Mar-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

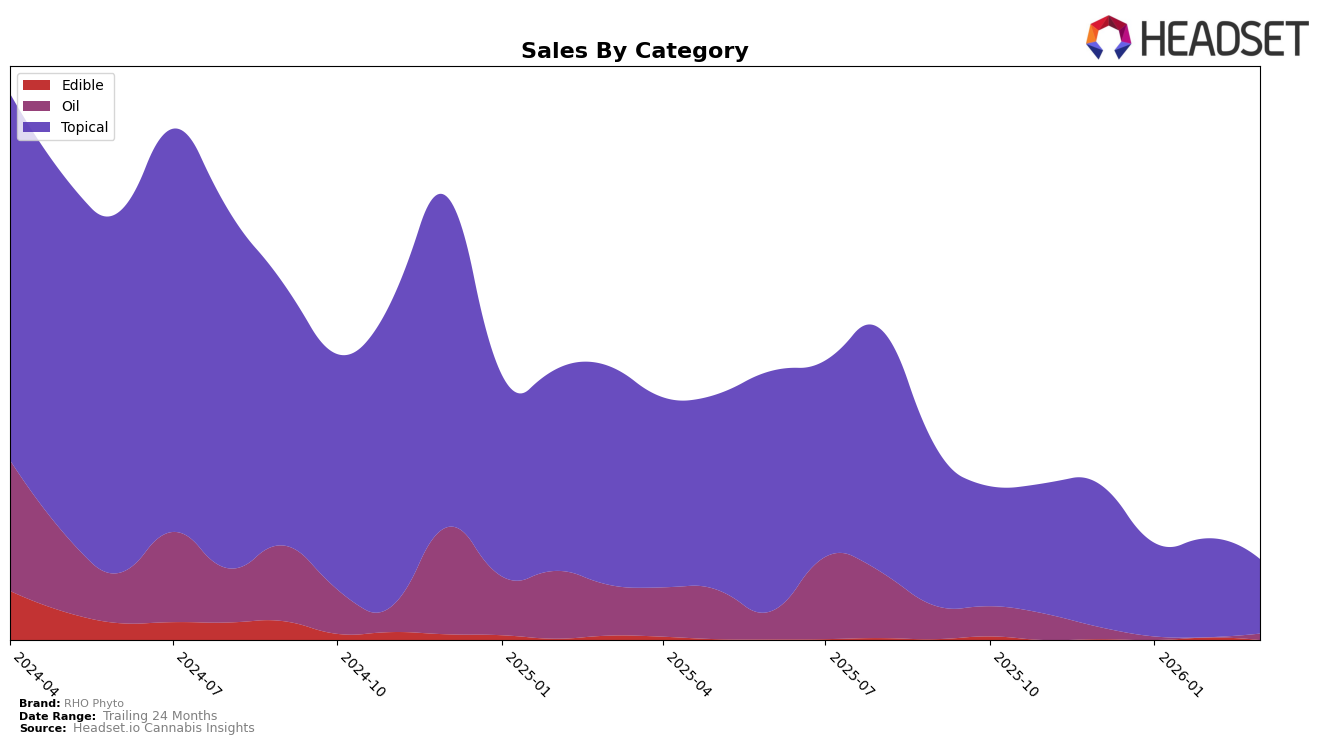

Market Insights Snapshot

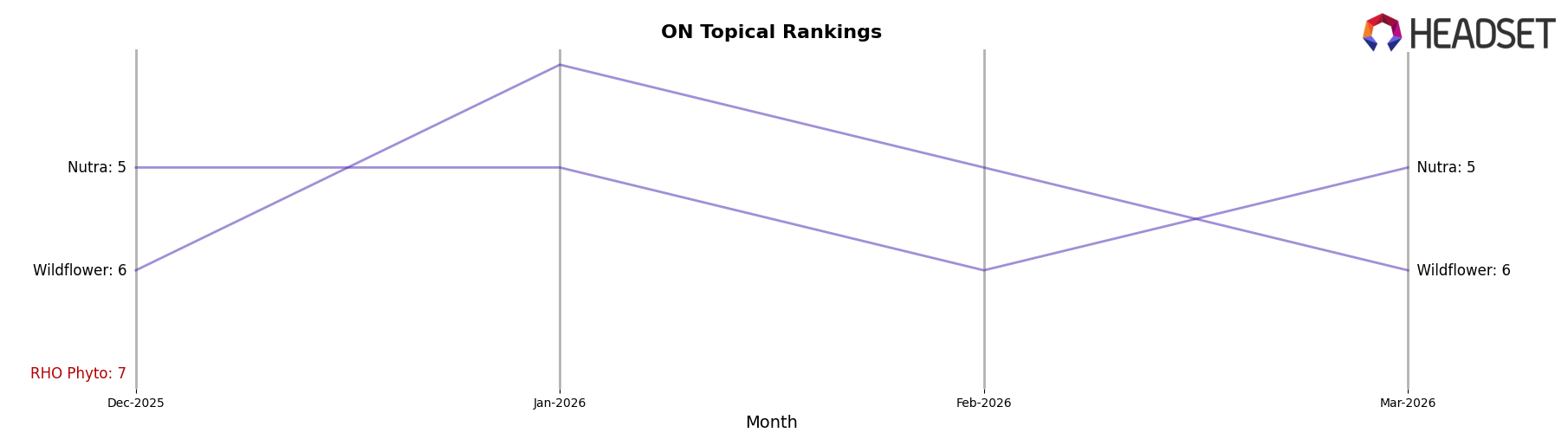

In the Ontario market, RHO Phyto has shown a notable presence in the Topical category. As of December 2025, the brand was ranked 7th, indicating a strong foothold in this niche. However, in the subsequent months of January, February, and March 2026, RHO Phyto did not appear in the top 30 brands. This absence suggests a decline in their market position, which could be attributed to increased competition or shifts in consumer preferences within the Topical category. Despite this, the brand's initial ranking shows that there was a significant interest in their products at the end of 2025.

While RHO Phyto's performance in Ontario's Topical category provides some insights, it is crucial to consider the broader implications of their absence from the top rankings in the following months. This decline might reflect challenges in maintaining market share or adapting to evolving market trends. The brand's strategy moving forward will likely need to address these competitive pressures to regain its standing. The data suggests that while RHO Phyto has potential, consistent performance across months is essential for long-term success.

Competitive Landscape

In the Ontario topical cannabis market, RHO Phyto experienced a notable decline in its competitive standing from December 2025 to March 2026. Initially ranked 7th in December 2025, RHO Phyto did not maintain a presence in the top 20 brands in the subsequent months, indicating a significant drop in market visibility and potential sales. In contrast, competitors such as Wildflower and Nutra consistently ranked within the top 6, with Wildflower reaching as high as 4th place in January 2026. This suggests that while RHO Phyto struggled to maintain its market position, its competitors were able to capture and sustain consumer interest, potentially impacting RHO Phyto's sales trajectory negatively. The data highlights the importance for RHO Phyto to reassess its market strategies to regain competitive ground in the Ontario topical category.

Notable Products

In March 2026, the top-performing product from RHO Phyto was the CBD/THC 25:1 Deep Tissue Extra Strength Gel in the Topical category, maintaining its first-place rank consistently from December 2025 with March sales at 189 units. The THC:CBG Rapid Act Oral Spray in the Oil category climbed back to second place, showing a significant improvement from its unranked status in February 2026. The CBG Transdermal Relief Gel also in the Topical category held steady in third place, despite a decrease in sales to 8 units. The CBD:THC 10:1 Daily Dose Gummies in the Edible category, which was ranked fourth in December 2025 and second in February 2026, was not ranked in March. Overall, while the rankings of the top products saw some fluctuations, the Deep Tissue Extra Strength Gel remained the consistent leader in sales.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.