Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

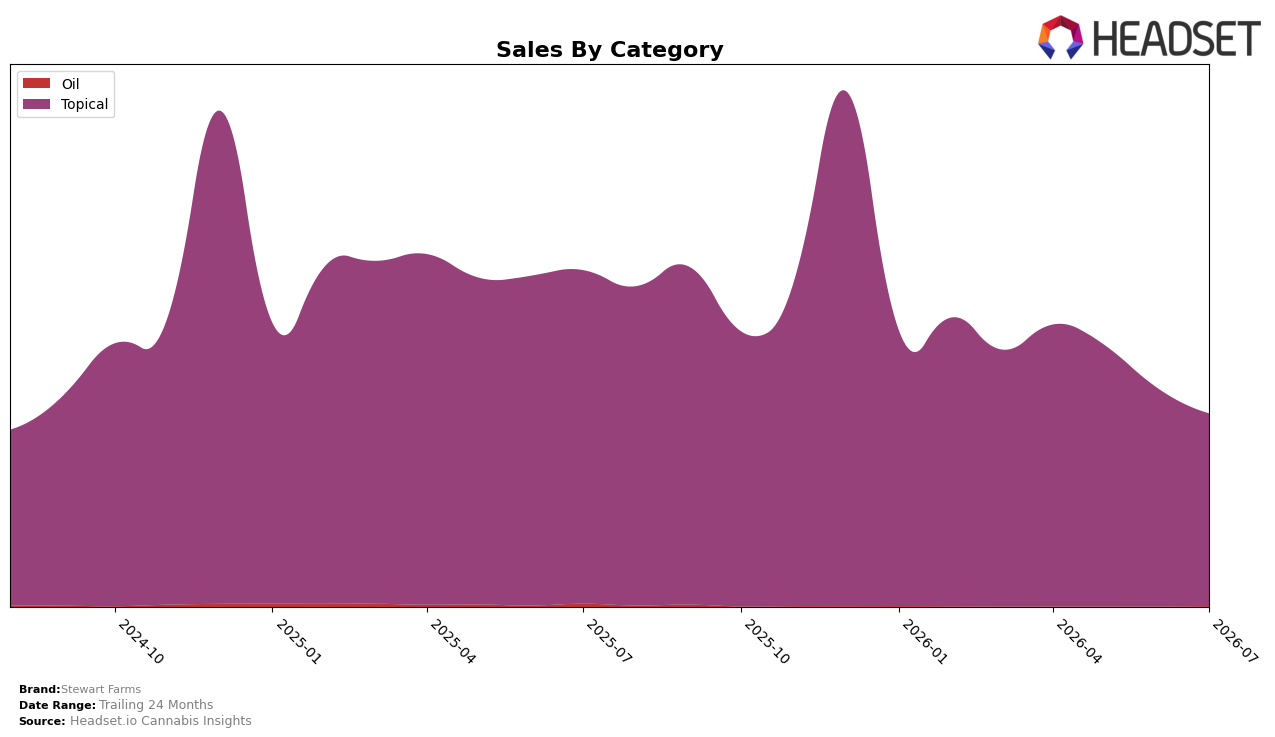

In July 2026, Stewart Farms remained concentrated in Topical with a 99.77% category share while Oil accounted for 0.23%, signaling an even tighter mix than prior periods; within that mix, Topical declined 42.29% year over year and 11.76% month over month, and Oil fell 84.09% year over year with no measurable month-over-month recovery. The brand’s average price declined 14.14% year over year to $28.92, while the leading market footprint was in ON, and within the Topical category the brand held rank 3 in Alberta. The pattern implies Stewart Farms is doubling down on a single-category identity while absorbing traffic and pricing pressure that reduced both Topical volume and the already small Oil presence.

The contraction in Oil to a 0.23% share alongside a 42.29% Topical drop and an 11.76% month-over-month slide concentrates risk but also clarifies positioning around Topical leadership, as evidenced by a rank of 3 in Alberta and a 99.77% mix. With average price down 14.14% year over year and Topical volume still negative month over month, the brand’s near-term positioning leans on defending Topical rank rather than rebuilding a multi-category portfolio; this suggests a strategy to convert price elasticity and provincial exposure in ON into sustained share while accepting limited relevance in Oil.

Competitive Landscape

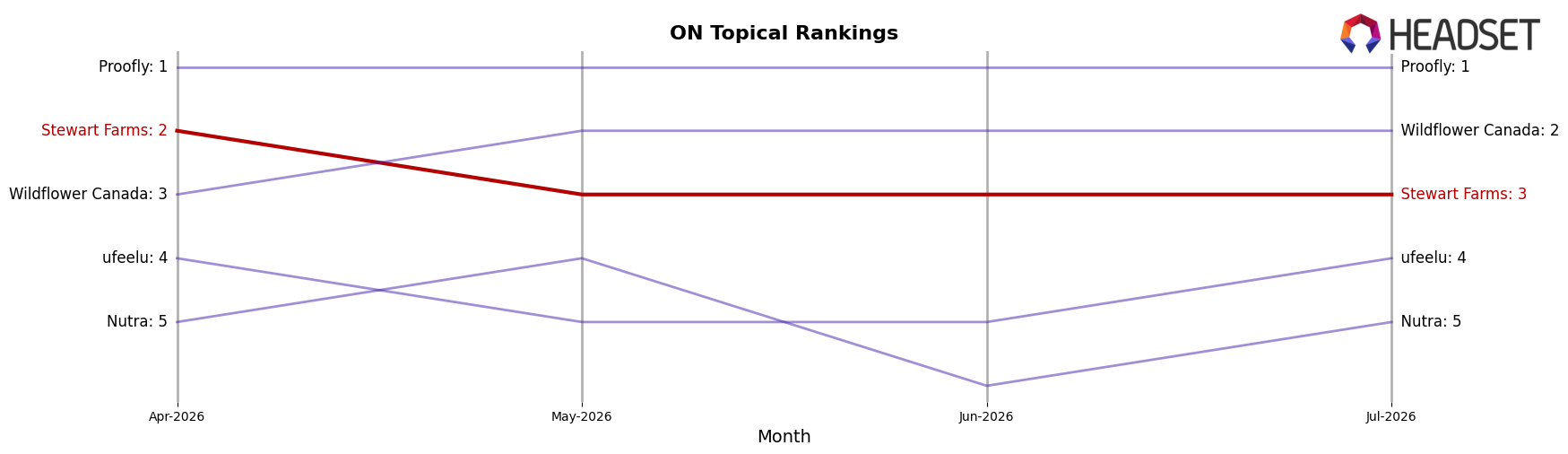

Stewart Farms ranks #3 in ON Topical in July 2026, down 1 position year over year from #2, after peaking at #2 in April 2026 but slipping from #2 three months ago to #3 now; this contrasts with Wildflower Canada, which rose from #3 to #2 while posting a 48.38% year-over-year sales increase, and Proofly, which held #1 despite a 1.99% year-over-year sales decline. Meanwhile ufeelu moved up from #5 to #4 with 14.16% growth as Nutra slipped from #4 to #5 with a 16.82% decline, indicating Stewart Farms is getting bracketed by faster risers above and below; the trajectory from #2 in April 2026 to #3 in July 2026 implies share defense is needed as mid-tier climbers compress its position.

Notable Products

Rebound - CBD Ultimate Strength Arctic Heat Cooling Cream (5000mg CBD, 120g) posted the steepest movement in July 2026 with a -25.4% month-over-month slide while holding rank 4, and Rebound - CBD/THC 1:1 Arctic Heat Muscle Cream (500mg CBD, 500mg THC, 120g) dropped -17.1% at rank 2, signaling pressure on higher-priced or higher-milligram therapeutics. CBD/THC 1:1 Blue Dream Bath Bomb (50mg CBD, 50mg THC, 130g) eased -6.4% but stayed at rank 1, while Rebound- CBD/THC 1:1 Arctic Heat Extra Strength Relief Stick (300mg CBD, 300mg THC, 30g) rose +24.0% at rank 7, indicating share is rotating from premium creams toward portable relief formats. Eight of the top ten SKUs are Topical bath bombs and creams, and the CBD:THC 1:1 bath bomb family anchors the leaderboard across ranks 1, 3, and 9, implying the franchise still pulls traffic even as individual SKUs retrench -18.9% to -0.1% month over month. The pattern implies Stewart Farms is migrating demand from heavyweight therapeutic creams toward accessible 1:1 bath and stick formats, pointing to a near-term focus on breadth and frequency over high-ticket depth, despite one cream still generating $49,946.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.