Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

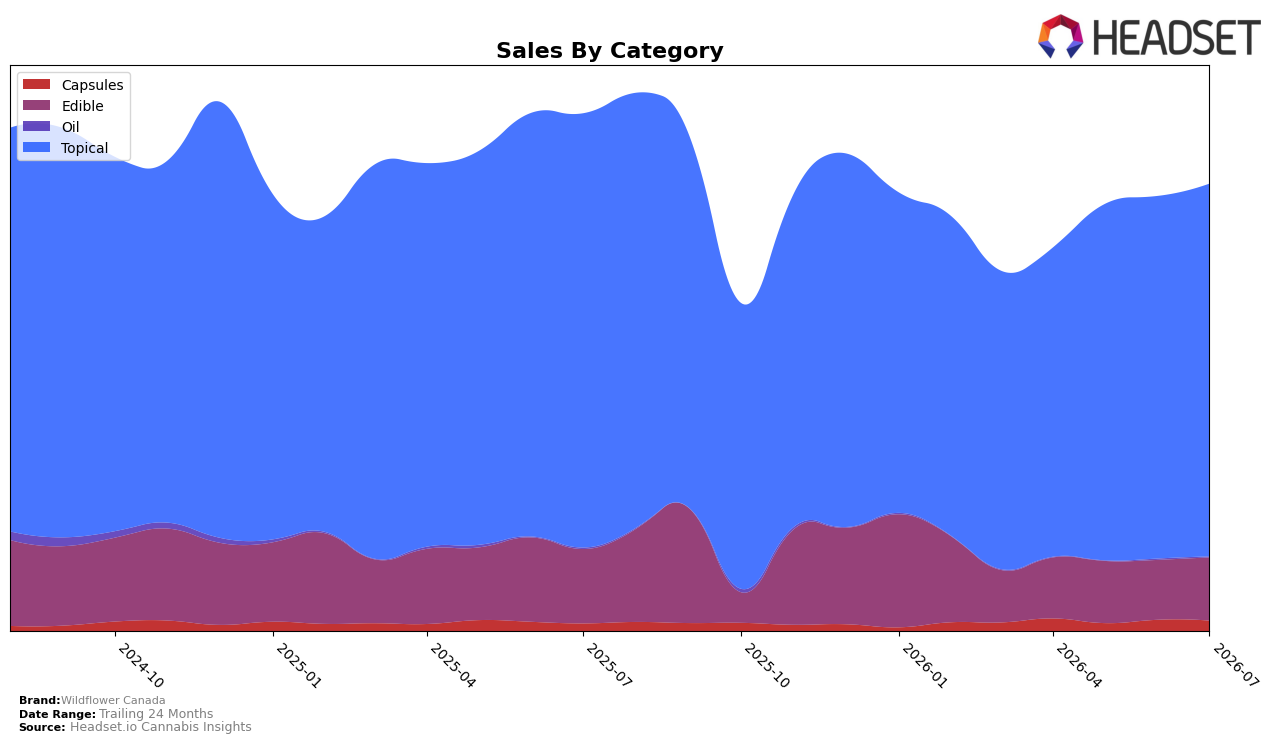

Wildflower Canada remained concentrated in Topical at 83.44% share in July 2026, with Topical sales down 14.16% year over year but up 2.80% month over month; Edible held 14.11% share with sales down 15.04% year over year yet up 5.60% month over month. Capsules were 2.27% of mix with sales up 37.55% year over year but down 7.87% month over month, while Oil slid to 0.17% share with sales down 41.31% year over year and down 33.34% month over month. Despite brand-level sales down 13.61% year over year and an average price decline of 2.77% year over year, the mix skews toward a higher-priced Topical average at $53.67 relative to Edible at $10.29, implying margin defense via category composition even as volume softens.

With Topical ranked 1 in Alberta and holding 83.44% of sales, the brand’s position leans on category leadership while Edible’s 5.60% month-over-month lift and Capsules’ 37.55% year-over-year growth indicate selective diversification paths. The simultaneous month-over-month gain in Topical at 2.80% and contraction in Capsules at 7.87%, paired with Oil’s 33.34% month-over-month decline, suggests prioritizing scale categories that can absorb price cuts while maintaining rank, reinforcing a strategy centered on Topical dominance with measured Edible expansion as the practical hedge.

Competitive Landscape

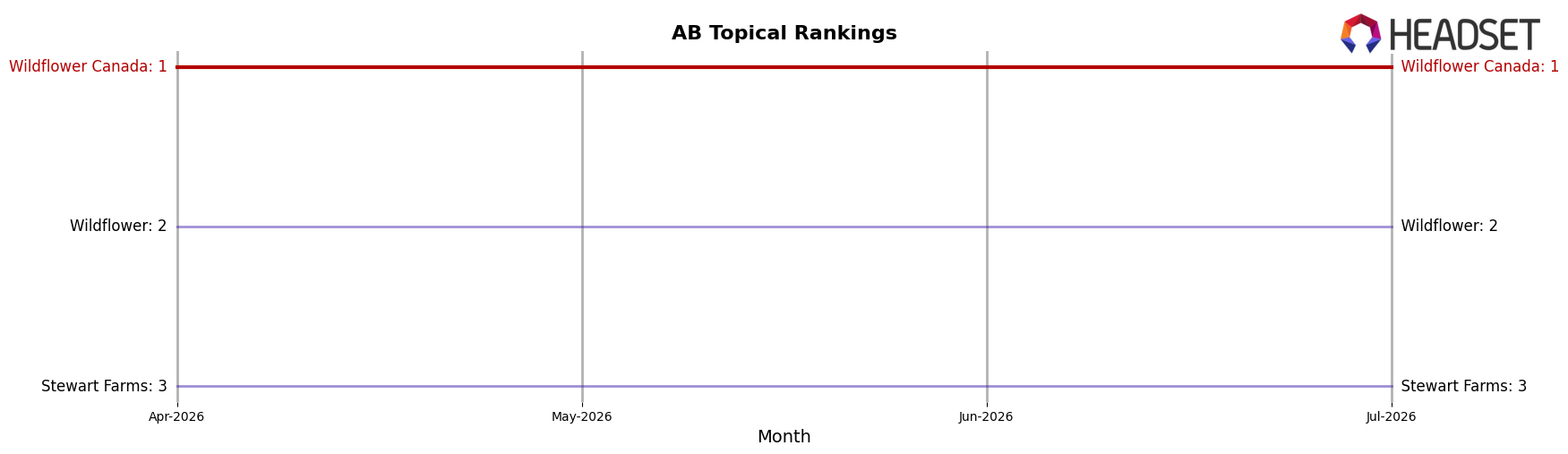

Wildflower Canada sits at rank #1 in AB Topical in July 2026, unchanged from #1 a year earlier, and it also held #1 three months ago, indicating zero rank volatility while the category around it shuffled by multiple positions. In contrast, Wildflower climbed from #5 to #2 with a 288.6% year-over-year sales increase, while Stewart Farms slipped from #2 to #3 on a 59.0% sales decline, and Proofly fell from #3 to #4 with a 41.5% drop; meanwhile, Solei moved from #4 to #5 while sales contracted 30.9%. This stability at #1 amid a competitor surging 3 ranks and others declining 1 rank implies Wildflower Canada’s current leadership is resilient to both rapid share gains from below and retrenchment among mid-pack rivals.

Notable Products

The steepest decline came from CBD Relief Stick (500mg CBD), down 75.8% month over month and sliding to rank 8, which contrasts with CBD Relief Stick (205mg CBD) falling 17.7% to rank 3 and indicates demand is consolidating away from mid-strength formats. CBD Extra Strength Relief Stick (1000mg CBD, 60g) in rank 1 grew 4.1% MoM and captured the only six-figure result at $284,437, while Sweet Dreams - CBD/CBN/THC 10:10:2 Goji Berry Gummies 5-Pack (50mg CBD,50mg CBN,10mg THC) rose 5.6% at rank 2, signaling that the top two positions are anchored by either very high-dose topical relief or sleep-oriented edibles. With four of the top ten being Topical SKUs and only one Capsule in rank 4 declining 7.9%, the mix points to concentration around topical relief with selective traction in sleep-support formats rather than broad portfolio lift.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.