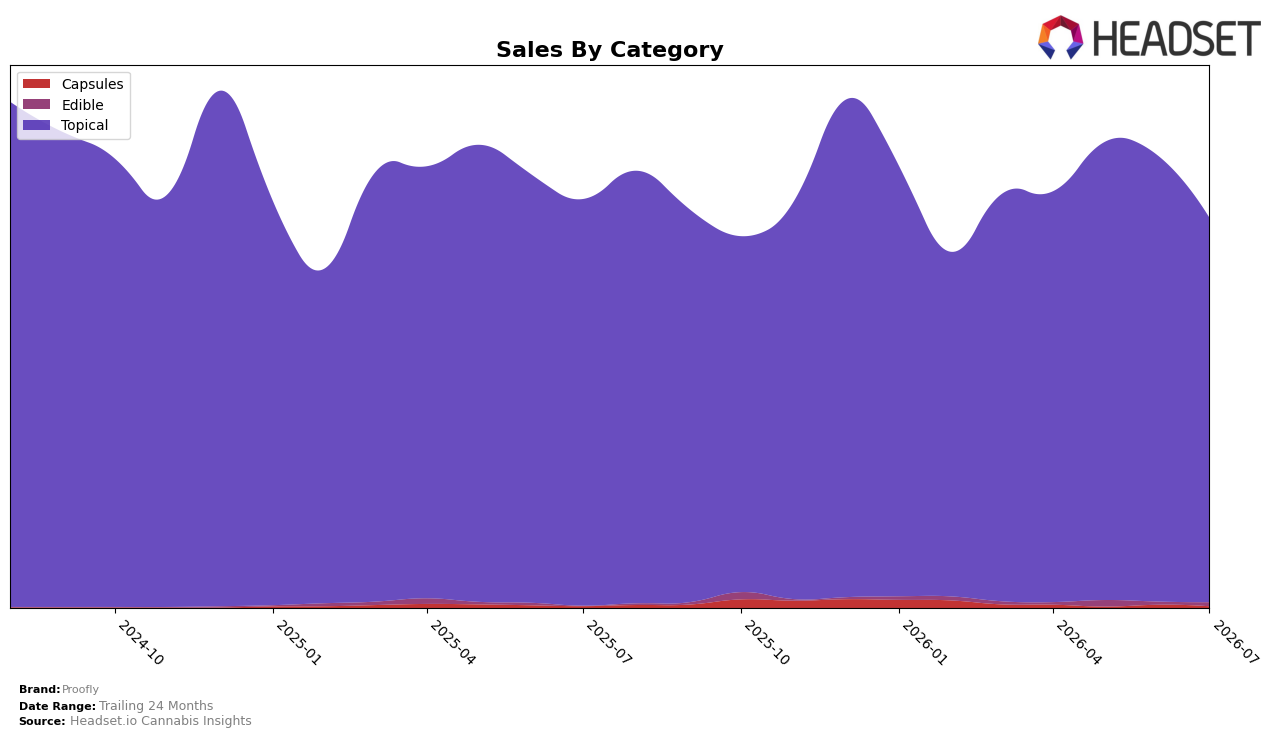

In July 2026, Proofly’s mix was overwhelmingly concentrated in Topical at 98.77% share, with Topical sales down 5.46% year over year and 13.80% month over month, while the much smaller Edible segment held 0.92% share with a 31.08% month-over-month lift and Capsules at 0.32% share fell 54.78% month over month and 6.32% year over year. Despite an overall brand sales decline of 4.59% year over year and a 3.14% increase in average price, the category footprint remains anchored to a single segment, and the combination of Topical’s double-digit month-over-month decline alongside Edible’s month-over-month uptick implies a nascent diversification that is not yet material to total revenue.

Proofly’s number 1 rank in Topical within British Columbia juxtaposed with a 13.80% month-over-month contraction in Topical share of sales suggests the brand’s leadership is concentrated but vulnerable to volume swings in one category. Given a 20.71% two-year brand sales decline and a portfolio where 98.77% of sales move in lockstep with Topical trends, the small but growing 0.92% Edible slice provides optionality; the pattern implies that even a modest reallocation toward categories with positive month-over-month momentum could reduce volatility without undermining the price architecture established in Topical.

Competitive Landscape

Proofly holds #1 in ON Topical in July 2026, unchanged from #1 a year earlier, and has stayed #1 over the latest three months, while competitor Wildflower Canada sits at #2 after improving from #3 year over year as its sales rose 48.4%, and Stewart Farms slipped to #3 from #2 with a 27.4% sales decline; further down, ufeelu moved up to #4 from #5 with 14.2% sales growth while Nutra fell to #5 from #4 with sales down 16.8%, indicating Proofly’s flat YoY rank at #1 amidst upward pressure from a faster-rising #2 suggests leadership is currently stable but faces tightening gap dynamics if competitor momentum persists.

Notable Products

CBD/THC 1:1 Balanced Muscle Cream (250mg CBD, 250mg THC,100ml) fell 39.7% month over month to rank 4 in July 2026, while CBD/THC Extra Strength Relief Cooling Gel (2000mg CBD, 100mg THC, 100g) declined 15.5% yet held rank 1. CBD Extra Strength Isolate Relief Muscle Joint Balm (2000mg CBD, 100g) slipped 8.0% at rank 3, and the 1:1 Extra Strength Muscle Balanced Cream dropped 29.9% at rank 6. With all top-10 SKUs concentrated in Topicals and multiple high-THC or balanced formulas losing double digits, the mix signals a shift toward defending flagship cooling and isolate formats rather than expanding balanced or novelty variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.