Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

1906 is stocked at 735 licensed dispensaries across New York, Oklahoma, and 5 other states, 211 of them in New York, with the deepest coverage in New York, Schenectady, Brooklyn, Queens, and Rochester. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

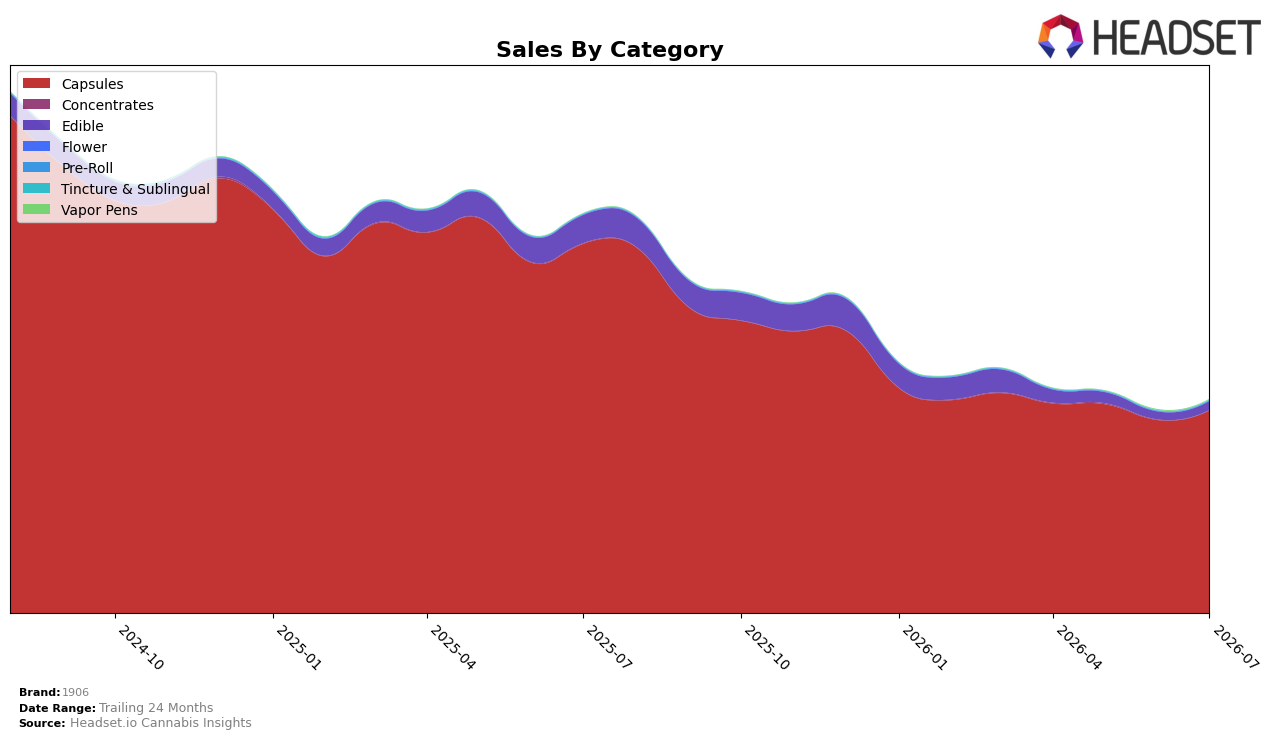

Capsules concentrated to 95.78% share in July 2026 with a month-over-month gain of 4.95% despite a year-over-year decline of 45.20%, while Edible slipped to 4.09% share after a 68.85% year-over-year drop but expanded 14.70% month-over-month. Peripheral bets stayed tiny: Vapor Pens held 0.12% share with a 44.32% month-over-month contraction and no year-over-year baseline, and Pre-Roll sat at 0.02% share even as month-over-month sales spiked 1,428.76% against a 17.11% year-over-year fall. With Capsules ranked 1 in Illinois and average price down 3.24% year over year to $20.66, the pattern implies 1906 is doubling down on its core format while trimming price to defend volume, leaving other formats as experimental rather than material contributors.

The mix shift, where Capsules’ share approaches 96% alongside Edible’s year-over-year contraction of 68.85% and Vapor Pens’ 44.32% month-over-month drop, tilts positioning toward a single-use-case proposition rather than a portfolio play. The contradiction of Capsules’ 4.95% month-over-month uptick amid a 45.20% year-over-year decline, plus Pre-Roll’s outsized 1,428.76% month-over-month jump from a near-zero base, implies 1906 is using limited, low-risk extensions to probe demand while reinforcing leadership in Capsules, prioritizing depth over breadth to sustain rank 1 in Illinois.

Competitive Landscape

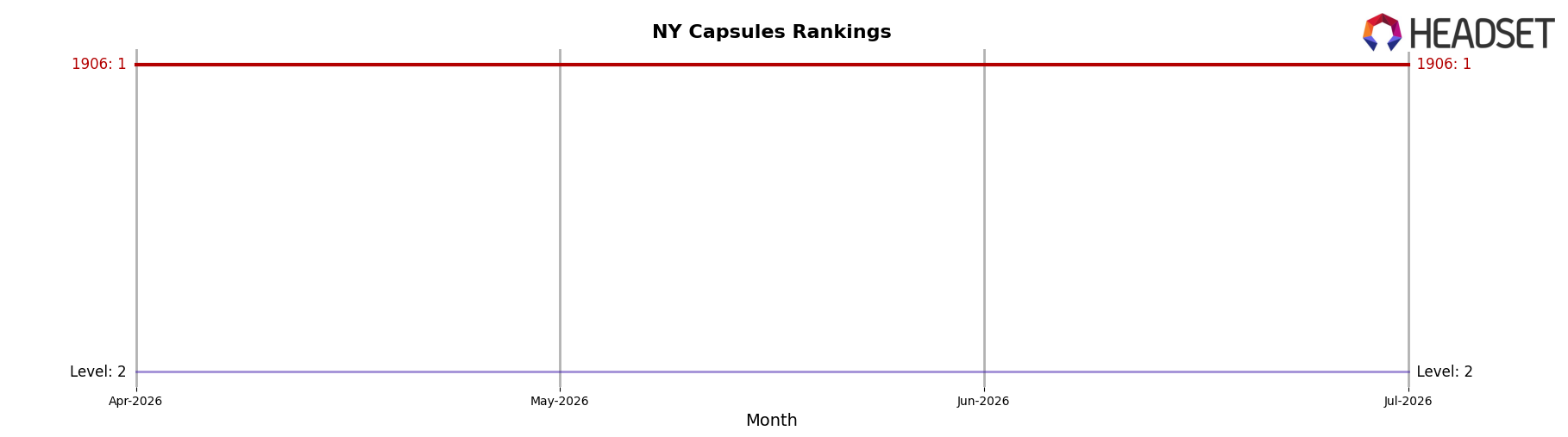

1906 is ranked #1 in New York Capsules in July 2026, unchanged from #1 a year ago, and also steady at #1 over the last three months, signaling rank stability while peers moved. Level sits at #2 versus #2 a year ago with sales down 14.9% year over year, while Revival climbed to #4 from #7 with a 9503.3% year-over-year sales jump, indicating that the closest incumbent slipped as a fast riser advanced from lower ranks. Canna Clinicals fell to #5 from #3 alongside a 21.7% decline, and Grassroots holds #3 with no year-over-year rank detail reported, together suggesting that 1906’s unchanged #1 amid competitor rank churn implies durable category leadership but rising pressure from challengers improving share momentum.

Notable Products

CBD/THC 1:1 Go Drop Tablets 20-Pack (100mg CBD, 100mg THC) posted the standout move in July 2026 with +26.6% MoM, rising to rank 4, while category leader CBD/THC 1:1 Bliss Tablets 20-Pack (100mg CBD, 100mg THC) slipped -6.0% but held rank 1. CBD/THC 1:1 Love Drops 30-Pack (75mg CBD, 75mg THC) climbed +22.7% to rank 7 as CBD/THC 1:1 Genius Drops 30-Pack (75mg CBD, 75mg THC) advanced +15.4% at rank 6, and eight of the top ten SKUs are Capsules, concentrating share at the expense of the lone Edible at rank 10. Despite mixed moves at the top, the skew toward Capsules with multiple double‑digit MoM gains signals an intentional push deeper into fast-moving functional capsules rather than broadening into edibles.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.