Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

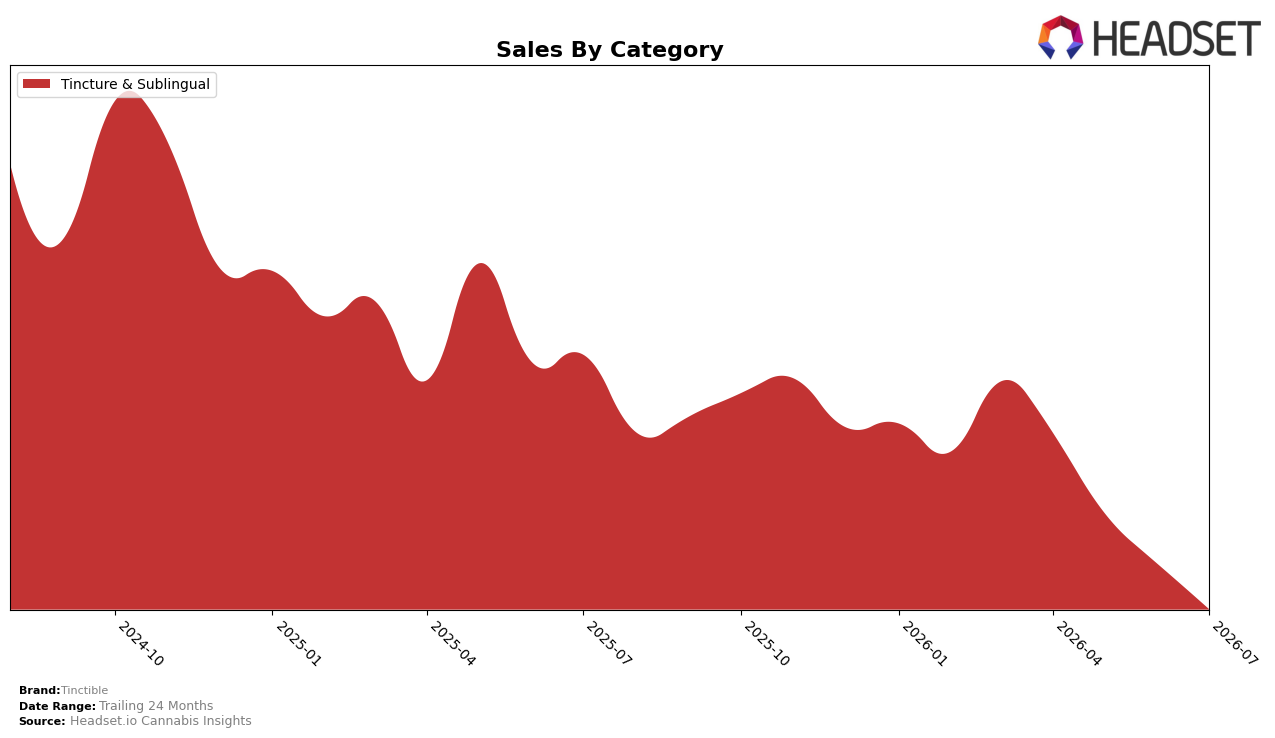

Tinctible concentrated entirely in Tincture & Sublingual for July 2026, with category share at 100.0% and a month-over-month drop of 58.9999% alongside a year-over-year decline of 89.0336%. Average price fell 19.6628% year over year to $16.17, within a single-category mix that leaves no buffer from a 58.9999% monthly contraction and an 89.0336% annual pullback. With no rank reported in Ohio for Tincture & Sublingual, the pattern implies the brand’s single-category exposure is amplifying downside volatility and constraining visibility in its top market.

The dual compression of volume (down 89.0336% year over year and 58.9999% month over month) and pricing (down 19.6628% year over year) within a 100.0% Tincture & Sublingual mix suggests positioning that is overly tied to one format’s demand curve. The combination of a 24‑month sales decline of 89.7158% and the absence of a category rank in Ohio indicates price adjustments have not offset share erosion, implying the brand must either diversify beyond Tincture & Sublingual or define a narrower price-led role within it to stabilize monthly swings and rebuild rank traction.

Competitive Landscape

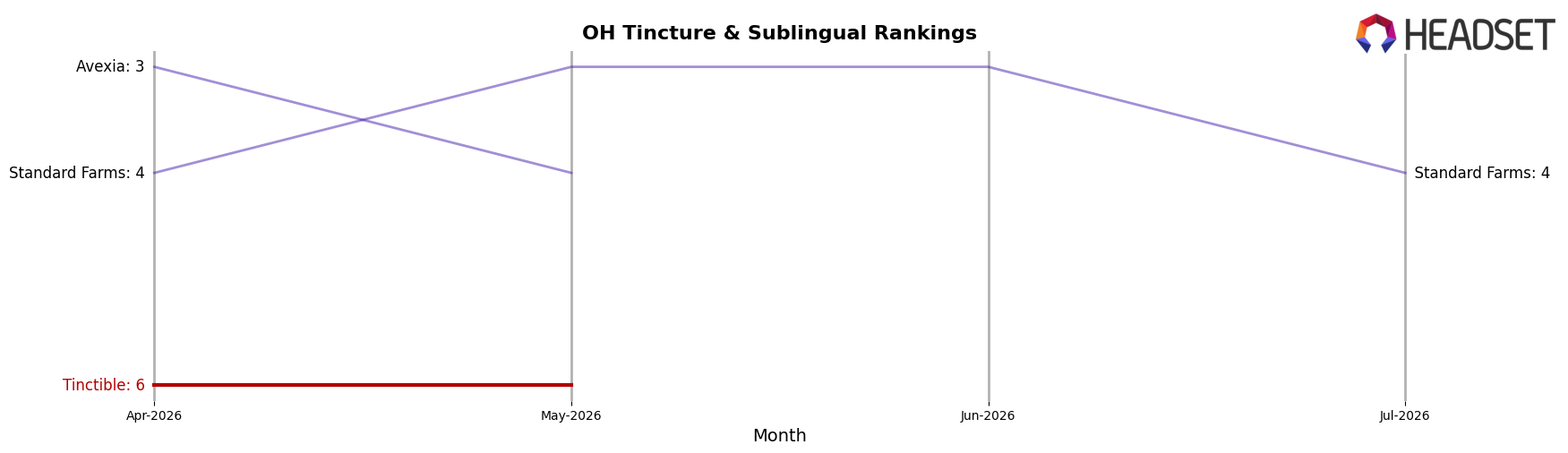

Tinctible sits at rank #8 in Ohio Tincture & Sublingual for July 2026, slipping 1 place year over year from #7 while falling 2 spots from #6 three months ago, and it remains 4 positions below its peak of #4 last reached in February 2025; by contrast, UB GOOD held #1 both this year and last as its sales grew 24.0% year over year, and Avexia stayed at #5 despite an 80.8% sales decline, indicating that Tinctible’s downward rank drift amid both stable leaders and contracting mid-tier rivals points to share being ceded to the category’s top performers rather than gained from weakening peers.

Notable Products

Squeeze In - THC/CBN 3:1 Blueberry Lavender Sleep Gel 11-Pack (110mg THC, 33mg CBN) posted the steepest decline at -76.2% MoM and sat at rank 3, setting the tone for a retrenchment across the lineup. The flagship Squeeze In- THC/CBG/CBD 2:1:1 Relief Blue Raspberry Gel 11-Pack (110mg THC, 55mg CBG, 55mg CBD) fell -51.1% MoM yet held rank 1, while Squeeze In- CBD/THC 1:1 Spark Watermelon Gel 11-Pack (110mg CBD, 110mg THC) dropped -49.9% MoM at rank 2. All three top-3 SKUs are Tincture & Sublingual formats, concentrating the portfolio at the category apex and implying Tinctible is leaning into a narrow form-factor focus that risks volatility when a single segment softens.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.