Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Standard Farms is stocked at 265 licensed dispensaries across Pennsylvania, Ohio, and Massachusetts, 100 of them in Pennsylvania, with the deepest coverage in Philadelphia, Pittsburgh, Lancaster, Altoona, and Cranberry Twp. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

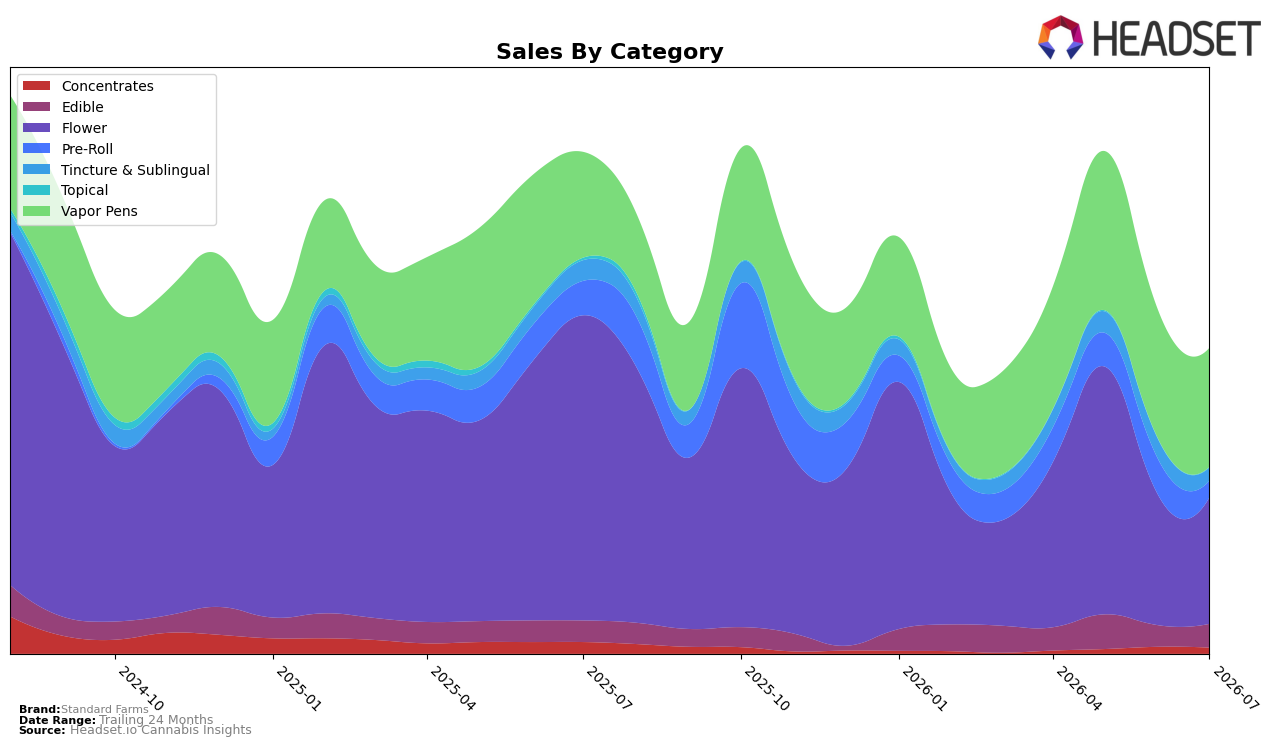

In July 2026, Standard Farms leaned on a two-pillar mix where Flower held 40.95% share with year-over-year sales down 58.46% and month-over-month down 3.06%, while Vapor Pens carried 38.54% share with year-over-year up 12.36% but month-over-month down 7.50%. Edible contributed 7.85% share with year-over-year up 9.84% and month-over-month up 9.71%, whereas Pre-Roll slid to 5.58% share with year-over-year down 50.54% and month-over-month down 52.45%. Tincture & Sublingual represented 4.48% share with year-over-year down 34.67% and month-over-month down 31.94%, and Concentrates at 2.20% share fell 45.05% year-over-year and 10.95% month-over-month, with Topical at 0.40% share down 60.51% year-over-year but up 4.00% month-over-month. Despite an overall brand sales decline of 38.71% year-over-year alongside a 19.78% year-over-year drop in average price, the mix implies the brand is reallocating demand from contracting Flower and Pre-Roll toward steadier Vapor Pens and Edible to buffer volatility.

The split momentum—Vapor Pens up 12.36% year-over-year but down 7.50% month-over-month, versus Flower down 58.46% year-over-year with only a 3.06% month-over-month pullback—signals a pivot toward inhalables with more defensible annual traction, while Edible’s 9.71% month-over-month lift alongside a 9.84% year-over-year gain suggests a secondary consumption occasion gaining relevance. With Tincture & Sublingual contracting 31.94% month-over-month and 34.67% year-over-year and Concentrates shrinking 10.95% month-over-month and 45.05% year-over-year, the brand’s positioning is consolidating around mid-price, higher-velocity formats, implying Standard Farms can concentrate assortment and pricing around Vapor Pens and Edible while using Flower as a scaled but de-emphasized volume driver.

Competitive Landscape

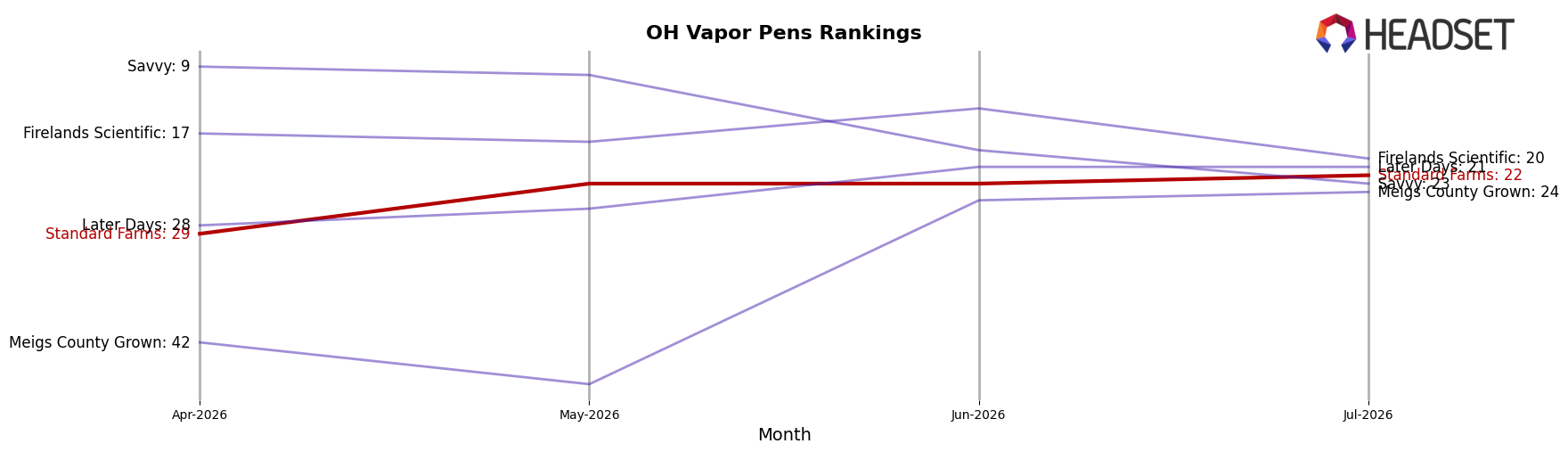

Standard Farms sits at rank #22 in July 2026 in OH Vapor Pens, improving 12 positions year over year from #34, yet slipping 7 spots from April 2026’s #15 peak and 7 spots from April 2026’s three-month reference at #29, indicating mixed momentum within the quarter. Against the field, Certified (Certified Cultivators) held #1 with a 76.8% year-over-year sales increase while &Shine rose from #3 to #2 with 27.3% growth, outpacing Standard Farms’ rank gains despite Select climbing from #5 to #3 on 55.6% growth; meanwhile, Butterfly Effect - Grow Ohio slid from #2 to #5 with a -2.3% change, showing volatility among leaders that Standard Farms has not converted into sustained share. The pattern implies a recovery arc—up 12 ranks year over year but down 7 ranks since April 2026—that requires near-term stabilization against faster-rising competitors to avoid reversion toward the low-30s.

Notable Products

Meyer Hashky Pre-Roll (1g) posted the steepest decline at -55.7% while still holding rank 1, whereas LA Kush Cake Pre-Roll (1g) surged +91.5% into rank 4, indicating volatility concentrated within the Pre-Roll lineup. Sunburst Distillate Disposable (1g) slipped -12.5% at rank 7 as Golden Hour Distillate Cartridge (1g) in rank 9 inched up +1.2%, and Vapor Pens accounted for three of the top ten with a combined presence across ranks 6, 7, 9, and 10 anchoring a higher-dollar tier at $22,276 for Sunburst. With five of the top ten in Pre-Roll, the mix suggests Standard Farms is leaning on breadth in value-driven Pre-Rolls while using Vapor Pens to stabilize revenue and hedge against Pre-Roll swings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.