Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

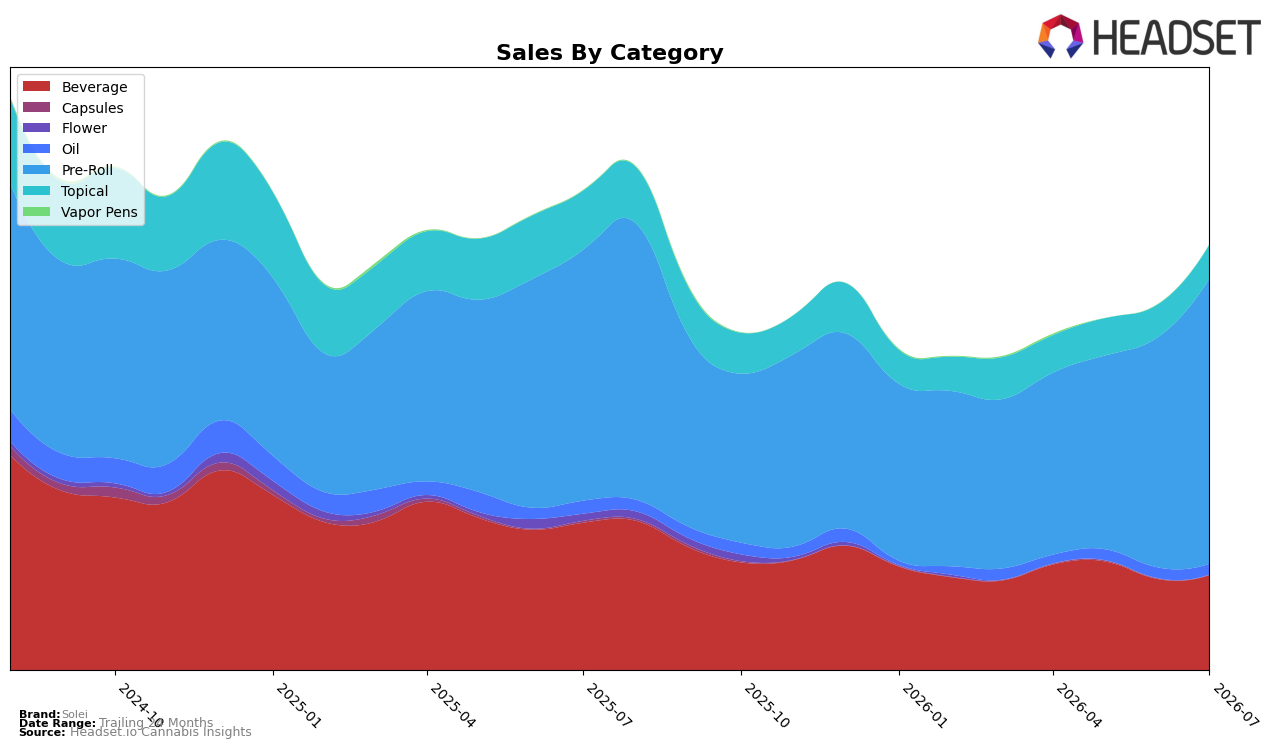

In July 2026, Solei concentrated 67.16% of sales in Pre-Roll with a year-over-year gain of 13.59% and a month-over-month jump of 23.80%, while Beverage fell 35.58% year over year despite a 4.29% month-over-month uptick. Topical contracted 42.37% year over year with a modest 4.15% month-over-month rise, and Oil declined 16.75% year over year with a 0.43% month-over-month increase; together these shifts lifted Pre-Roll’s share versus Beverage at 22.36% and Topical at 7.99%. Although overall brand sales declined 11.34% year over year, the mix tilt toward a faster-growing Pre-Roll and away from shrinking Beverage and Topical indicates a pivot toward inhalable demand concentration that can stabilize volume if July’s 23.80% Pre-Roll momentum persists.

The category reweighting—Pre-Roll up 23.80% month over month and 13.59% year over year while Beverage down 35.58% year over year—implies Solei is trading breadth for depth, leaning into a higher-price Pre-Roll average at $18.72 versus Beverage at $6.05. With Topical at 7.99% share and Oil at 2.50% share posting year-over-year declines of 42.37% and 16.75% respectively, the brand’s portfolio is concentrating into one lead format as its overall average price rose 6.83% year over year; this positioning suggests near-term share defense will depend on sustaining Pre-Roll velocity while accepting reduced reach across lower-price, slower categories.

Competitive Landscape

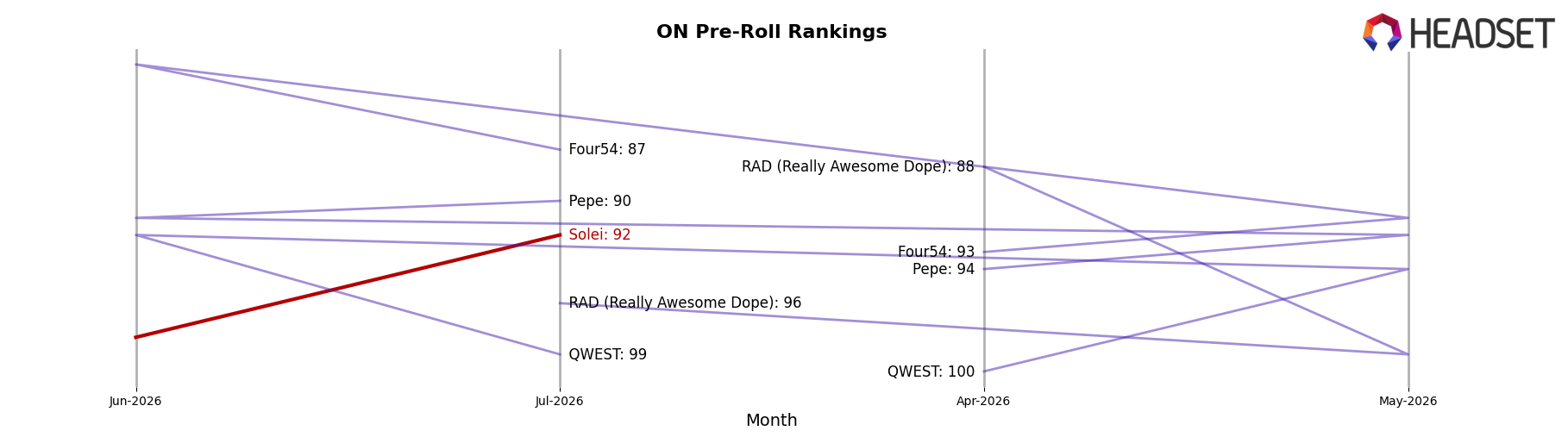

Solei is ranked #92 in ON Pre-Roll in July 2026, improving 18 positions from #110 year over year and rising 14 positions from #106 over the last three months; this marks a peak rank of #92 in July 2026, while category leaders moved in divergent directions as Back Forty / Back 40 Cannabis climbed from #2 to #1 with 67.4% YoY sales growth and General Admission slid from #1 to #2 alongside a 23.2% YoY sales decline. With Thumbs Up Brand advancing from #9 to #4 and 52.7% YoY growth while Spinach moved from #14 to #5 with 65.3% YoY growth, the mid-tier is compressing upward, implying Solei’s rank gains are timing-sensitive and will require sustained share capture to avoid slipping as faster-rising competitors pull the threshold higher.

Notable Products

Slims -Balance Pre-Roll 10-Pack (4g) posted a +50.4% month-over-month surge to rank 4 in July 2026, while the CBD/THC 2:1 Dark Cherry Sparkling Beverage (10mg CBD, 5mg THC, 355ml) fell -41.1% to rank 6, setting a split trajectory between inhalables and mixed-ratio drinks. Slims - Free Pre-Roll 10-Pack (4g) added +17.1% at rank 3 as Jean Guy Pre-Roll (1g) slid -25.4% to rank 7, and four of the top ten are Pre-Roll SKUs, indicating demand concentration in ready-to-use formats. CBD Dragonfruit Watermelon Sparkling Water (25mg CBD, 12oz, 355ml) gained +13.7% at rank 1 compared to CBD Mango Passionfruit Sparkling Soda (25mg CBD, 12oz, 355ml) at +7.2% and rank 2, with beverages led by CBD-only profiles while THC-inclusive options contract by -41.1%. The pattern implies Solei’s near-term mix is tilting toward Pre-Roll volume leadership and CBD-only beverage retention, with less traction for hybrid CBD/THC drinks, steering portfolio priority toward inhalables and non-intoxicating refreshment.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.