Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

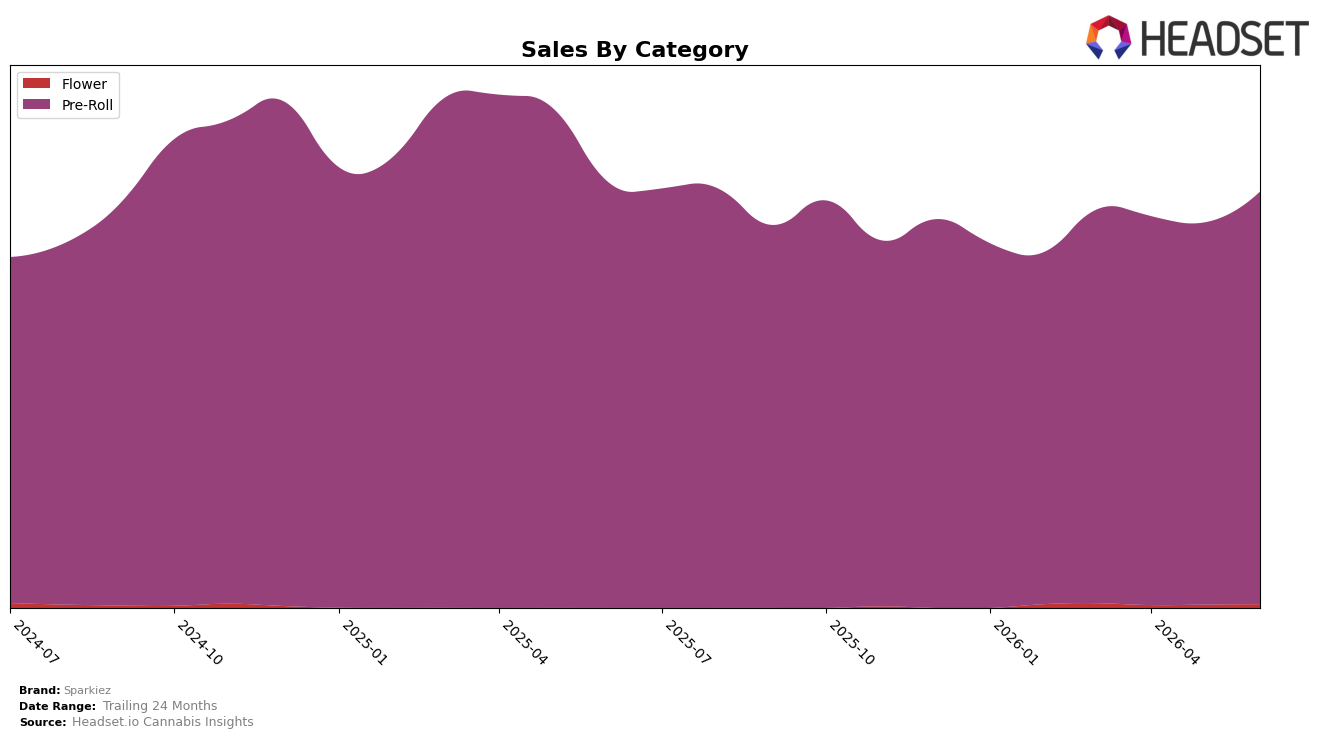

In June 2026, Sparkiez concentrated 99.09% of sales in Pre-Roll while Flower held 0.91%, with Pre-Roll up 7.93% month over month but down 3.14% year over year, and Flower up 12.47% month over month with no year-over-year baseline reported; this mix sits alongside a brand-level year-over-year sales change of -2.25% and a 24‑month gain of 18.02%. Average price rose 3.33% year over year to $16.65 while Pre-Roll pricing sat at $16.61 and Flower at $22.95, and within the Pre-Roll category Sparkiez held rank 15 in California; the pattern implies that short-term volume is rebounding on concentrated Pre-Roll strength while the slight annual decline reflects exposure to a single category that is still cycling negative versus last year.

The combination of a 7.93% month-over-month lift in a category that drives 99.09% of sales and a brand rank of 15 in California Pre-Roll indicates momentum concentrated in a crowded middle tier, while a 3.33% year-over-year price increase alongside a -3.14% Pre-Roll year-over-year trend suggests limited elasticity headroom. With Flower’s 12.47% month-over-month growth off a 0.91% share base and the brand’s -2.25% year-over-year sales change versus an 18.02% 24‑month increase, the implication is that diversification needs to scale faster than current gains to buffer category swings and support rank advancement from 15 without over-reliance on price.

Competitive Landscape

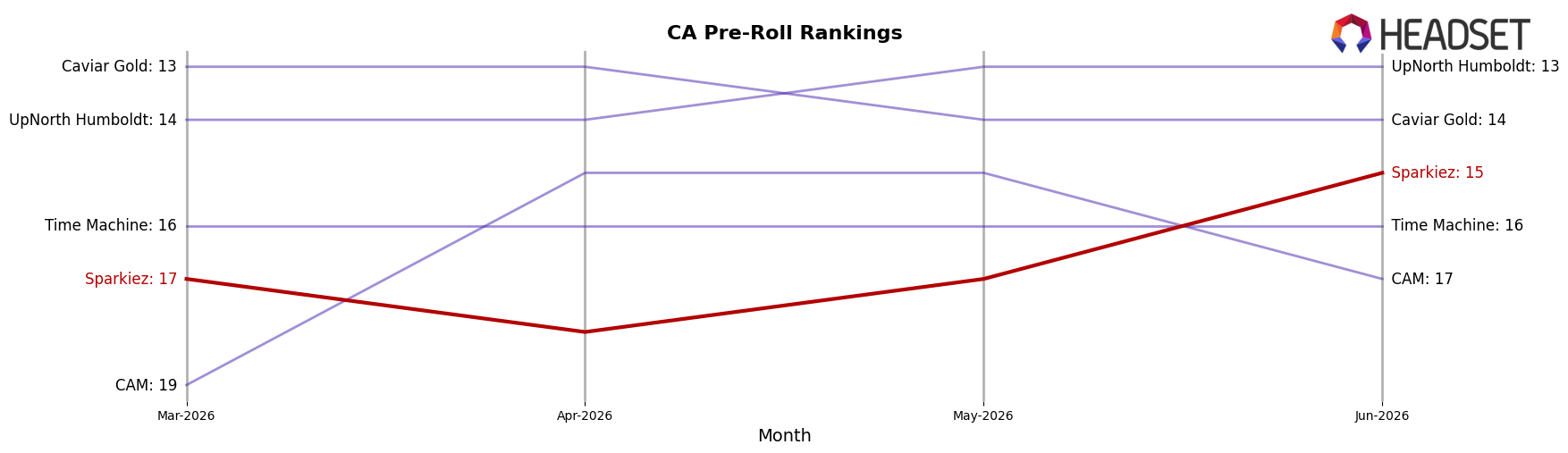

Sparkiez sits at rank #15 in CA Pre-Roll in June 2026, down 1 position YoY from #14 and up 2 positions from March 2026’s #17, while its historical peak was #12 in December 2024. In contrast, Jeeter held #1 both YoY and currently (#1 to #1), and CannaBiotix (CBX) climbed from #7 to #4, indicating upward mobility among leaders as Sparkiez slipped one rank YoY. This mix of a modest YoY decline (-1 rank) but a quarter-over-quarter improvement (-2 ranks since March 2026) implies Sparkiez is stabilizing mid-pack, and the trajectory points to a need for share-capturing moves to prevent further drift from the December 2024 peak.

Notable Products

Jack Pre-Roll 14-Pack (14g) posted the steepest decline at -22% month over month while sliding to rank 6, and Guava Pre-Roll (1g) fell -13% at rank 7. In contrast, Guava Pre-Roll 14-Pack (14g) rose 24% to hold rank 1 and Sativa Pre-Roll 14-Pack (14g) gained 13% at rank 8, while Bubba Kush Pre-Roll 14-Pack (14g) added 9% at rank 4. Four of the top ten are 14-Pack SKUs concentrated in Pre-Roll, and that pack-size tilt is reinforced by Hindu Kush Pre-Roll 14-Pack (14g) at rank 3 with a 5% increase. The pattern implies Sparkiez is consolidating around multi-pack Pre-Rolls, with single-gram formats ceding share to higher-count packs that anchor the top ranks and larger dollar volume, led by Guava Pre-Roll 14-Pack (14g) at $110,686.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.