Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sungaze is stocked at 71 licensed dispensaries across Washington, with the deepest coverage in Seattle, Bellevue, Tacoma, Spokane, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

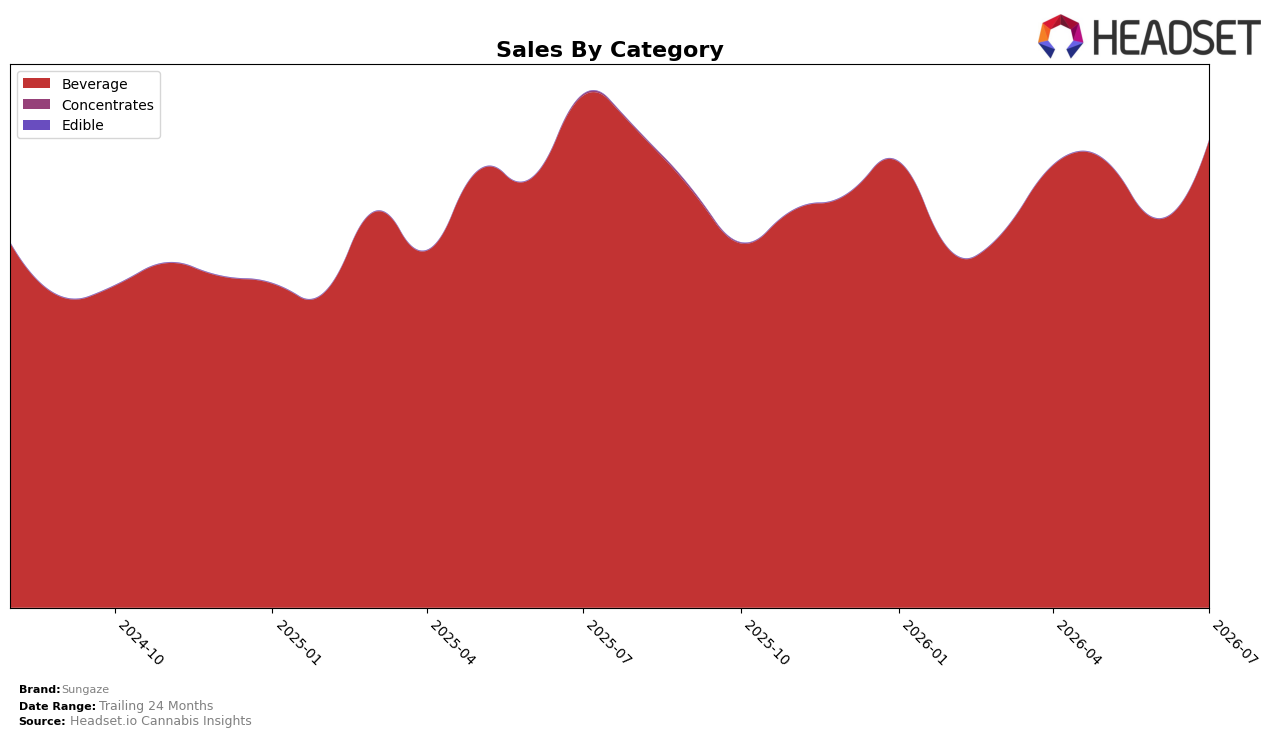

Sungaze concentrated 100.0% of July 2026 sales in Beverage, with category sales up 20.27% month over month but down 8.70% year over year; the brand’s overall sales decline of 8.89% YoY tracks closely with Beverage’s -8.70% YoY, while average price fell 28.36% YoY alongside a 20.27% MoM lift in category sales. In Washington Beverage, Sungaze sits at rank 15 and posted a 20.27% MoM sales increase as its average price of $5.96 coincided with a 28.36% YoY price drop, implying the July 2026 volume uptick was driven primarily by pricing-led elasticity within a single-category footprint rather than assortment expansion.

The mix locked at 100.0% Beverage plus a rank of 15 in Washington signals limited insulation from category headwinds, as the -8.70% YoY category movement mirrors the brand’s -8.89% YoY trend while the 20.27% MoM rebound paired with a 28.36% YoY price compression indicates a trade-down dynamic. This pattern implies positioning that is skewed toward value-sensitive segments where price reductions convert to short-term share defense at rank 15, but without diversification beyond Beverage, the July 2026 bounce is more a pricing response than a durable shift in demand.

Competitive Landscape

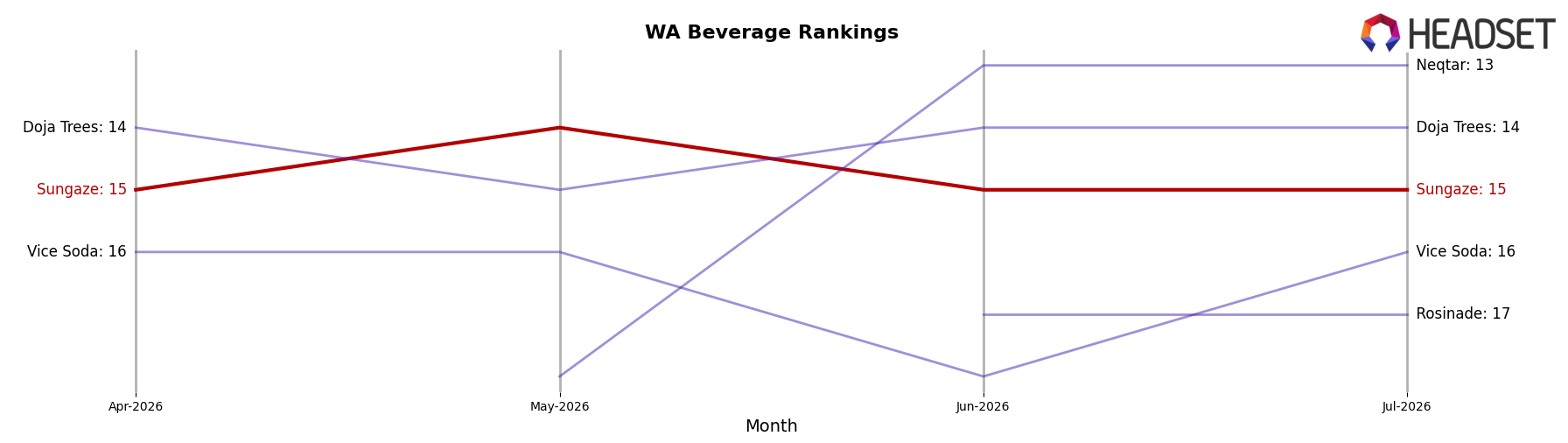

Sungaze sits at #15 in WA Beverage in July 2026, down 3 positions year over year from #12, while holding flat versus three months ago at #15; meanwhile, Journeyman climbed from #2 to #1 and Ray's Lemonade slid from #1 to #2 with a -31.4% sales change year over year as Blaze Soda jumped from #8 to #4 on 130.5% YoY growth, indicating share is consolidating toward movers rather than mid-pack holders; given Sungaze’s peak of #11 in September 2024 and no rank improvement across the last three months, the trajectory implies that maintaining the current position risks gradual share erosion as faster-rising rivals re-order the top 10.

Notable Products

Zero Sugar - CBD/THC 2:1 Strawberry Citrus Seltzer (5mg CBD, 2.5mg THC, 355ml) posted the largest month-over-month jump at 167.5% while moving into rank 3, outpacing the 111.3% surge for CBD/THC 2:1 Strawberry Citrus Seltzer (5mg CBD, 2.5mg THC, 355ml) at rank 2. At the same time, CBD/THC 2:1 Lemon Ginger Seltzer 2-Pack (10mg CBD, 5mg THC, 12oz, 355ml) fell 17.5% to rank 4 and the Zero Sugar 2-Pack variant declined 17.6% at rank 10, indicating pack formats and Lemon Ginger are ceding momentum to single-serve Strawberry Citrus options. Supernova - CBD/THC 2:1 Strawberry Citrus Seltzer (10mg CBD, 5mg THC, 12oz, 355ml) climbed 88.8% to rank 1, while the Strawberry Citrus 6-Pack dipped 1.2% at rank 9, and eight of the top ten are Beverage SKUs concentrated in 2:1 seltzers; this mix implies Sungaze is consolidating around Strawberry Citrus singles, prioritizing zero-sugar and core 2:1 formats over multipacks and Lemon Ginger.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.