Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Kanha / Sunderstorm is stocked at 1,081 licensed dispensaries across California, Massachusetts, and 2 other states, 732 of them in California, with the deepest coverage in Los Angeles, Sacramento, San Francisco, San Diego, and Santa Ana. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

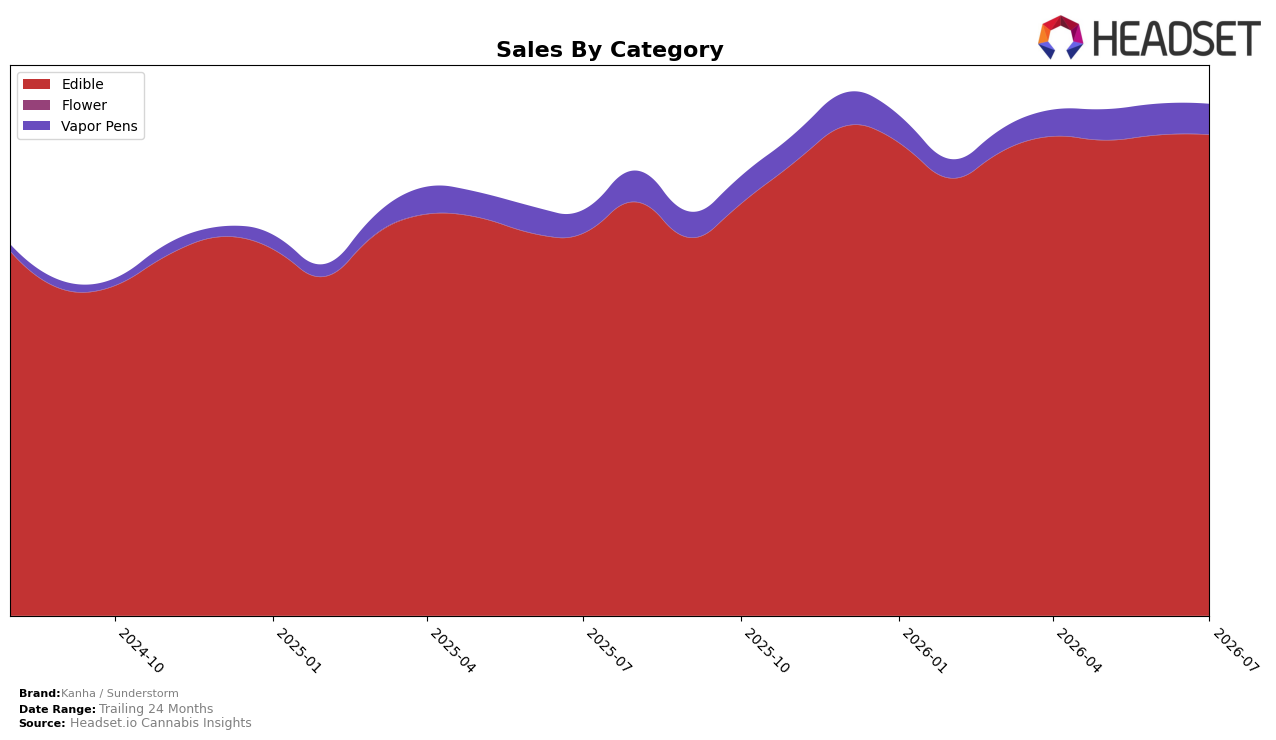

In July 2026, Kanha / Sunderstorm derived 94.09% of sales from Edible, up 25.85% year over year and up 0.08% month over month, while Vapor Pens held 5.91% share with 32.59% year-over-year growth but a 1.75% month-over-month decline; overall brand sales were up 26.22% year over year as average price fell 1.46%. The Edible average price sat at $15.94 versus $36.55 in Vapor Pens, and the near-flat month-over-month gain in Edible alongside the Vapor Pens month-over-month dip indicates volume-led stability in the core with limited cross-category momentum right now.

Kanha / Sunderstorm’s category concentration positions it as an Edible-led brand with a #2 rank in Edible in Massachusetts, implying competitive parity near the top tier while price elasticity remains manageable given a 1.46% average price decrease against 26.22% year-over-year sales growth. The combination of a 0.08% month-over-month uptick in Edible and a 1.75% month-over-month slide in Vapor Pens suggests the brand’s short-term gains hinge on preserving Edible depth rather than expanding share via Vapor Pens, which points to reinforcing market presence in Massachusetts and scaling the Edible engine where rank tailwinds already exist.

Competitive Landscape

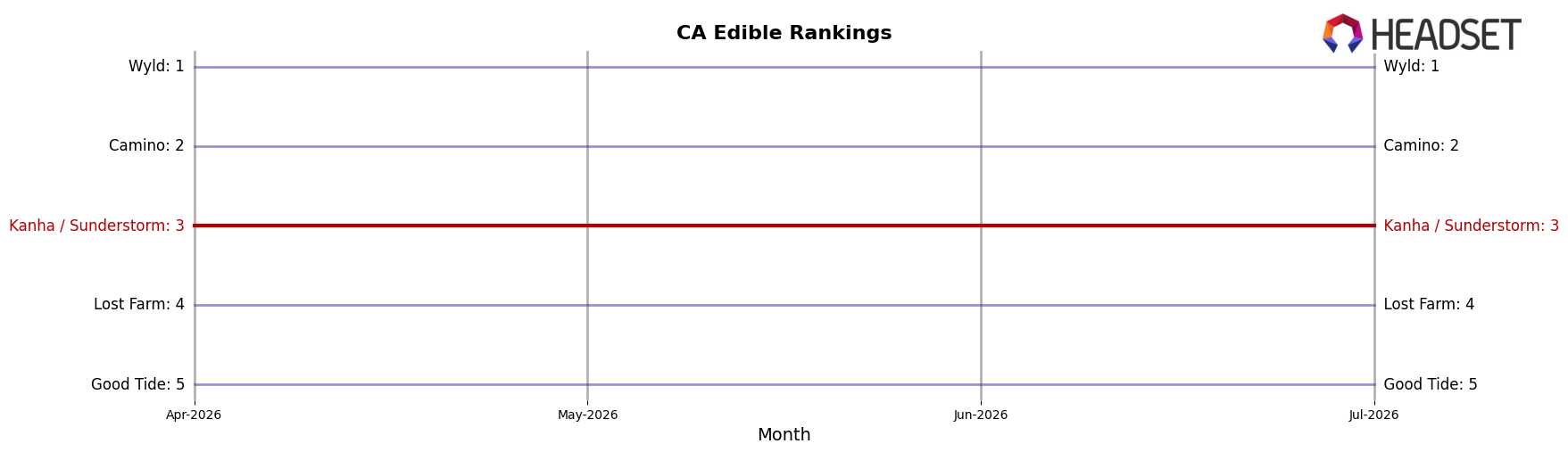

In California Edible, Kanha / Sunderstorm sits at rank #3 in July 2026 with no year-over-year rank change from #3, and no three-month movement from #3 to #3, indicating stable placement while the category shuffled elsewhere; Wyld held #1 with a 2.20% year-over-year sales increase while Camino maintained #2 alongside a 14.77% increase, positioning Kanha / Sunderstorm behind two brands that paired static ranks with positive sales momentum. Down-market pressure is limited as Lost Farm remained at #4 with 12.84% year-over-year growth and Good Tide stayed #5 with 22.07% growth, so the short-term risk is less about a rank drop and more about a widening performance gap. The pattern implies that holding #3 through July 2026 without rank churn converts into a share-defense challenge: absent above-market growth, static rank against faster-growing peers will translate into relative share erosion even if dollar sales remain steady.

Notable Products

Sour Cherry Limeade Solventless Rosin Gummy Belts 4-Pack (100mg) posted the steepest movement in July 2026 with a -9.61% month-over-month decline while sliding to rank 10, contrasting with the category leader CBN/THC/CBG 3:2:1 Sleep Marionberry Plum Gummies 10-Pack (150mg CBN, 100mg THC, 50mg CBG) that edged up +5.22% at rank 1. Love - THC/THCV/CBG 2:1:1 Raspberry Rose Gummies 10-Pack (100mg THC, 50mg THCV, 50mg CBG) advanced +10.73% at rank 3 as Blueberry Lemon Drop Rosin Sour Gummy Belts 4-Pack (100mg) softened -1.88% at rank 2, indicating momentum is concentrating in functional formulations rather than flavor-led variants. With four of the top ten being solventless rosin formats and three functional multi-cannabinoid SKUs in the top seven, the mix tilts toward differentiated effects over novelty flavors, implying Kanha / Sunderstorm is leaning into effect-segmented edibles to defend premium shelf positions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.