Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

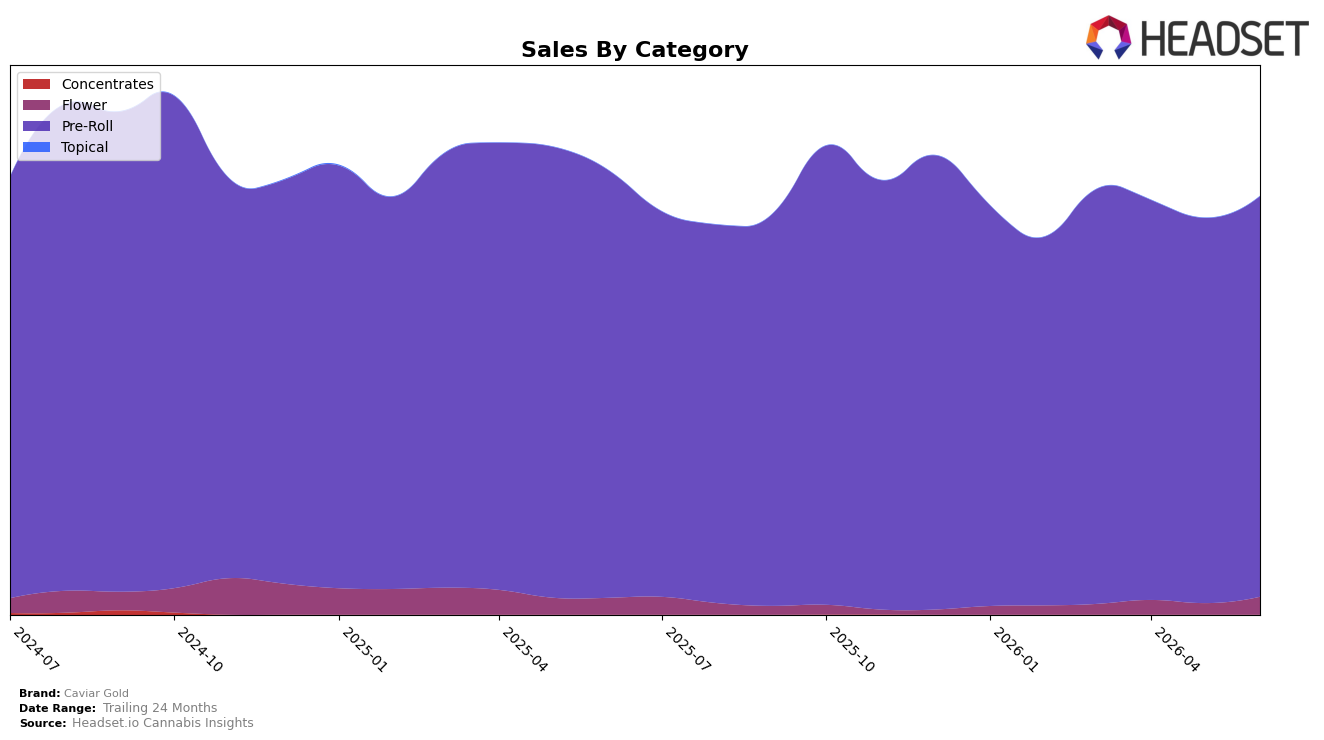

Caviar Gold concentrated 95.80% of June 2026 sales in Pre-Roll, while Flower accounted for 4.20%, indicating an extreme tilt toward a single category. Within Pre-Roll, year-over-year sales fell 6.34% as average price moved to $15.21, but month-over-month sales rose 4.00%, pointing to short-term demand stability despite annual contraction. Flower moved in the opposite direction: year-over-year sales grew 6.49% and month-over-month surged 56.85% on a lower $14.33 average price, lifting its share from a small base without yet reshaping the mix. The pattern implies Caviar Gold is still anchored to Pre-Roll for scale while Flower is emerging as a tactical growth pocket that can buffer volatility in the core.

Positioning-wise, the mix suggests Caviar Gold is optimized for Pre-Roll shelf presence, as shown by a Pre-Roll rank of 14 in California alongside a 4.00% month-over-month uptick, yet the 6.34% year-over-year decline signals pressure that a 56.85% month-over-month Flower spike can partially offset. With overall brand sales down 5.87% year-over-year and average price down 10.98%, the combination points to a price-led defense in Pre-Roll while testing elasticity through Flower, implying a barbell strategy: protect rank in California Pre-Roll and use Flower’s faster percentage gains to diversify revenue momentum.

Competitive Landscape

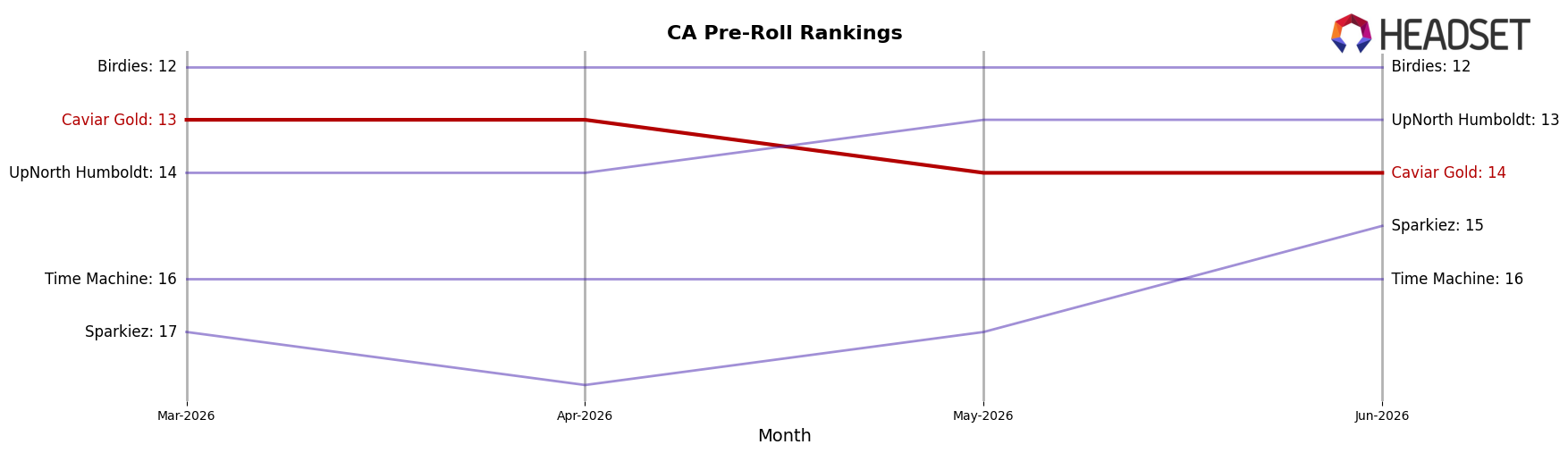

Caviar Gold sits at rank #14 in June 2026 in CA Pre-Roll, slipping 1 position year over year from #13, and down 1 spot from its March 2026 position of #13, while its peak of #12 in December 2025 is now 2 ranks higher than current. In contrast, CannaBiotix (CBX) advanced from #7 to #4 alongside a 39.1% YoY sales increase, and Presidential held steady at #5 with 7.7% YoY growth, placing Caviar Gold 9 positions behind a stable top-5 competitor and 10 positions behind category leader Jeeter at #1 with 0.7% YoY growth. This rank drift of 1 place over the year, coupled with rivals either climbing or defending top-5 slots, implies Caviar Gold is ceding relative share and must either trade up in velocity or assortment to re-enter the #12–#13 band it last occupied in December 2025–March 2026.

Notable Products

Cavi Cone - Lost Louie Infused Pre-Roll (1.5g) posted the standout move in June 2026 with a +51% month-over-month surge that pushed it to rank 2, while Cavi Cone - Lightning OG Infused Pre-Roll (1.5g) fell 18% to rank 4. The top five also included Cavi Cone - Apple Drip Infused Pre-Roll 3-Pack (1.5g) at rank 1 with +22% MoM, whereas Cavi Cone - King Cavi OG Infused Pre-Roll (1.5g) slid 17% to rank 6. Nine of the top ten are Pre-Roll SKUs, concentrating sales into a single format and indicating the portfolio is leaning further into infused cones rather than diversifying into other categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.