Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

AiroPro is stocked at 1,039 licensed dispensaries across Missouri, Maryland, and 19 other states, 155 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Springfield, Columbia, and Independence. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

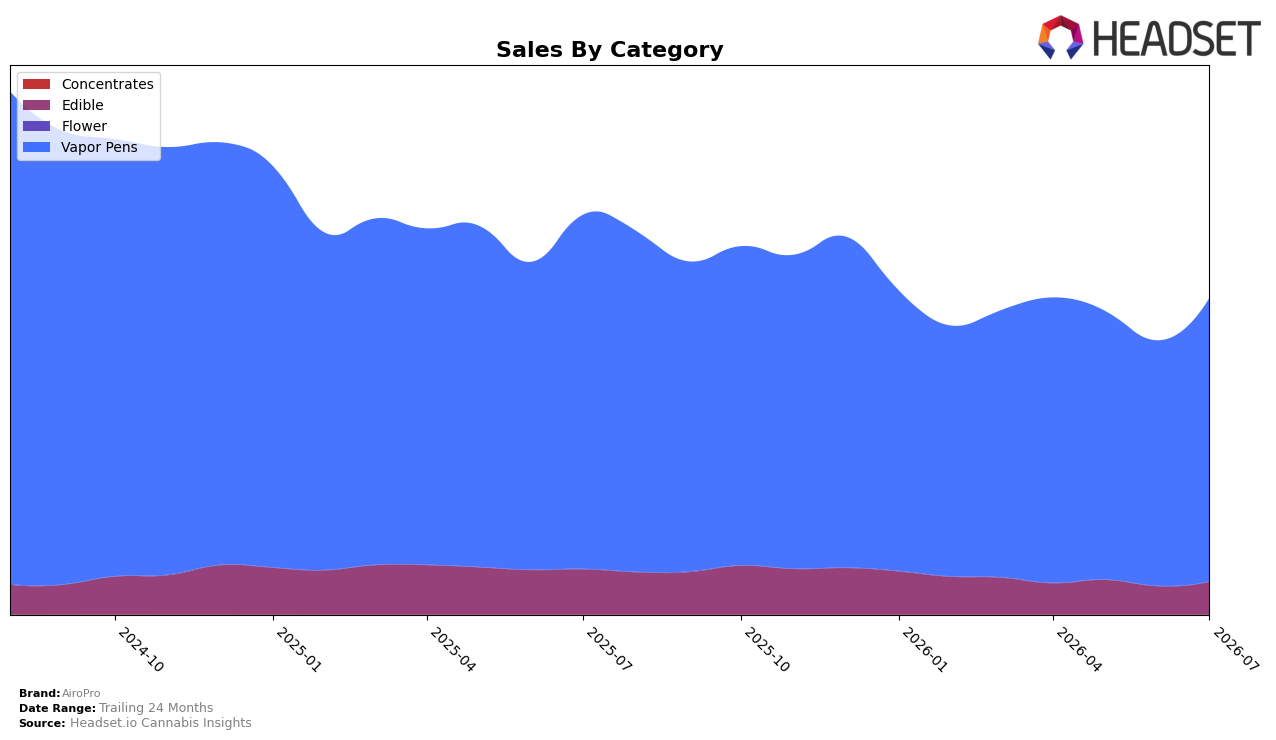

In July 2026, AiroPro concentrated 89.73% of sales in Vapor Pens, with Edible contributing 10.27%, indicating heavy reliance on a single category. Vapor Pens declined 19.97% year over year but climbed 15.54% month over month, while Edible fell 27.77% year over year yet rose 15.74% month over month, pairing broad annual contraction with short-term recovery. The average price slipped 0.32% year over year to $40.10, and AiroPro ranked 5 in Vapor Pens in Nevada, signaling a mix where near-term volume is rebounding off a lower base but the annual drag persists due to outsized exposure to Vapor Pens and deeper Edible declines.

With Vapor Pens carrying nearly nine-tenths of the mix and posting a 15.54% month-over-month increase against a 19.97% year-over-year drop, AiroPro’s positioning hinges on capturing intra-quarter demand spikes while managing annual share erosion. The 27.77% year-over-year decline in Edible alongside a 15.74% month-over-month uptick suggests tactical wins that do not yet offset category drag; coupled with a 0.32% average price decrease and a rank of 5 in Nevada Vapor Pens, the pattern implies a strategy oriented toward volume-led regain in Vapor Pens with limited diversification benefits from Edible in the current window.

Competitive Landscape

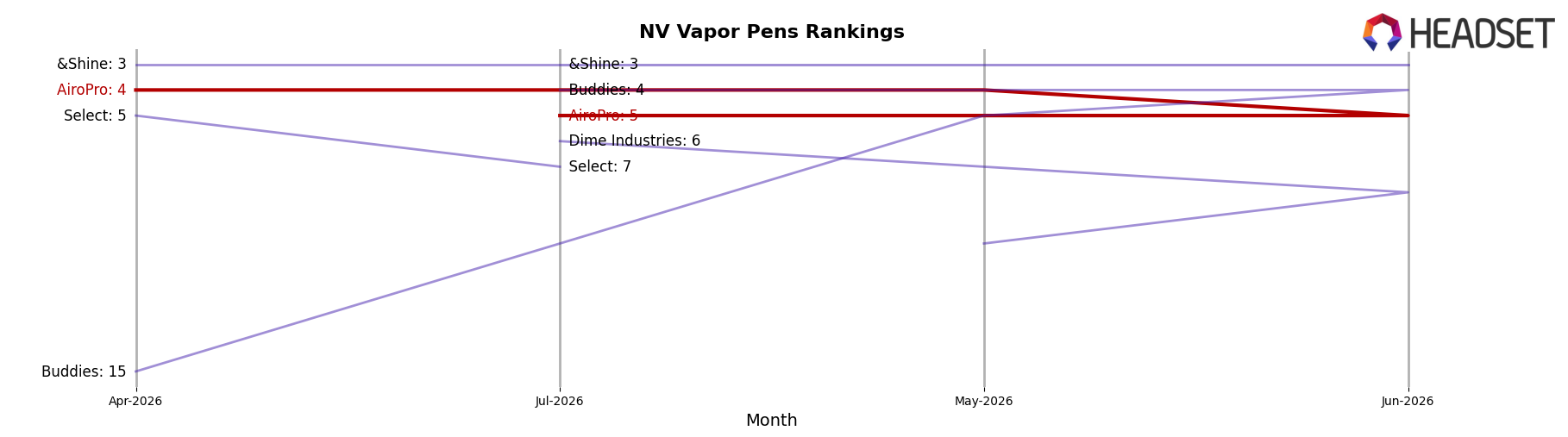

AiroPro ranks #5 in NV Vapor Pens in July 2026, improving 3 positions from #8 in July 2025, while slipping 1 spot from #4 in April 2026; meanwhile, Rove held #1 year over year with a -31.8% sales change and STIIIZY stayed at #2 with a -38.6% sales change, indicating that AiroPro’s upward rank shift contrasts with top competitors’ static positions despite their double-digit declines. Compared with &Shine at #3 (down -15.7% in sales YoY) and Buddies at #4 (no YoY rank available), AiroPro’s move from #8 to #5 and its peak at #4 in May 2026 suggest gains are driven more by relative outperformance than absolute category expansion, implying a trajectory of share capture as incumbents contract.

Notable Products

Artisan Series - Black Mamba BDT Distillate AiroPod Cartridge (1g) posted the largest movement in July 2026 with a +63.0% month-over-month surge to rank 1, while its sibling Artisan Series - Black Mamba BDT Distillate AiroX Disposable (1g) climbed to rank 7 on +38.0% MoM, indicating accelerated pull for the Black Mamba flavor across formats. The 2g Artisan Series - Black Mamba BDT Distillate AiroX Disposable held rank 2 with +24.3% MoM, and four of the top five SKUs are Vapor Pens, signaling a concentration toward inhalable formats over Edibles where the lead Oria gummies at rank 3 grew +28.2% but remain a smaller contributor at $58,202. The pattern implies AiroPro is consolidating around Black Mamba-led Vapor Pen platforms and larger 2g devices, prioritizing format breadth within a narrow flavor franchise to drive share at the top of the ranking.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.